November 2025 could be a turning point for crypto. From ETFs to major network upgrades, here are six catalysts that could shape the market.

Keep reading

As we move into November 2025, the crypto-market is gearing up for one of its most intriguing phases yet. From spot-ETF momentum to narrative shifts, network upgrades and real-world asset tokenization, multiple catalysts are aligning. Here are six key developments to watch.

1. Seasonality & Historical Momentum Could Kick In

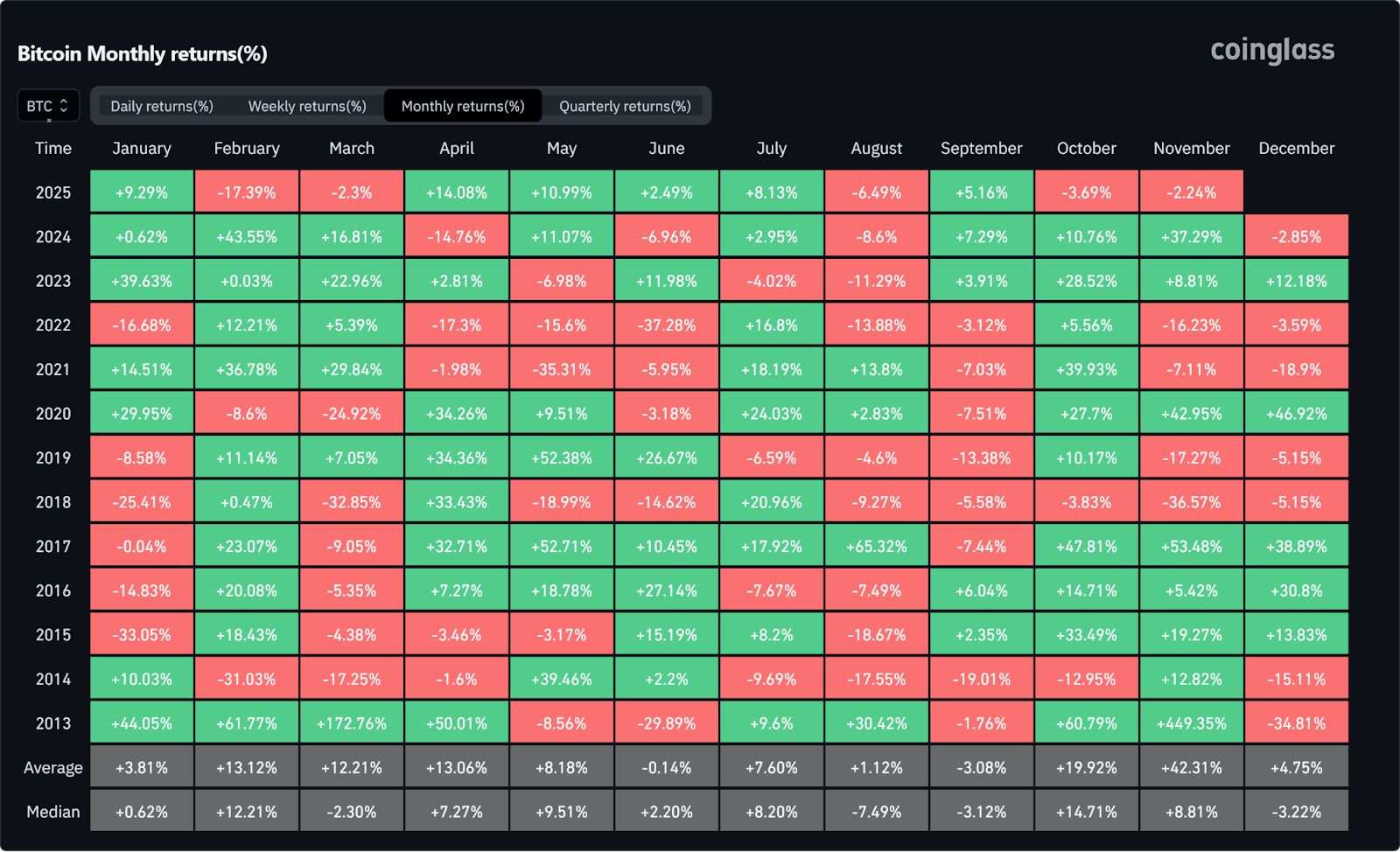

While "Uptober" fell short of expectations, November could tell a different story. Historically, it's been one of the strongest months for digital assets, with Bitcoin in particular averaging +42.31% gains in recent years.

When combined with the renewed ETF narrative, increased whale accumulation, and a stronger appetite for risk assets, market momentum appears to be building. Participants are closely monitoring how these dynamics could influence sentiment, especially as trading volumes and key technical levels come into play. If Bitcoin maintains stability around the $100K zone and Ethereum shows signs of renewed strength, November could become a more active month for crypto markets compared to October.

2. Ether’s Next Move Could Set the Tone for Altcoins

The final weeks of 2025 may prove pivotal for Ethereum (ETH). Although retail accumulation has paused somewhat, wallet-level data shows large holders (1,000 to 100,000 ETH wallets) added roughly 1.6 million ETH in October (around $6 billion), it’s a sign that whales and larger holders are staying active as the year winds down.

If ETH begins to break out or even stabilize around current levels, it could unlock the broader altcoin market, which has been lagging for months. The playbook that many are hoping for is the following one: ETH strength leads to improved risk appetite, which in turn sparks an altcoin rotation as investors seek higher risk exposure.

Ethereum remains the accepted benchmark for gauging sentiment across the non-Bitcoin segment of the market, and its performance frequently acts as a catalyst for capital flows into smaller assets. Keeping an eye on its fundamentals (from staking yield to liquidity shifts on major exchanges) will be important. In many ways, ETH could potentially become the gatekeeper to the next phase of the market’s recovery and the tone-setter for the coming months.

3. ETF Comeback After Delays

The recent U.S. government shutdown briefly froze several crypto-spot ETF filings, leaving the “ETF narrative” in suspense. But now the pause is over for Bitwise’s Spot Solana ETF. It has finally launched with strong early inflows, and the broader momentum is returning.

With this foundation, November could reignite the ETF trade in earnest, we may finally see filings for Ethereum staking products, new spot-Bitcoin funds and renewed institutional interest. If filings begin to stack up and regulatory engagement deepens, this could mark the next major inflection for how crypto is accessed in traditional portfolios.

4. Altcoins at an Inflection Point

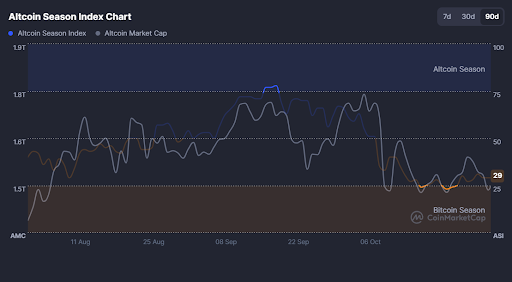

The broader altcoin sector enters November under pressure as the Altcoin Season Index sits near 29, signaling a reset after October’s downturn. But inflection points often follow pressure. If ETH sets the tone (as many are hoping for), mid-cap and high-beta altcoins (such as SOL, AVAX, NEAR) could begin to capture rotation flows.

Traders might want to watch for flow changes such as increased volumes, wallet relocations and new project launches. While caution is still prevailing, this may be the window where sentiment begins to swing back into “altcoin season”.

5. Major Network Upgrades

Technical infrastructure is not just background noise; it often creates catalyst-events. For example, Ethereum’s upcoming Fusaka Upgrade (scheduled for early December) is designed to increase layer-2 data capacity and reduce transaction costs.

Meanwhile, various Layer-2 ecosystems are preparing upgrades and cross-chain activations. One such upgrade, Shibarium Upgrade’s security overhaul on the Shiba Inu network. These events may ignite renewed network activity, developer interest and capital flows into ecosystems ready to scale.

6. Real-World Asset (RWA) Tokenization Accelerates

The tokenization of real-world assets (RWAs), such as real estate, bonds, equities, is moving from niche to mainstream. For instance, according to Standard Chartered, this market is projected to grow to around $2 trillion by 2028. Institutional interest is burgeoning, and regulatory frameworks are emerging.

As November unfolds, we may see announcements of large tokenization initiatives or new platforms bridging DeFi and traditional finance. For crypto holders and ecosystem observers, this means the familiar “crypto only” narrative is expanding into real-asset integration, a meaningful broadening of the opportunity set.

The Verdict

November 2025 is shaping up to be more than just another month. Spot-ETFs potential, ETH’s path, altcoin rotation, seasonal tailwinds, infrastructure upgrades and RWA tokenization all sit in motion. Each one individually is significant; together they create a multi-vector setup.

For those in the crypto space, whether you're holding long-term, actively trading, or building the next wave of infrastructure, November is likely to be eventful. This isn't a month to coast on autopilot. Track where capital is flowing. Pay attention to which narratives are gaining momentum and which are fading. The players are moving, and the pieces are falling into place.

NEWS AND UPDATES

LATEST ARTICLE

-your-emergency-fund.png)

We've all been caught off guard with an emergency payment - from having to replace an appliance to an unexpected medical bill. These things happen and they're out of our control, so it's best to be prepared. Emergency funds are the best way to protect yourself, and a great way to start building your savings.

These unforeseen expenses shouldn't cripple your savings. With an emergency savings fund, you can recover more quickly and get back on track to achieving your financial goals with little to no stress.

What is an emergency fund?

An emergency fund is easily accessible money stored in a bank account set aside specifically for unexpected expenses or financial emergencies, anything from medical expenses to a loss of income. Emergency savings are typically used for unplanned expenses that fall outside of your normal monthly spending, with the funds stored in a savings account.

These funds allow you to weather the storm and avoid the need (and costs) of taking out a high-interest loan or credit card debt. Keeping the funds in a savings account removes the temptation to spend it, as would be the case if you stored the funds in a checking account.

Why emergency savings are important

Emergency or unexpected expenses without the proper precautions can quickly turn into debt or take a toll on your savings goals. And if hit with two or more in a row, this might cause long-term consequences that cause havoc on your finances.

Rather rest assured knowing that you have an emergency fund in place should something unexpected happen than fall back on costly loans and credit cards, or even other savings accounts like your retirement savings.

Emergency funds play an essential role in any reliable financial plan, providing peace of mind and a buffer for your other savings accounts. These funds can be used during periods of unemployment, the sudden death of a family member, illness and disability, or emergency home and auto repairs. Never underestimate the importance of an emergency fund and its impact on your financial well-being should something go wrong.

Start your emergency fund with these 7 simple steps

1. Review your monthly budget and see where you can save

It's critical to understand where your money is going so you can find ways to save it. Budgeting allows you to maximize your income and discover methods to decrease or control your spending.

To do this you can sit down with a financial advisor, or take matters into your own hand with your checking account statements, a pen and paper or a budgeting app. Be sure to review both your checking and savings accounts to get a clear picture. This is the first step in improving your financial health, and to start building your emergency fund.

2. Establish a goal amount for your emergency fund

A budget is a plan for spending that helps you figure out how much money you'll need each month to meet your essential expenses. A general rule of thumb when looking to build an emergency fund goal is to aim for six months' worth of income, enough to cover monthly expenses for housing, food, and transportation.

Don't be discouraged by how long this will take, rather establish a goal to work towards and move forward in that direction. Ideally, you want to be able to cover your living expenses for six months.

3. Create a direct deposit to your savings account

Avoid temptation by setting up a direct deposit from your current bank account (or wherever you receive your income) to your savings account. Better yet, you can create a split direct debit which allows you to automatically allocate funds to various accounts, including retirement funds etc.

If you're new to saving, experts recommend starting with an emergency fund, and once you've established this, move on to other savings accounts. If you already have a retirement fund or money market account set up, continue with this while building your emergency fund.

4. Little by little increase your savings

Increase the amount you're putting into your emergency fund by 1 percent or a certain amount over time until you've reached your savings goal. Increasing amounts gradually might help to make the smaller deposit into your checking account seem less noticeable and steadily build financial security.

5. Direct any unexpected income straight to your savings accounts

Commit to redirecting any unexpected income to your emergency fund, at least until you have reached your saving goal. This might be money from a bonus, inheritance, a tax refund, lottery winnings etc.

6. And once you've reached your goal? Save some more

Being unemployed for more than a year or being hospitalized for several months are both situations that require more than a six-month cushion. Should you find yourself here you’ll be glad you have more money saved in your emergency fund.

7. Find a bank account with perks that can kickstart your savings

When opening new checking or savings accounts, shop around by observing bank or credit union offers. Some banks offer cash incentives to new customers. Use this to kickstart your emergency fund, or to add a little extra to an already established one.

In conclusion

An emergency fund provides a cushion for unplanned events and can help you avoid taking on credit card debt or taking out a personal loan. By putting your emergency money in a high-yield savings account as opposed to checking and savings accounts, you can earn interest while you save money and build your nest egg.

Having an emergency fund saved in a separate account prevents you from spending the money and ensures that it is accessible in the case of an emergency. Emergencies can occur whether or not you are prepared; as a result, being prepared is the best way to deal with a potentially difficult scenario.

Knapphet är ett grundläggande begrepp som beskriver klyftan mellan våra oändliga behov och de begränsade resurser som finns tillgängliga i världen. Det handlar inte bara om varor och tjänster i vardagen — knapphet spelar också en avgörande roll inom investeringar och finans.

Att förstå knapphet hjälper oss att se hur resurser används, hur marknader fungerar och varför priser sätts som de gör. Oavsett om du tänker på globala resursutmaningar eller möjliga investeringsmöjligheter, är det viktigt att förstå hur knapphet påverkar beslutsfattandet.

Vad betyder knapphet?

Inom ekonomin syftar knapphet på det faktum att det finns en begränsad mängd råvaror, arbetskraft, mark och kapital, samtidigt som behoven och önskemålen hos individer, företag och hela samhällen är i princip oändliga.

Ur ett investeringsperspektiv kan knapphet visa sig i form av ett begränsat utbud av högkvalitativa aktier. Medan allt fler vill hitta lönsamma investeringar, finns det bara ett visst antal välpresterande bolag att satsa på.

Denna begränsning driver ofta upp priserna på attraktiva tillgångar, eftersom fler vill äga en bit av något som det finns lite av. Det innebär att investerare måste prioritera klokt – och väga potentiell avkastning mot högre kostnader.

Vad påverkar knapphet?

Ekonomer använder begreppet knapphet för att förklara varför vissa resurser som tidigare var lättillgängliga plötsligt blir svåra att få tag i. Det finns tre huvudorsaker till knapphet:

Efterfrågedriven knapphet

Detta sker när efterfrågan överstiger tillgången. Exempel: En ny populär spelkonsol släpps och säljer slut direkt eftersom så många vill ha den.

Utbudsdriven knapphet

Här är det yttre faktorer som påverkar tillgången, till exempel tillverkningsproblem eller naturkatastrofer. Ett exempel är chipbrist som påverkar hela elektronikindustrin.

Strukturell eller relativ knapphet

Denna typ av knapphet uppstår när vissa grupper har bättre tillgång till resurser än andra, ofta på grund av politiska eller ekonomiska ojämlikheter – inte på grund av resursens faktiska tillgång.

Knapphet i olika branscher

Knapphet påverkar olika branscher på olika sätt. Inom jordbruket kan torka eller dåliga skördar minska tillgången på livsmedel, vilket driver upp priserna och förändrar konsumentbeteenden.

Inom teknik kan brist på komponenter som mikrochip fördröja produktion, göra produkter dyrare och begränsa tillgången. I sjukvården kan brist på läkemedel eller utrustning höja kostnader och försvåra tillgången till vård.

Inom finans påverkar knapphet också kapitalfördelning. När det finns begränsat med kapital eller attraktiva investeringar måste investerare fatta strategiska beslut – vilket i sin tur driver upp priserna på eftertraktade tillgångar.

Hur påverkar knapphet oss?

I dagens samhälle påverkar knapphet alla – privatpersoner, företag och regeringar.

För privatpersoner innebär det svåra val kring vad pengarna ska användas till. Företag kan ha svårt att få tag på råvaror, vilket påverkar produktionen och priserna. Regeringar måste ta hänsyn till knapphet när de utformar politik, budgetar och samhällsprojekt.

Knapphet driver ekonomisk politik och påverkar hur resurser fördelas. Den formar också marknadsdynamiken – när tillgång och efterfrågan förändras påverkar det priser, utbud och efterfrågan i hela ekonomin.

Knapphet inom ekonomi

Ur ett investeringsperspektiv innebär knapphet att det finns ett begränsat utbud av en viss tillgång, samtidigt som efterfrågan är hög – vilket i sin tur kan driva upp priset.

Det kan handla om allt från naturresurser till populära kryptotillgångar. När något blir svårt att få tag på ökar ofta dess värde. Ett tydligt exempel är Bitcoin, som har ett maxutbud på 21 miljoner coins. När fler efterfrågar något som är begränsat i utbud, tenderar priset att öka.

Strategier för att hantera knapphet på marknaden

Oavsett om du investerar eller handlar aktivt, här är sex strategier att ha i åtanke för att navigera marknader där knapphet spelar roll:

- Diversifiera dina investeringar – Sprid dina investeringar för att minska risken om en bransch påverkas av brist.

- Välj stabila sektorer – Satsa på områden där tillgången på resurser är god och förutsägbar.

- Utforska nya marknader och teknologier – Håll ögonen öppna för innovation och framväxande sektorer.

- Tänk långsiktigt – Tillgångar som fastigheter eller råvaror kan behålla sitt värde över tid.

- Håll dig informerad – Följ marknadstrender, utbudsproblem och förändringar i efterfrågan.

- Fundera på hållbarhet – Investera i teknologier och lösningar som hanterar resurser på ett effektivt sätt och kan bidra till framtida stabilitet.

Observera: detta är endast generella förslag och inte finansiell rådgivning. Gör alltid noggrann research innan du fattar investeringsbeslut.

Slutsats

Knapphet är ett centralt begrepp inom ekonomi som visar klyftan mellan våra oändliga behov och världens begränsade resurser.

Det påverkar alla – från privatpersoner till företag och hela regeringar. Genom att förstå hur knapphet fungerar kan vi fatta bättre beslut, investera klokare, och använda våra resurser mer effektivt.

Knapphet formar vår ekonomi, våra marknader och våra möjligheter – att förstå det är nyckeln till att navigera dagens komplexa värld.

The financial industry has seen significant growth within its digital sector due to the adaptation required during Covid-19. With the increased interest in digital payments has come the rise of virtual cards.

Shopping online and online purchases continue to break barriers that traditional financial institutions never predicted. While these institutions do allow users to do online shopping, there are still a lot of limitations and risks to be wary of.

Every time you shop online, you risk your account number and details being stolen and used against you. Credit card companies have had to evolve, and one way they have done that is through the introduction of an actual account-linked virtual card.

How do virtual credit cards and debit cards work?

Virtual cards are stored on your mobile device and can be used to make contactless payments in store or online. A virtual card has its own unique card number, CVC, and expiration date. These virtual cards are simply a copy of your physical card, linked to your bank account, and stored on your application or phone. Think of it as an online account and card.

Virtual cards are very similar to an actual credit or debit card, with the main difference being that they only exist digitally, and can not be used to withdraw physical cash. Virtual credit cards provide the same features and mechanics as traditional credit and debit cards.

A virtual credit card still has an expiry date and 16-digit account number, and CVV codes. They are connected to payment networks like Visa and Mastercard and are generally accepted by merchants who use physical card machines, similar to Apple and Google Pay.

Your virtual card information and virtual credit card number are stored digitally, eliminating the risk of someone stealing your card and simply entering your details when shopping online.

Virtual credit cards act as digital wallets, providing more advanced security and ease of online access. Virtual cards are created for one-time use or act as a temporary account number, but what are the benefits of a limited-use virtual card number? Let’s get into it.

Benefits of a virtual credit card

The first and foremost virtual credit card feature benefit that you can expect is an enhanced layer of security. To combat fraudulent activity, a data breach, and account information being stolen, virtual cards have randomly generated and disposable card numbers. This makes virtual cards one of the safest payment methods, eliminating physical and confirmed details, meaning your temporary information can not be stolen or lost. If your info is compromised, you can cancel it without having to create a new bank account or waiting for a new card in the mail.

Control and customization is an additional layer of benefits users can expect from using virtual credit cards. Users can customize how many virtual account numbers they want, set spending limits, choose their preferred currencies, and more. Similar to a normal debit card account, you can also create recurring payments with merchant details, as tailored to the amount, time, and so on.

Some virtual credit cards provide users with point-earning rewards or store credit when used. Credit card companies can also easily access your information to improve your credit score based on your recurring payments set up.

Creating multiple virtual debit cards allows you to distribute, allocate, and track funds with ease. This means at the end of the day, you have more visibility of your funds going in and out and can create a dedicated virtual debit card for a specific area of your financial responsibilities.

Getting your virtual card number

Whether you are trying to manage your funds with your debit or credit cards accounts, a virtual card can make matters easier. All you need is a debit or credit card account, such as the one offered by Tap and you can create your unique virtual card at the click of a button. With some traditional banks you can even create multiple cards if you want, each with its own unique account number and expiration date.

These digital wallets and accounts provide ease when you want to shop online, avoid physical wallet and card theft, as well as easier fund management. A virtual debit card is a big part of the future, as we move into the digital era.

Experience a whole new world of digital payments and money management from the safety of your mobile device. You should be able to use your virtual card at any merchant that accepts debit and credit card payments, or contactless transactions, such as Apple Pay or Google Pay. Create your virtual account number today and enjoy purchases online and in-store. The future of payments is here.

In recent years, cryptocurrency, and therefore cryptocurrency exchanges, have firmly established themselves in the global financial market. As they become increasingly popular, many concerns have been raised over the regulation of these entities, and how they are preventing illicit monetary activity from taking place.

In an attempt to crack down on funds being illegally moved, exchanges are required to implement KYC (Know Your Customer) and AML (anti-money laundering) policies. Regulatory bodies are working to build legal frameworks for the industry, in an attempt to fight crime conducted using blockchain technology.

The biggest challenge for these regulatory bodies is to find a solution that doesn't hamper the innovative qualities of cryptocurrencies.

In the UK there is the Financial Conduct Authority, a financial regulatory body that operates outside of the UK government. In 2020, the FCA required every company participating in any crypto activity in the sector to comply with its Money Laundering, Terrorist Financing and Transfer of Funds (Information on the Payer) Regulations 2017 policy (the 'MLR's). This obligation requires crypto service providers to complete the necessary registration and infrastructural requirements.

What is AML in crypto?

AML stands for anti-money laundering and involves protocols that ensure that every transaction can be tied to an identity, thus providing greater transparency. This ensures that if any suspicious activity is flagged, the origins and/or destination of the funds can be confirmed on the platform.

Due to the anonymous, or more accurately pseudonymous, nature of cryptocurrencies, many believe that it provides an easy opportunity for ill actors to engage in money laundering. Money laundering is the act of changing large amounts of illicit income into a legitimate avenue, the money is "laundered" so as to appear clean.

While cryptocurrencies seemingly provide a perfect platform for money laundering due to the lack of central authority or third parties, AML processes are implemented on exchanges to stop this activity in its tracks.

What are the risks hindering AML practices?

The first risk that challenges AML practices is privacy coins, cryptocurrencies designed to conceal transactions and the relevant information attached to them. Platforms like Monero offer users the opportunity to send funds with no record of the transaction taking place.

The data associated with the transactions like the sender, receiver and amount sent are encrypted and often broken up when stored on the blockchain to ensure they are untraceable.

The second risk is coin join platforms that mix cryptocurrency transactions, hiding the origin and destination of the funds. These platforms essentially provide a service that can make ordinary cryptocurrencies anonymous.

While cryptocurrencies have their benefits, there are a number of challenges they pose to regulatory bodies, AML and CFT (Combating the Financing of Terrorism) intentions:

- The anonymity they can provide

- Opportunity for gaps when transacting cross-border transactions

- Absence of one central authority to ensure compliance

- The limited scope of identity verification processes

Differentiating between illicit activity and investors just wanting to safeguard their investments is a tricky business. Bad actors might make use of paper wallets to hide funds and keep them secret, while an investor might make use of a paper wallet in order to protect their funds against theft.

AML in crypto exchanges

Despite the challenges it faces, AML has proven to be valuable in cracking down on illegal activity conducted on crypto exchanges.

In July, $1.45 billion worth of illegal cross-border crypto transactions were traced back to 33 individuals on the South Korean exchange, Bithump. The platform quickly banned all foreign transactions, requiring a mobile KYC verification, and increased the KYC requirements so as to align with the country's AML regulations.

Bitcoin ATMs, a notorious option for mixing funds, have come together to form the Cryptocurrency Compliance Cooperative (CCC). This operation calls for cash-based cryptocurrency services, financial institutions, and regulators to participate in building universal compliance factors.

Does AML help or hinder the crypto market?

While AML tends to go against the decentralized nature of cryptocurrencies, the crypto community actively welcomes these regulatory efforts as it drives more trust and interest in the market on top of innovation and adoption. For example, an institution or retail investor is more likely to invest in a regulated asset than in a lawless, anything-goes market.

Anyone that has been watching the markets closely for the last several months will have noticed a definite chill in the air (not to mention a decline in their money). As the bears become more prominent, weak hands are losing faith and exiting the market. Why are we talking about a cryptocurrency winter now? Before we firmly declare this to be a crypto winter, let's explore the recent dips of the digital asset market and what previous crypto winters have detailed.

What is a cryptocurrency winter?

A cryptocurrency winter is a term used in the crypto market to describe a long term bear market. A bear market is classified as a declining market where shares have fallen below 20%. Investors typically call it a crypto winter when the markets have struggled to reclaim highs previously witnessed (usually right before the winter set in). Does that mean cryptocurrency investors should take out their snow shoes? Metaphorically, yes. And by snow shoes we mean thick skin and strong hands.

The recent market climate (five month period).

Since reaching its most recent all-time high, Bitcoin has dropped over 40%. After reaching highs of $68,789.63 in November 2021, Bitcoin has gone through a red-tainted slump reaching lows of $33,710 in late January and since recovering to just under the $40,000 mark.

Ethereum, the second-biggest cryptocurrency, has experienced a similar fate, dropping from highs of $4,891 in November 2021 to lows of $2,211 in late January. Ethereum has since corrected to the $2,800 region as it generates interest in its move to a Proof-of-Stake consensus.

It's no secret that the stock markets have suffered a similar fate in recent months, with seemingly only gold remaining unscathed. Experts have suggested in various articles that the uncertainty in global politics is playing a considerable role in the decline of various markets and businesses.

Buterin confirms a crypto winter

As touched on above, the current ongoing war between Russia & Ukraine has played a large role in driving investors' uncertainty as prices bounce through the highly volatile period. While we've seen an increase in trading volume, there have also been strong price swings.

This paired with the declining prices has led to a downfall in companies and traders entering the market, further fuelling the problem. This has become known in the industry as a crypto winter.

Ethereum founder, Vitalik Buterin, recently confirmed the case, although he also highlighted the positives, particularly for those on the development side. He pointed out that crypto winters offer a period of rejuvenation for the industry, allowing unsustainable projects to fall away.

"They welcome the bear market because when there are these long periods of prices moving up by huge amounts as it does - it does obviously make a lot of people happy - but it does also tend to invite a lot of very short-term speculative attention."

He added that it encompasses a "time when a lot of those applications fall away and you can see which projects are actually long-term sustainable, like both in their models and in their teams and their people." If one factors the development side of things in, we can bank on the industry coming out stronger after this period.

Unwrapping the previous crypto winter

The last crypto winter we experienced took place in 2018 after the highs of December 2017 (when Bitcoin almost reached $20,000). This bear market continued until mid-2019 before it started showing signs of recovery. It wasn't until Bitcoin defied the odds in 2020 and overcame the pandemic that it soared to higher heights, almost triple that of the previous all-time high.

While losing 40% of its value this season sounds rough, the previous crypto winter saw losses of 84%. As cryptocurrencies further emerge themselves into the mainstream financial markets, many believe it is only a matter of time before the prices enter the green again. Time also tends to play a regulator role when it comes to changing crypto seasons.

Bitcoin's four year cycle theory

There is a growing belief in the industry that Bitcoin has a definitive four-year cycle of prices rising and falling. This aligns with the halving mechanism which takes effect every 210,000 blocks, or roughly every four years.

The halving, the last of which took place in May 2020, halves the rewards given to miners for verifying transactions and effectively halves the number of new coins entering circulation. History has shown that a bull run succeeds these events, roughly twelve to eighteen months later.

Surviving the chill

While many can agree that the crypto winter is upon us, there is no saying how long it might last, or how low it may go. Analysts suggest that traders use the time to sharpen their investment strategies and implement plans of action that keep risk to a minimum. As blockchain and cryptocurrencies have already passed a significant milestone in their adoption, there is no stopping it now. For any traders concerned over the crypto winter, fear not. It will pass.

It's 2025 and you've decided to get involved in the crypto industry and find out what the fuss is all about. You've made a smart choice, and we're pleased to welcome you. In this step-by-step guide, we'll be showing you a simple overview of how to complete the following:

- Create an account

- Deposit funds

- Buy Bitcoin, Ethereum or any other cryptocurrency

- Sell a cryptocurrency

- Withdrawal funds

Investing in digital currencies can feel daunting at first, but once you've made your first purchase, transaction, or sale, you'll see that using cryptocurrencies is simpler than expected. Be sure to keep an eye on market prices, as volatility in the crypto industry can go through waves, and educate yourself on the coins that you wish to purchase. Whether you're a trader/investor in the UK, EU, EEA, or USA, everyone can gain access to the crypto markets through the Tap mobile app.

In this article, we're going to show you the ropes, guide you through the process and explain step-by-step how to gain the skills to successfully operate in the crypto space and increase your investment portfolio. No previous trading experience is necessary (stocks or crypto).

Step 1: create an account

The first and most important decision to make before buying cryptocurrencies is determining where to buy them from. With plenty of options available on the market and plenty more news stories about them, it's imperative that you select a trustworthy and reliable source.

The Tap mobile app ticks these boxes and proves so by being licensed and regulated by the Gibraltar Financial Services Commission. The platform has over 300,000 registered users, at the time of writing, operates in 28 countries across the globe, and has been nominated multiple times for PAY360 Awards (previously the Emerging Payments Awards).

To create an account on Tap, simply follow these steps:

- Download the Tap mobile app from either the Apple or Google Play store.

- Create an account by filling in the relevant information. If you make a mistake, simply go back and alter it before moving to the next step.

- Once the account is set up you will be asked to complete the KYC / identity verification process. Simply follow the onscreen prompts and submit the required information.

- You will receive an email confirmation once your account is all set up.

Step 2: deposit funds

In order to buy cryptocurrency through the Tap app, you will need to deposit funds. This can be done in both crypto and fiat currencies, however, we will focus on the fiat deposits today.

- Select the Cash option in the top horizontal menu.

- Select the fiat currency you would like to deposit, your options are US dollars, Pound Sterling, or Euros.

- We're selecting GBP, then select one of the options: deposit or debit card top-up.

- Fill in the relevant information and perform the transaction.

- Once the funds have cleared they will appear in the relevant Cash wallet.

Step 3: Buy Bitcoin, Ethereum, or any other cryptocurrency

Now for the exciting part! It's time to buy digital currency. For the sake of this tutorial, we're going to show you how to buy Bitcoin, however, the process is consistent across all cryptocurrencies.

- In the top horizontal menu, select Cryptocurrencies.

- Choose the cryptocurrency you would like to purchase.

- Once in the crypto wallet, select the blue Buy button.

- You'll be given the option to decide how to pay, simply scroll to the bottom and select Pound Sterling (or the crypto or fiat currency that you deposited).

- Enter the amount that you would like to purchase.

- Select the Execute Trade button.

- Once the transaction is completed, the funds will appear in your Bitcoin wallet.

Step 4: Sell A Cryptocurrency

Now that you're familiar with how to buy crypto, it's high time you learned how to sell.

- To sell Bitcoin (or any other cryptocurrency), go to the relevant wallet in the Crypto section.

- Select the blue Sell button.

- From here you can decide whether you'd like to sell the cryptocurrency for another cryptocurrency or for a fiat currency. In this example, we'll sell BTC for GBP.

- Select the Pound Sterling option and enter the amount of BTC you'd like to sell.

- Proceed with the Execute Trade button.

- The funds will then be available in your Cash GBP wallet.

Step 5: Withdrawal Funds

Completing the final process in this step-by-step guide, we're going to explain how to withdraw funds. You have several options here as the Tap app allows users to withdraw funds directly into their bank account, instantly send funds to other Tap users, or withdraw cryptocurrencies.

- In the top horizontal menu, select Cash.

- Choose the Withdraw button, located underneath your balance.

- Select the option most preferable to you: Instant, to a Tap user; bank transfer; Crypto withdrawal.

- Follow the relevant instructions and select Execute Trade once complete.

Tap into a brighter future with crypto

On top of the simple and easy-to-use app, Tap also offers highly secure wallet solutions that are integrated into your account from the get-go. With Tap, you can securely store and manage a wide range of cryptocurrencies from one convenient location, and even more easily spend them using the Tap card.

Bitcoin 101

Here are several frequently asked questions regarding Bitcoin, the first cryptocurrency to come into existence.