November 2025 could be a turning point for crypto. From ETFs to major network upgrades, here are six catalysts that could shape the market.

Keep reading

As we move into November 2025, the crypto-market is gearing up for one of its most intriguing phases yet. From spot-ETF momentum to narrative shifts, network upgrades and real-world asset tokenization, multiple catalysts are aligning. Here are six key developments to watch.

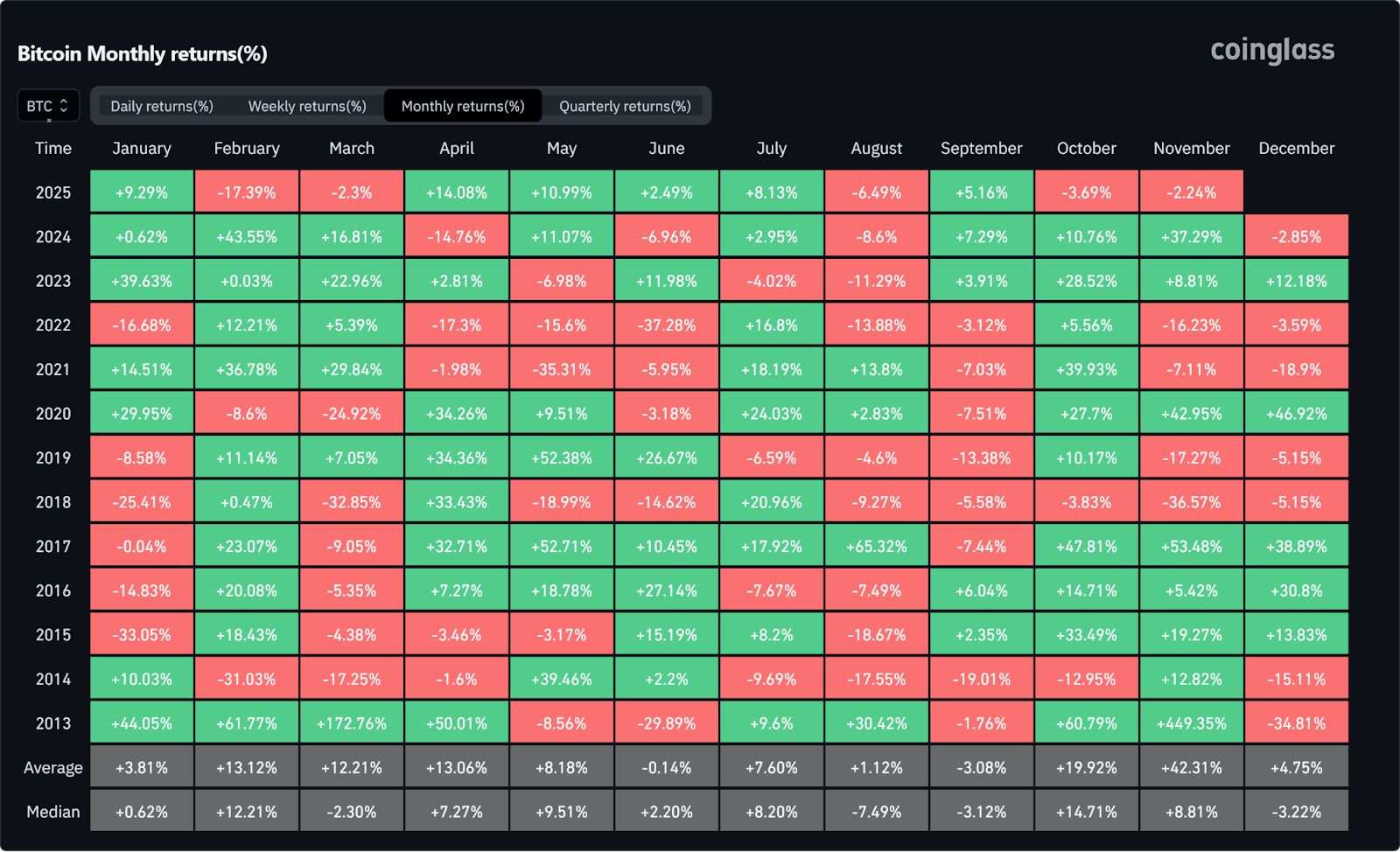

1. Seasonality & Historical Momentum Could Kick In

While "Uptober" fell short of expectations, November could tell a different story. Historically, it's been one of the strongest months for digital assets, with Bitcoin in particular averaging +42.31% gains in recent years.

When combined with the renewed ETF narrative, increased whale accumulation, and a stronger appetite for risk assets, market momentum appears to be building. Participants are closely monitoring how these dynamics could influence sentiment, especially as trading volumes and key technical levels come into play. If Bitcoin maintains stability around the $100K zone and Ethereum shows signs of renewed strength, November could become a more active month for crypto markets compared to October.

2. Ether’s Next Move Could Set the Tone for Altcoins

The final weeks of 2025 may prove pivotal for Ethereum (ETH). Although retail accumulation has paused somewhat, wallet-level data shows large holders (1,000 to 100,000 ETH wallets) added roughly 1.6 million ETH in October (around $6 billion), it’s a sign that whales and larger holders are staying active as the year winds down.

If ETH begins to break out or even stabilize around current levels, it could unlock the broader altcoin market, which has been lagging for months. The playbook that many are hoping for is the following one: ETH strength leads to improved risk appetite, which in turn sparks an altcoin rotation as investors seek higher risk exposure.

Ethereum remains the accepted benchmark for gauging sentiment across the non-Bitcoin segment of the market, and its performance frequently acts as a catalyst for capital flows into smaller assets. Keeping an eye on its fundamentals (from staking yield to liquidity shifts on major exchanges) will be important. In many ways, ETH could potentially become the gatekeeper to the next phase of the market’s recovery and the tone-setter for the coming months.

3. ETF Comeback After Delays

The recent U.S. government shutdown briefly froze several crypto-spot ETF filings, leaving the “ETF narrative” in suspense. But now the pause is over for Bitwise’s Spot Solana ETF. It has finally launched with strong early inflows, and the broader momentum is returning.

With this foundation, November could reignite the ETF trade in earnest, we may finally see filings for Ethereum staking products, new spot-Bitcoin funds and renewed institutional interest. If filings begin to stack up and regulatory engagement deepens, this could mark the next major inflection for how crypto is accessed in traditional portfolios.

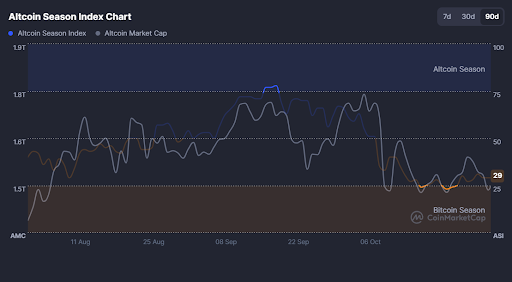

4. Altcoins at an Inflection Point

The broader altcoin sector enters November under pressure as the Altcoin Season Index sits near 29, signaling a reset after October’s downturn. But inflection points often follow pressure. If ETH sets the tone (as many are hoping for), mid-cap and high-beta altcoins (such as SOL, AVAX, NEAR) could begin to capture rotation flows.

Traders might want to watch for flow changes such as increased volumes, wallet relocations and new project launches. While caution is still prevailing, this may be the window where sentiment begins to swing back into “altcoin season”.

5. Major Network Upgrades

Technical infrastructure is not just background noise; it often creates catalyst-events. For example, Ethereum’s upcoming Fusaka Upgrade (scheduled for early December) is designed to increase layer-2 data capacity and reduce transaction costs.

Meanwhile, various Layer-2 ecosystems are preparing upgrades and cross-chain activations. One such upgrade, Shibarium Upgrade’s security overhaul on the Shiba Inu network. These events may ignite renewed network activity, developer interest and capital flows into ecosystems ready to scale.

6. Real-World Asset (RWA) Tokenization Accelerates

The tokenization of real-world assets (RWAs), such as real estate, bonds, equities, is moving from niche to mainstream. For instance, according to Standard Chartered, this market is projected to grow to around $2 trillion by 2028. Institutional interest is burgeoning, and regulatory frameworks are emerging.

As November unfolds, we may see announcements of large tokenization initiatives or new platforms bridging DeFi and traditional finance. For crypto holders and ecosystem observers, this means the familiar “crypto only” narrative is expanding into real-asset integration, a meaningful broadening of the opportunity set.

The Verdict

November 2025 is shaping up to be more than just another month. Spot-ETFs potential, ETH’s path, altcoin rotation, seasonal tailwinds, infrastructure upgrades and RWA tokenization all sit in motion. Each one individually is significant; together they create a multi-vector setup.

For those in the crypto space, whether you're holding long-term, actively trading, or building the next wave of infrastructure, November is likely to be eventful. This isn't a month to coast on autopilot. Track where capital is flowing. Pay attention to which narratives are gaining momentum and which are fading. The players are moving, and the pieces are falling into place.

NEWS AND UPDATES

LATEST ARTICLE

You might have come across the term p.a. in traditional investment cycles, but how does it relate to crypto? In this article, we’re breaking down what p.a. means, how to get in on it and how it relates to the crypto industry.

What does P.A. mean?

P.a. is an investment term that stands for per annum. This refers to the interest an investor can gain over a year's period and provides insight into the yields that the investment will generate. This is calculated on a simple basis and not compound.

You might see digital wallet platforms offering reward rates of 8% p.a. Or 14% p.a., this tells the potential investor that the platform will provide 8% of the initial investment, over a 12 month period.

PA can also stand for price action, a popular term used on crypto Twitter. In this piece we're focusing on the annual interest rates version.

How can users make money with crypto assets?

There are several ways in with industry participants can earn cryptocurrency. Below we outline the most widely used, and safest options. Be sure to check each option with the relevant blockchain network as these will differ from network to network.

Crypto Mining

Crypto mining can be a lucrative means of generating a passive income, however, the costs might run high depending on where you live and what cryptocurrency you are mining. Each network has its own way of minting new coins, which require different hardware and electricity means.

Bitcoin, for instance, is a Proof of Work network that requires miners to use large amounts of energy as they race to finish a complex cryptographic puzzle. The first to complete this is rewarded with mining the next block and receiving the associated payoffs.

Bitcoin requires a large amount of electricity, not practical in areas with high electricity costs, and either a graphics processing unit (GPU) or an application-specific integrated circuit (ASIC), which can also be costly.

If you wish to get involved with mining cryptocrrencies be sure to do adequate research on what will be required and what income this could generate before investing any money.

Crypto Staking

Crypto staking is an alternative minting solution for Proof of Stake networks, such as Cardano and soon-to-be Ethereum. Crypto staking requires users putting their funds in a smart contract usually for a predetermined lock up period to confirm transactions on the network. This will typically require a minimum amount, so as to ensure that individuals hold a “stake” in the network and will act on good intentions.

When crypto traders stake the minimum balance, a node will deposit these funds into a staking pool on the network, similar to a deposit. The bigger the stake, the higher the chances of that user, now referred to as a node, being chosen to verify transactions. When the node is chosen to confirm transactions, they will create a new block and receive a reward for adding it to the blockchain.

Reward rates are specific to each blockchain network so be sure to check the details relevant to platform on which you wish to stake. As a security mechanism, the staked coin in the network is typically taken away if the node acts with ill intent.

Passive Income

There are a number of crypto initiatives that allow users to earn passive income through their crypto assets. These work in a similar way to holding funds in a wallet, however, these wallets will likely be on a cryptocurrency exchange or DeFi wallet and the user will typically not be able to access the funds for a certain period of time.

Over the duration the user will earn interest as stipulated in the initial agreement. Note that p.a. Values are subject to change with market fluctuations, rising when prices rise and falling when an asset’s price takes a dip. This typically works in the same way as a savings account.

Its worth noting that the onus lies on the traders to pay taxes on any income generated. It is important to check the crypto specific tax laws in your region.

Disclaimer: This article is intended for communication purposes only, you should not consider any such information, opinions, or other material as financial advice.

When referring to the yield on an investment, this indicates the earnings generated over a certain period of time. It is generally presented in percentage form and includes the interest or dividends relevant to the initial investment.

While returns are calculated using the difference in value at two specific points in time, the yield will calculate the total (net) value earned over a period of time. This provides an invaluable tool in helping you understand the potential value of an investment.

Basic yield is calculated as the net realised return divided by the initial investment amount. For example, if an investor bought $100 worth of Bitcoin which grew to $2,000 in the next year, then the formula would look like this:

$1,900 / $100 = 19

-> which translates to 1900%.

There are several different formulas based on the type of yield you wish to calculate. These include:

- Yield on Stocks

- Yield on Bonds

- Yield to Maturity

- Yield to Worst

- Yield to Call

A high yield isn’t necessarily a good thing. Should the market’s decline or the company pays out high dividends the yield will still reflect as high. Always do your own research when considering an investment, or trust a financial advisor.

Since stablecoins emerged in the crypto sphere, many have questioned their legitimacy. While cryptocurrencies are perhaps more frequently used as a tool for value storage rather than a means of transaction, coins (or any financial products) that cannot appreciate in value certainly raise several questions. So why have stablecoins become so popular among businesses and individuals alike? Below we're taking a look at their use cases and reporting on whether they're the safe haven of crypto.

What are stablecoins?

Before we continue, let's clarify what stablecoins are. These types of cryptocurrencies are "stable assets" that have their value pegged to a fiat currency or commodity. This might include the US dollar, Euros, the price of gold or even other cryptocurrencies. So while Bitcoin (BTC) and Ethereum (ETH) are subject to bouts of volatility, stablecoins remain consistent with the price of the money they are pegged to.

Stablecoins are not to be confused with CBDCs (central bank digital currencies) which are operated by a government-controlled organisation, usually a country's national bank. Stablecoins are controlled by a company and utilise blockchain technology to facilitate transactions, store the relevant data and maintain security.

Stablecoins' economic policy ensures that they maintain their value through the use of smart contracts, algorithms and reserves. For each Tether in circulation, for example, one US dollar needs to be held in a reserve account. These types of cryptocurrency tokens provide a reliable and non-volatile means of making payments with the companies issuing them regulating the circulating supply.

What value do Stablecoins provide?

While many might not initially see that value in a fiat-pegged cryptocurrency, stablecoins are actually hugely useful in a largely volatile market. Let the current top 5 biggest cryptocurrencies based on market cap in the industry be an indication, with two of the five being stablecoins.

As stablecoins utilise blockchain technology, the coins naturally inherit all the characteristics of seamless and fast digital transactions (as well as transparency when it comes to transactions). Much like traditional digital assets, stablecoins can be transferred across borders instantly, a much faster and cheaper alternative to using fiat currencies and without the chance of price swings. Users, whether consumers or businesses are able to buy, store and sell stablecoins as they would any other cryptocurrency on the market.

For example, should you wish to pay a business in another country for services rendered or any other expense, it would prove to be much faster and cheaper to use a stablecoin than to send your local currency via traditional banking services. Stablecoins offer a much more streamlined means of completing the job.

Stablecoins also provide an entry into exchanges that don't work with fiat currencies, providing a reliable means of trading on those platforms. Stablecoins have also come to be known as "risk-off" assets, giving newer traders a chance to "test" the markets without the volatility.

This innovation in the blockchain space has opened many new markets to the use of cryptocurrencies, certainly more mainstream markets across a wide range of countries. As information regarding how they work spreads, more businesses have opened their mind to using them in everyday working life. Stablecoins have also become a popular option with users trading on DeFi (decentralised finance) platforms, providing a secure and efficient means of using the products.

Are stablecoins the safe haven of crypto?

In essence, yes. Since the advent of stablecoins (marked by the launch of Tether) in 2014, there has been a number of new stablecoins to emerge, resulting in more confidence in crypto markets. This has equated to more movement and trade volume, and a lower risk management sector.

So while one isn't going to make huge returns (if any) on stablecoins, they bring value to the market due to their stability and transaction ability.

As stablecoins are used by traders to hedge against falling markets, they provide a safe haven for their digital funds until the markets return to normal levels. Businesses around the world use stablecoins as they provide a faster and cheaper means of settling bills, allowing them to harness the power of blockchain technology without the worry of prices rising or falling in a short space of time.

Tap into stability

Tap can support your market entry endeavors by providing a platform to include a variety of assets in your portfolio. Whether you're considering accumulating stablecoins during market shifts or looking to engage in various transactions, Tap offers a streamlined experience. You can easily acquire, sell, trade, store, and manage widely utilized stablecoins like Tether (USDT) and USD Coin (USDC), all from a single secure platform.

The global financial crash in 2007 was the catalyst for the creation of Bitcoin. Designed to provide a decentralized way in which people can manage their own money, digital currencies slowly infiltrated the greater financial markets.

Almost a decade later, crypto adoption is at its highest and for the first time challenging traditional financial institutions and their product range. So, which is better? Let's explore the pros and cons of each category.

Blockchain technology has seen an incredible increase in interest in the last few years. While it provides a universal backbone relevant to almost any industry, it has also brought the world cryptocurrencies, NFTs, decentralized finance (DeFi) and other digital assets.

Tackling existing centralized monetary challenges, blockchain technology and digital currencies are two of the greatest inventions of the 21st century.

Digital currency versus banking

Cryptocurrencies are decentralized digital currencies that can be used to exchange goods and services as well as a store of value. They're typically acquired through crypto exchanges and kept in secure crypto wallets. These virtual currencies are autonomous, operate in a secure manner with little human interaction, and are increasingly considered the future of finance.

The predominant financial systems in the world are currently banks. They provide financial services to those that meet their requirements, including loans, savings, and other financial services.

However, unlike cryptocurrencies, they have several problems core to them being centralized and susceptible to biases. They're also slower than cryptos, and some of them charge exorbitant interest rates on loans as well as routine purchases.

The pros and cons of the Banking system vs digital currencies

There has been little development in the banking sector in the last several decades, so while the products are useful there has been very little innovation in the space. Below we outline the current challenges that the traditional systems face when compared to the advantages of a digital currency.

Financial Inclusivity

Banks are notorious for requiring lengthy paperwork and in-depth background checks. They are also known to provide different products and limits to different groups of people, including payment durations, soft loans, limits, etc.

When creating the digital currency Bitcoin, Satoshi Nakamoto wanted to counteract this financial inclusivity pertaining to fiat currencies and the greater financial system and instead provide a financial product available to all. Cryptocurrencies, therefore, do not require any paperwork or identification to operate or open a digital wallet.

While buying digital assets on an exchange will require personal information, they do not require any background checks or credit scores. Unlike in the traditional financial system, engaging in crypto markets is also not exclusive to location, allowing anyone from any corner of the globe to immediately access the digital payment systems.

Accessibility

Banking institutions operate within certain hours and are closed on weekends, meaning that transactions can sometimes take days to clear. They will also typically require an in-person authentication for very large transactions, and affect the remittance markets in the global financial system.

Cryptocurrencies on the other hand operate 24/7 (even on public holidays) as they are maintained by members all around the world. Cryptocurrencies provide zero downtime with unlimited amounts and do not require third-party authentication before making transactions. One digital currency can send value to the other side of the world in minutes, requiring no in-person authentication.

Security

The banking industry, particularly online systems, are susceptible to being hacked, alongside fraudulent activities and money embezzlement. While this is not always the direct fault of the central bank or financial institutions, it has become a common problem as ill actors have learned how to navigate the security systems and trick the owners of these accounts.

Through the use of blockchain technology, transactions cannot be intercepted or reversed, and are handled in a peer-to-peer nature ensuring that they do not go through a third party for authentication and require minimal human interference.

Fees and Transaction Times

During transaction periods, banks often add on extra costs and taxes. When sending and receiving money, banks frequently charge very high transaction fees and taxes, especially when conducting international remittances. These transactions also take a long time to clear due to their sluggish procedures, especially for large amounts of cash.

Cryptocurrencies provide an excellent solution to the remittance markets as they provide fast and cheap transactions. Blockchain technology ensures that they clear in several minutes (depending on the cryptocurrency and the network’s congestion at the time) and that they are sent directly to the recipient’s wallet (as opposed to waiting for the receiving bank to clear the transaction).

Diversification

Traditional banking services generally lack significant diversification options due to their competitive pricing structures. However, cryptocurrencies enable users to engage with multiple products simultaneously, which can provide opportunities for leveraging various networks and creating portfolios with reduced risk concentration.

Smart Contracts

Another advantage that blockchain currently holds over traditional banking systems is the use of smart contracts. Smart contracts are digital agreements that automatically execute once predetermined criteria have been met. Leveraging smart contracts in the financial services industry offers a seamless and entirely decentralized approach to modern banking.

Which is Better: The central bank or digital assets?

Comparing central banks and digital assets reveals intriguing aspects of both systems. Banking systems have become an integral part of modern society, underpinning economies and facilitating everyday financial transactions. They offer stability, regulatory frameworks, and familiarity to the masses.

On the other hand, cryptocurrencies introduce a realm of innovation. Their decentralized nature challenges traditional financial paradigms, enabling secure and direct peer-to-peer transactions. Additionally, cryptocurrencies empower novel applications such as smart contracts, decentralized finance (DeFi), and tokenization of assets.

Selecting one over the other isn't straightforward due to their contrasting strengths. Central banks provide stability and a well-established foundation, while digital assets spark possibilities for disruption and financial inclusivity.

Presently, these financial systems coexist synergistically. The banking system maintains its role as a bedrock for economic operations, while digital assets complement by offering alternative avenues for value exchange and financial exploration. As both systems continue to evolve, it's likely that their interaction will shape the financial landscape in intricate and unexpected ways.

Why not use both? Tap offers the perfect solution to merging the best of both worlds through an innovative alt-banking mobile app. Through the app, users can load both fiat and cryptocurrencies into their unique, secure digital wallets and use both interchangeably to pay bills, send money to friends, and even earn interest. Get the best of both worlds by enjoying the benefits of both the traditional banking systems and cryptocurrencies.

Why not harness the strengths of both paradigms? Embracing this dual approach, Tap presents a groundbreaking solution that seamlessly blends the attributes of both money accounts and digital assets within an innovative mobile application. Tap empowers users to effortlessly load fiat currencies alongside cryptocurrencies into their individualized, secure digital wallets.

This fusion enables users to fluidly alternate between these assets for various purposes, such as settling bills, conducting peer-to-peer transactions, and even capitalizing on interest-earning opportunities. By embracing this convergence, you can truly enjoy the advantages offered by both traditional finance and the dynamic potential of cryptocurrencies.

We are delighted to announce the listing and support of Lido (LDO) on Tap!

LDO is now available for trading on the Tap mobile app. You can now Buy, Sell, Trade or hold LDO for any of the other asset supported on the platform without any pair boundaries. Tap is pair agnostic, meaning you can trade any asset for any other asset without having to worries if a "trading pair" is available.

We believe supporting LDO will provide value to our users. We are looking forward to continue supporting new crypto projects with the aim of providing access to financial power and freedom for all.

Lido's liquid staking service allows users to tap into the benefits of staking rewards without compromising their tokens' liquidity. Lido aims to empower users to put their staked assets to use, supporting a number of PoS cryptocurrencies. The platform offers a liquid staking solution that provides users with a system that allows them to earn rewards on staked coins while also receiving a tokenized version of the staked coins which can generate returns in other DeFi protocols.

The Lido DAO token (LDO) is an ERC-20 token, the native utility token to the Lido protocol used to reward users. The token has a total supply of 1 billion tokens and serves three primary functions.

The LDO token grants holders with governance rights in the operations of the Lido DAO, as well as the removal or addition of Lido node operators and helping with the management of fee parameters and distribution.

Get to know more about Lido (LDO) in our dedicated article here.

The Curve protocol and Curve DAO token form another innovative project to come from the DeFi movement and one that provides a particularly unique and well-designed concept. Improving on functionalities that DeFi platforms like Uniswap and Sushiswap have otherwise neglected, Curve focuses on providing a viable alternative solution to traditional financial platforms in the blockchain industry.

The Curve Finance platform, launched in January 2020, later released a decentralised autonomous organisation (DAO) alongside the Curve DAO token eight months later. CRV functions as the in-house token of the platform.

What Is Curve DAO (CRV)?

The Curve platform, formally known as Curve Finance, provides traders with a decentralised exchange on which to swap digital assets. Curve aims to provide minimum price slippage between two tradable crypto assets by focusing on stablecoins or assets of similar value. Through an automated market maker (AMM) and focused smart contracts, the decentralised exchange is able to manage liquidity.

While the platform can be compared to Uniswap, in reality, it has some key differences and a much higher amount of locked liquidity. The platform and its liquidity providers are more focused on stablecoins and other coins of that nature. CRV tokens fuel the network and are a tradable asset for crypto users.

The Curve DAO provides more decentralised governance to Curve's trading platform. The Curve protocol has grown into a well-respected financial asset within the DeFi ecosystem with its strong DeFi protocol.

Who created the Curve protocol?

The Curve platform was created by a Russian scientist with ample experience in the crypto industry. Michael Egorov both founded the platform and acts as its CEO. He previously co-founded a crypto business focused on building privacy-oriented protocols and infrastructure, NuCypher, in 2015, as well as LoanCoin, a decentralised bank and loans network.

As of August 2020, Egorov holds 71% of the governance tokens after locking up a large amount of CRV tokens in response to yearn.finance’s increasing voting power in the Curve network. In a statement made later, Egorov admitted to “overreacting”.

How does Curve work?

Launched prior to Uniswap V2, Curve Finance operates similarly to the DeFi platform but has implemented some key differences. The decentralised exchange differentiates itself from the original AMM platform by innovating the liquidity pool trading structure and relevant smart contracts.

The Curve DAO trading platform is managed by a mathematical function called a bonding curve, which is designed to let cryptocurrencies trade for the best possible price amongst each other. Bonding curves are also used by other DeFi trading platforms, like Uniswap.

Due to the Curve DAO platform being primarily focused on stablecoins, its bonding curve is specifically focused on these pegged digital currencies and is able to trade a larger amount of stablecoins with less change in their relative prices in a liquidity pool.

Lending pools

In order for the Curve DAO platform to operate, it requires a group of users who are willing to lock up their cryptocurrencies in order for them to be traded by others. The platform provides a return on their coins plus a portion of the fees from trades when incentivizing liquidity providers.

The platform manages the coins in the liquidity pools by making them more expensive or cheaper, based on their fluctuating amounts, thereby making them more attractive to buyers and sellers using the platform.

On Uniswap, liquidity pools are based strictly on predetermined trading pairs while on Curve DAO the liquidity pools comprise multiple assets. On Curve DAO, entire liquidity pools can also be used as an asset inside another liquidity pool.

How does a trader use the liquidity pools?

Once a trader adds liquidity to a specific pool, through stablecoins or other digital assets, the user will receive a token specific to that pool. 3pool is an example of one of the most popular liquidity pools on the Curve platform.

While the platform is known to provide trading for stablecoins, it also supports mirrored assets such as renBTC and wBTC. These assets are both built on the Ethereum blockchain and track the price of Bitcoin in a typical derivatives fashion. Since the prices are close in value they can function in the same pool and be traded using the Curve DEX.

What is the Curve DAO token (CRV)?

The CRV token is the utility token and governance token of the Curve DAO platform, providing users with governance rights, an incentive structure for fee payments, as well as providing long-term rewards to liquidity providers. CRV tokens are awarded to users based on their liquidity commitment and length of ownership.

The Curve DAO token was launched alongside the Curve DAO in August 2020. The maximum supply is 3.03 billion CRV tokens, with 62% of that being distributed to liquidity providers. The rest is allocated between employees (3%), and shareholders (30%), and a small percentage is kept for community reserves (5%). Employee and shareholder allocations work off of a two-year vesting schedule.

At the time of writing, over 531 million CRV tokens are in circulation, roughly 16% of the total supply. The market cap at the time was around $365 million, positioning the Curve DAO token network in the top 20 biggest platforms in the DeFi ecosystem.

How can I buy Curve DAO tokens?

If you’d like to buy Curve DAO tokens to include in your crypto portfolio, you can do so easily through the Tap mobile app. Providing a highly secure and equally simple crypto trading platform, users can buy CRV with British Pounds or Euros, or exchange tokens for other cryptocurrencies supported on the platform such as Bitcoin or Ethereum.

Simply download the app, create an account and follow the steps to get verified through the KYC process. You will then have access to several wallets, and a much simpler crypto trading experience.