Some crypto companies are fully compliant, fully regulated, and still can't keep their bank accounts. Learn why the financial system is quietly freezing them out.

Keep reading

Why can't a fully compliant, regulated crypto business secure a bank account in 2025?

If you're operating in this space, you already know the answer. You've lived through it. You've submitted the documentation, walked through your AML procedures, and demonstrated your regulatory compliance… only to be rejected. Or worse still, waking up to find your existing account frozen, with no real explanation and no path forward.

This isn't about isolated cases or bad actors being weeded out. It's a pattern of systematic risk aversion that's creating real barriers to growth across the entire sector, and it's throttling one of the most significant financial innovations of our generation.

We're Tap, and we're building the infrastructure that traditional banks refuse to provide.

The Economics Behind the Blockade

Let's examine what's actually driving this exclusion, because it's rarely about the reasons banks cite publicly.

The European Banking Authority has explicitly warned against unwarranted de-risking, noting it causes "severe consequences" and financial exclusion of legitimate customers. Yet the practice continues, driven by two fundamental economic pressures that have nothing to do with your business's actual risk profile.

The compliance cost calculation

Financial crime compliance across EMEA costs organizations approximately $85 billion annually. For traditional banks, the math is simple: serving crypto businesses requires specialized expertise, enhanced monitoring, and ongoing due diligence. As a result, it's cheaper to reject the entire sector than to build the infrastructure needed to serve it properly.

The regulatory capital burden

New EU regulations impose a 1,250% risk weight on unbacked crypto assets such as Bitcoin and Ethereum. This isn't a compliance requirement; it's a capital penalty that makes crypto exposure commercially unviable for traditional institutions, regardless of the actual risk individual clients present.

In the UK, approximately 90% of crypto firm registration applications have been rejected or withdrawn, often citing inadequate AML controls. Whether those assessments are accurate or not, they've created the perfect justification for blanket rejection policies.

The result? Compliant businesses are being treated the same as bad actors; not because of what they've done, but because of the sector they're in.

The Real Cost of Financial Exclusion

Financial exclusion isn’t just an hiccup; it creates tangible operational barriers that ripple through every part of running a crypto business.

Firms that have secured MiCA authorization, built robust compliance programs, and met regulatory requirements can find themselves locked out of basic banking services. Essential fiat on-ramps and off-ramps remain inaccessible, slowing payments, limiting growth, and complicating cash flow management.

Individual cases illustrate the problem vividly as well. Accounts are closed because a business receives a payment from a regulated exchange. Others are dropped with vague references to “commercial decisions,” offering no substantive justification. Founders frequently struggle to separate personal and business finances, as both are considered too risky to serve.

The irony is striking. By refusing service to compliant businesses, traditional banks aren’t mitigating risk; they’re amplifying it. Forced to operate through less regulated channels, these legitimate firms face higher operational and compliance risks, slower transactions, and reduced investor confidence. Over time, this slows innovation, and raises the cost of doing business for firms that are legally and technically sound.

Debanking Beyond Europe: U.S. Crypto Firms Face Their Own Challenges

Limited access to banking services isn’t exclusive to Europe. Leading firms in the U.S. crypto industry have faced numerous challenges regarding the banking blockade. Alex Konanykhin, CEO of Unicoin, described repeated account closures by major banks such as Citi, JPMorgan, and Wells Fargo, noting that access was cut off without explanation. Unicoin’s experience echoes a broader sentiment among crypto executives who argue that traditional financial institutions remain wary of digital asset businesses despite recent policy shifts toward a more pro-innovation stance.

Jesse Powell, co-founder of Kraken, has also spoken out about being dropped by long-time banking partners, calling the practice “financial censorship in disguise.” Caitlin Long, founder of Custodia Bank, recounted how her institution was repeatedly denied services. Gemini founders Tyler Winklevoss and Cameron Winklevoss shared similar frustrations.

These experiences reveal a pattern many in the industry interpret as systemic risk aversion. Even in a market as large and mature as the United States, crypto-focused businesses continue to encounter obstacles in maintaining basic financial infrastructure. The issue became especially acute after the collapse of crypto-friendly banks such as Silvergate, Signature, and Moonstone; institutions that once served as key bridges between fiat and digital assets. Their exit left a gap few traditional players have been willing to fill.

Why Tap Exists

The crypto industry has reached an inflection point. Regulatory frameworks like MiCA are providing clarity. Institutional adoption is accelerating. The technology is proven and tested. But the fundamental infrastructure gap remains: access to business banking that actually works for digital asset businesses.

This is precisely why we built Tap for Business.

We provide business accounts with dedicated EUR and GBP IBANs specifically designed for crypto companies and businesses that interact with digital assets. This isn't a side offering or an experiment, it's our core focus.

Our approach is straightforward

We built our infrastructure for this sector

Rather than retrofitting traditional banking systems to reluctantly accommodate crypto businesses, we designed our compliance, monitoring, and operational frameworks specifically for digital asset flows. This means we can properly assess and serve businesses that others automatically reject.

We price in the actual risk, not the sector

Blanket rejection policies exist because they're cheap and simple. We take a different approach: evaluating each business based on their actual controls, compliance posture, and operational reality. It costs more, but it's the only way to serve this market properly.

We're committed to sector normalization

Every time a legitimate crypto business is forced to operate without proper banking infrastructure, it reinforces outdated stigmas. By providing professional financial services to compliant businesses, we're helping demonstrate what should be obvious: crypto companies can and should be served by the financial system.

It isn't about taking on risks that others won't. It's about properly evaluating risks that others refuse to understand.

Moving Forward

The industry is maturing. Regulatory clarity is emerging. Institutional adoption is accelerating. But you can't put your business on hold while traditional banks slowly catch up to reality.

That's not sustainable in the long run.

As a firm, you shouldn't have to beg for a bank account. You shouldn't have to downplay your crypto operations just to access basic financial services. And you certainly shouldn't have to accept that systematic exclusion with little to no explanation other than “It’s just how things are."

The crypto sector is building the future of finance. Your banking partner should believe in that future too. If you're ready to work with financial infrastructure built for your business, not in spite of it, here we are.

Talk today with one of our experts to understand how we can help your business access the banking infrastructure you need.

NEWS AND UPDATES

LATEST ARTICLE

Om du är ny i kryptovärlden, eller bara nyfiken på stablecoins, så har du hittat rätt. Här går vi igenom allt du behöver veta om dessa digitala tillgångar. Vi kommer att förklara varför de är användbara på finansmarknaden och även titta närmare på några av de mest populära stablecoins som handlas idag.

Stablecoins är inte skapade för att ge avkastning, men de fungerar som ett effektivt skydd mot värdeförluster när marknaden vänder nedåt. Dessutom låter de användare dra nytta av kryptons fördelar som traditionella valutor inte kan erbjuda.

Även om man kan tro att regleringen för stablecoins skulle skilja sig från annan krypto, ligger de idag under samma paraply som övriga digitala tillgångar. Dock pågår diskussioner om att reglera stablecoin-emittenter mer specifikt.

Vad är stablecoins?

Stablecoins är en typ av kryptovaluta som är utformad för att hålla ett stabilt värde genom att knytas till en stabil tillgång, som till exempel en fiatvaluta eller råvara. Syftet är att erbjuda en stabilare marknad i en annars volatil bransch.

Stablecoins gör det möjligt för företag att använda krypto utan att utsätta sig för extrema prisrörelser eller risker kopplade till motparter. Även om de inte ger den avkastning som ofta förknippas med kryptomarknaden, erbjuder de en strategi för att skydda sig mot volatilitet.

I takt med att kryptomarknaden växer snabbt, har vi nu ett brett utbud av stablecoins med olika strukturer, ledarskap, rykten och användningsområden. Stablecoins delas huvudsakligen in i två kategorier: fiat-säkrade stablecoins och krypto-säkrade stablecoins, men det finns också algoritmiska stablecoins och råvarubackade stablecoins.

Fiat-säkrade stablecoins (fiatvalutor)

Fiat-säkrade stablecoins är knutna till statligt utgivna valutor, som den amerikanska dollarn. Dessa coins är backade i förhållandet 1:1, vilket innebär att emittenten håller motsvarande mängd fiatvaluta i ett säkert konto.

Exempel på stablecoins i denna kategori är Tether (USDT), Paxos Standard Token (PAX) och USD Coin (USDC). Alla är kopplade till den amerikanska dollarn och kräver att utgivaren håller motsvarande belopp i reserv.

Krypto-säkrade stablecoins (kryptovalutor)

En något ovanligare typ av stablecoins är de som är säkrade med andra kryptotillgångar. Här baseras värdet på den underliggande kryptovalutan, och projektet behöver inte en tredje part för att hålla reserver.

Ett bra exempel är DAI — en krypto-säkrad stablecoin som skapas när användare skickar ETH till ett Ethereum-baserat smart kontrakt.

Algoritmiska stablecoins (smart contracts)

Algoritmiska stablecoins är kopplade till andra digitala tillgångars värde via smarta kontrakt och samverkar med en annan kryptovaluta. Om priset går över den tänkta nivån, skapas nya coins för att sänka värdet. Om priset sjunker under peggingen, bränns coins för att höja värdet.

Att investera i algoritmiska stablecoins betraktas som högrisk, eftersom eventuella fel i algoritmen kan leda till dramatiska värdeförluster — något vi såg med Terra LUNA-kraschen 2022.

Råvarubackade stablecoins

Det finns även stablecoins som är backade av råvaror, som guld. Populära exempel här är Paxos Gold (PAXG) och Tether Gold (AUXt), vilka är kopplade till fysiskt guld som lagras i valv.

Vissa stablecoins, som kallas centralbankernas digitala valutor (CBDC), backas inte av någon specifik tillgång men är ändå kopplade till ett fiatvärde. Dessa ges ut av centralbanker som en digital version av deras nationella valuta.

Hur fungerar stablecoins?

Stablecoins är oftast byggda på blockkedjenätverk som möjliggör smidiga transaktioner. Det mest populära standardprotokollet för stablecoins är Ethereum's ERC-20.

Precis som andra kryptovalutor används stablecoins i peer-to-peer-transaktioner, men de nyttjar Ethereum-nätverket för att genomföra dessa och hålla nätverket säkert.

Emittenten av stablecoinen ansvarar för att hålla motsvarande belopp i fiat eller andra säkra tillgångar i reserv. I fallet med råvarubackade stablecoins lagras den underliggande tillgången fysiskt i valv.

Vad används stablecoins till?

Medan världen långsamt integrerar kryptovalutor i det traditionella finansiella systemet, erbjuder stablecoins ett enkelt sätt att bygga broar mellan dessa två världar.

Stablecoins ger användare fördelarna med digitala tillgångar utan den typiska volatiliteten och hjälper kryptoekosystemet att smidigt integreras i vardagen.

Vilka risker finns med stablecoins?

Trots deras namn bär stablecoins fortfarande vissa risker. Deras värde är beroende av den tillgång de är kopplade till, vilket betyder att de inte är helt immuna mot snabba prisrörelser.

Regleringsrisk är också en faktor, eftersom lagar och riktlinjer för stablecoins snabbt kan förändras. Dessutom är stablecoins utsatta för emittentrisk — deras stabilitet beror på trovärdigheten hos den organisation som backar dem.

Otillräckliga reserver eller bristande transparens kan leda till likviditetsproblem och skakiga marknader.

Vad är syftet med stablecoins?

Du kanske undrar varför man skulle vilja köpa en tillgång som inte förväntas ge avkastning. Svaret är att stablecoins spelar en viktig roll inom kryptomarknaden.

Skydd mot volatilitet

De fungerar som en säker hamn när marknaderna svänger kraftigt. Eftersom de är kopplade till en stabil tillgång kan du skydda dina medel under björnmarknader och enkelt flytta tillbaka dem när marknaden stabiliseras.

Prisstabilitet (likt fiatvalutor)

Stablecoins ger också stabilitet vid handel med kryptovalutor, vilket är särskilt värdefullt för företag som vill använda krypto för betalningar. Genom att använda en stabil valuta slipper de risken att ett köp för $2 plötsligt bara är värt $1.

Remitteringsmarknaden

Stablecoins används också flitigt för att snabbt och billigt skicka pengar över landsgränser — betydligt smidigare än traditionella banköverföringar.

Populära stablecoins på kryptomarknaden

Stablecoins har gått från att vara ifrågasatta till att idag finnas med bland de fem största kryptovalutorna sett till marknadsvärde.

Tether (USDT)

Tether är förmodligen den mest kända stablecoinen och hör till de fem största kryptovalutorna totalt. Trots viss kontrovers kring dess reserver är Tether ett självklart val för många företag och investerare.

Ursprungligen lanserades Tether 2014 under namnet Realcoin och byggdes som ett lager ovanpå Bitcoin-nätverket. Idag används ERC-20-standarden och stöds även på Ethereum, EOS, Tron, Algorand och OMG.

Dai (DAI)

DAI började som Single-Collateral DAI (SAI), baserat på en enda kryptotillgång. 2019 lanserades Multi-Collateral DAI, som är soft-peggad till den amerikanska dollarn och baserad på flera kryptotillgångar via Ethereum smarta kontrakt.

DAI hanteras av Maker Protocol och MakerDAO, och användare kan även tjäna ränta genom att hålla DAI-tokens.

USD Coin (USDC)

USDC är en annan populär fiat-backad stablecoin, med ett något mindre kontroversiellt rykte. Bakom står Centre Consortium, som håller $1 i reserv för varje USDC som ges ut.

Målet är att skapa ett ekosystem där USDC accepteras av så många plånböcker, börser och tjänster som möjligt.

Utforska stablecoin-världen i appen

Stablecoins är kända för sin förmåga att hålla värdet stabilt och erbjuda ett skydd mot prisrörelser på marknaden.

Oavsett om du vill bygga en portfölj med fiat- eller krypto-säkrade stablecoins, eller hålla dig till traditionella kryptovalutor, så erbjuder Tap-appen en smidig och säker plattform för att hantera dina tillgångar.

Med Tap-appen får du tillgång till både börshandel och en unik plånbok där du kan förvara både krypto och fiat. Dessutom kan du använda ett förbetalt kryptokort för att betala var som helst i världen — med ett enkelt knapptryck.

We are delighted to announce the listing and support of Enjin (ENJ) on Tap!

ENJ is now available for trading on the Tap mobile app. You can now Buy, Sell, Trade or hold ENJ for any of the other asset supported on the platform without any pair boundaries. Tap is pair agnostic, meaning you can trade any asset for any other asset without having to worries if a "trading pair" is available.

We believe supporting ENJ will provide value to our users. We are looking forward to continue supporting new crypto projects with the aim of providing access to financial power and freedom for all.

Playing an important role in the adoption of Web3, Enjin provides a platform of software products designed to allow anyone to harness the power of NFTs (non-fungible tokens) through the development, trade, monetization, and marketing of blockchain assets.

Powering the ecosystem is the Enjin Coin (ENJ), a token used to back the value of NFTs and other assets minted on the platform. When an asset is minted it locks ENJ tokens into a smart contract and effectively removes the tokens from circulation.

Enjin Coin (ENJ) is the native token of the Enjin ecosystem. Built on the Ethereum blockchain and compatible with multiple gaming platforms, the Enjin Coin is an ERC-20 token that allows the in-game items created on the platform to be traded with real-world value. The ENJ token has a maximum supply of 1 billion coins.

Get to know more about Enjin (ENJ) in our dedicated article here.

We are delighted to announce the listing and support of Chiliz (CHZ) on Tap!

CHZ is now available for trading on the Tap mobile app. You can now Buy, Sell, Trade or hold CHZ for any of the other asset supported on the platform without any pair boundaries. Tap is pair agnostic, meaning you can trade any asset for any other asset without having to worries if a "trading pair" is available.

We believe supporting CHZ will provide value to our users. We are looking forward to continue supporting new crypto projects with the aim of providing access to financial power and freedom for all.

Chiliz is a fintech company that uses blockchain technology to create new ways for fans to support and engage directly with their favorite sports teams. The company's goal is to be the leading provider of fintech solutions for sports and entertainment businesses around the world. Chiliz enables its users to trade tokens to show their support for professional sports teams.

Chiliz fans can buy their favorite team's Fan Tokens using the native Chiliz token " CHZ " on socios.com, the crowd management platform that Chiliz uses. Sports fans staking $CHZ on Socios.com also have opportunity to receive new Fan tokens as well as a up to 10% $CHZ bonus yield.

Despite radically reshaping the world’s financial landscape, the first ever cryptocurrency has limitations when interacting with newer blockchains. For example, Ethereum. Wrapped Bitcoin (WBTC) solves this limitation by allowing Bitcoin to function on the Ethereum network, enabling access to decentralized finance (DeFi) services.

WBTC is an ERC-20 token that represents Bitcoin 1:1 on the Ethereum blockchain, combining Bitcoin’s value with Ethereum’s smart contract power, and opening new opportunities for BTC holders in decentralized finance (DeFi). Unlike Bitcoin variants aiming to improve its technology, WBTC extends Bitcoin's utility without replacing it.

Join us in this deep dive on how WBTC works, its benefits, risks, and how it connects Bitcoin to the broader DeFi ecosystem.

Unlocking Bitcoin’s Power on Ethereum

Launched in January 2019, approximately 10 years after Bitcoin's initial release, WBTC was created as a collaborative effort between BitGo, Kyber Network, and Ren (formerly Republic Protocol), along with other major players in the DeFi space including MakerDAO, Dharma, and Set Protocol.

As an ERC-20 token, WBTC adheres to Ethereum's token standard, making it compatible with the entire Ethereum ecosystem, including its smart contracts, decentralized applications, and wallets.

In structure, WBTC bears similarities to stablecoins like USDC or USDT, which are backed by reserve assets. However, while stablecoins aim to maintain a stable value (usually pegged to a fiat currency like the US dollar), WBTC's value fluctuates with Bitcoin's market price.

Each WBTC token is backed by an equivalent amount of Bitcoin (BTC) held in reserve by a custodian, maintaining a strict 1:1 ratio, meaning 1 WBTC is always equivalent to 1 BTC in value.

Wrapped Bitcoin is now under the control of a Decentralized Autonomous Organization (DAO) called the WBTC DAO. This organization oversees the protocol, ensuring the integrity of the wrapping process and maintaining transparency in the system. Unlike Bitcoin's fully decentralized nature, WBTC relies on certain trusted entities to maintain the backing of the tokens, which creates an interesting balance between utility and trustworthiness.

WBTC belongs to a broader category of financial instruments known as "wrapped tokens." These are cryptocurrencies that are enclosed or "wrapped" in a digital vault and represented as another token on a different blockchain. While WBTC represents Bitcoin on Ethereum, there are other wrapped tokens in the cryptocurrency space, including Wrapped Ether (WETH) which, somewhat paradoxically, is a wrapped version of Ethereum's native token on its own blockchain that conforms more strictly to the ERC-20 standard.

Why Does Wrapped Bitcoin Exist?

Wrapped Bitcoin (WBTC) was created to bridge the gap between Bitcoin and newer blockchain platforms like Ethereum.

1. Bitcoin's limited smart contract functionality

Bitcoin prioritizes security over programmability, making it unsuitable for complex decentralized apps. In contrast, Ethereum supports smart contracts that power a wide range of automated financial services.

2. Access to DeFi for Bitcoin holders

Ethereum's DeFi ecosystem offers lending, trading, and yield farming, but Bitcoin holders couldn't participate without converting their BTC. WBTC solves this, letting them use Bitcoin's value within Ethereum-based applications.

3. Unlocking Bitcoin's liquidity

Bitcoin's vast market capitalization holds significant untapped liquidity. WBTC brings this capital into Ethereum's DeFi network, benefiting both Bitcoin holders and the broader ecosystem.

4. Faster, more flexible Bitcoin transactions

While Bitcoin transactions can be slow and costly, WBTC uses Ethereum's network for quicker, cheaper trades-ideal for active traders and DeFi users.

In short, WBTC enhances Bitcoin's utility without altering its core protocol, connecting it to the evolving world of decentralized finance.

How Does Wrapped Bitcoin Work? The Nuts and Bolts

Wrapped Bitcoin (WBTC) bridges Bitcoin and Ethereum through a secure, transparent process involving key participants and smart contracts.

1. Wrapping and unwrapping process:

Wrapping (BTC → WBTC): Users send Bitcoin to a custodian, who secures it and mints an equivalent amount of WBTC on Ethereum, sending it to the user's Ethereum wallet.

Unwrapping (WBTC → BTC): Users burn WBTC, prompting the custodian to release the equivalent Bitcoin back to their Bitcoin wallet.

This 1:1 pegging ensures WBTC is fully backed by Bitcoin reserves.

2. Key participants:

Custodians (e.g., BitGo): Hold and safeguard the Bitcoin backing WBTC.

Merchants: Authorized to request minting or burning of WBTC.

Users: Individuals or entities using WBTC in Ethereum's DeFi ecosystem.

WBTC DAO Members: Stakeholders who govern protocol decisions.

3. Transparency and verification:

Proof of reserves: Publicly verifiable Bitcoin addresses back every WBTC in circulation.

On-chain verification: Minting and burning are recorded on both blockchains.

Regular attestations: Independent checks confirm reserve accuracy.

4. Technical implementation:

WBTC is built as an ERC-20 token, Ethereum’s standard for fungible tokens. All ERC-20 tokens follow the same set of rules, which makes them interchangeable, easy to trade, and instantly compatible with most Ethereum wallets and DeFi apps.

This makes WBTC easily transferable, compatible with wallets, and usable in DeFi apps like lending platforms, decentralized exchanges, and yield farming protocols. It gives Bitcoin the same programmability and utility as Ethereum-native assets.

Showdown: Wrapped Bitcoin (WBTC) vs. Bitcoin (BTC)

Although WBTC and BTC share the same value, their use cases differ. Bitcoin is designed for security, immutability, and censorship resistance. WBTC, on the other hand, thrives in Ethereum’s ecosystem where smart contracts enable lending, borrowing, and trading.

For storing wealth long-term, Bitcoin remains the go-to. For generating yield or accessing DeFi, WBTC is the practical choice. Different uses for different needs.

How Wrapped Bitcoin Boosts Your Crypto

1. DeFi accessibility:

WBTC lets users leverage Bitcoin in DeFi platforms for:

Lending & borrowing: Use WBTC as collateral on platforms like Aave or Compound to earn interest or borrow assets.

Yield farming: Provide WBTC liquidity for rewards, often surpassing Bitcoin's passive holding returns.

Liquidity provision: Earn trading fees by adding WBTC to pools on exchanges like Uniswap.

Synthetic assets: Mint assets pegged to traditional markets using WBTC as collateral.

2. Enhanced liquidity:

WBTC boosts capital efficiency across Ethereum by:

Expanding DeFi liquidity: Unlocking Bitcoin's market value to strengthen liquidity pools.

Reducing slippage: Deeper markets enable smoother trades.

Providing stable collateral: Bitcoin-backed assets offer trusted options for DeFi protocols.

3. Transaction advantages:

Compared to Bitcoin, WBTC transactions on Ethereum benefit from:

Faster confirmations: Ethereum's ~12-second block times outpace Bitcoin's 10-minute average.

Predictable fees: Ethereum's fee structure can be more cost-effective in certain conditions.

Smart contract integration: WBTC supports complex transactions Bitcoin's network can't handle.

4. Broader utility:

Beyond DeFi, WBTC enhances user options by:

Accessing smart contracts: Participate in advanced applications without selling Bitcoin.

Composability: Use WBTC across multiple protocols simultaneously.

Simplified management: Store WBTC alongside other Ethereum assets in common wallets.

Gaming & NFTs: Spend WBTC in blockchain games or NFT marketplaces.

While WBTC offers significant opportunities, it comes with trade-offs regarding decentralization and security, as covered in the next section.

Navigating Wrapped Bitcoin: Risks and Challenges

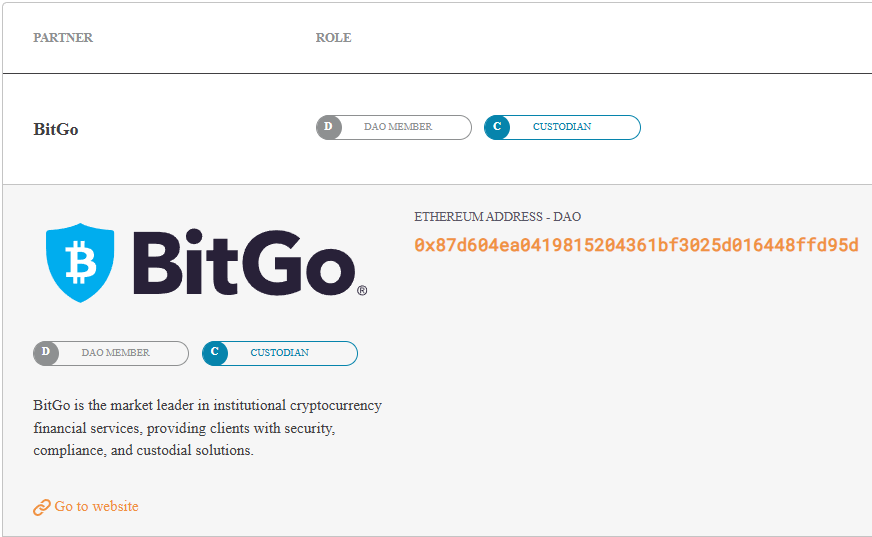

Custodial risks

While WBTC brings Bitcoin into DeFi, it introduces centralization as well. WBTC depends on BitGo as the sole custodian to hold the backing Bitcoin, creating a central point of failure. Users must trust these custodians to safeguard funds, process redemptions, and comply with regulations that could freeze assets or restrict conversions.

BitGo, DAO member and sole custodian. Source.

Smart contract risks

WBTC relies on Ethereum smart contracts, which, despite audits, can still have vulnerabilities or coding flaws. It's also affected by Ethereum network issues like congestion, high gas fees, and risks from interacting with DeFi platforms.

Price and market risks

WBTC tracks Bitcoin's price and shares its volatility. In turbulent markets, it may trade slightly above or below Bitcoin's value. Large conversions can strain liquidity, making big trades harder without impacting price.

Operational challenges

Managing WBTC involves both Bitcoin and Ethereum blockchains, which can be complex for newcomers. High Ethereum gas fees and slow WBTC-to-Bitcoin conversions (especially for large transactions) are additional hurdles.

Alternatives with less trust required

Some users prefer fully decentralized options like native Bitcoin, though it lacks smart contract functionality. Other wrapped Bitcoin solutions use different technologies to reduce reliance on custodians.

Wrapping Up WBTC

WBTC represents a shift in the cryptocurrency space, bridging the gap between Bitcoin's unparalleled network security and store-of-value properties with Ethereum's programmability and vibrant DeFi landscape. Since its launch in 2019, WBTC has grown from a novel concept to a cornerstone of cross-chain interoperability, enabling countless new use cases for Bitcoin holders.

For users, WBTC allows exposure to Bitcoin while engaging with decentralized finance (DeFi) on Ethereum and other platforms, enabling participation in both without choosing between them. While for DeFi, Bitcoin's liquidity has fostered growth, stability and asset diversity. WBTC has also paved the way for other wrapped assets, making the crypto ecosystem more interconnected and efficient.

As blockchain technology evolves, solutions like WBTC will address limitations while retaining core utility. Its success shows how cryptocurrency innovation can build upon existing strengths without replacing them.

Other Wrapped Bitcoin alternatives

While WBTC is the most widely used Bitcoin representation on Ethereum, several alternatives have emerged, each with different approaches to the bridge between Bitcoin and other blockchains:

- renBTC

- tBTC

- sBTC (Synthetic BTC)

- HBTC

- pBTC

How Can I Buy Wrapped Bitcoin (WBTC)?

If you’re looking to bring Bitcoin into the world of Ethereum, Wrapped Bitcoin (WBTC) is the gateway you might be looking for. Through the Tap app, users can easily add WBTC to their portfolios, opening up access to Ethereum’s thriving DeFi ecosystem. Getting started is simple: just download the app, create an account, and start trading WBTC in minutes.

As we move into a more digital world with enhanced security systems, so too are hackers and fraudsters. With millions of dollars lost each year at the hands of these ill actors, in this article we take a look at the 5 most common crypto scams and how to spot them. The financial world need not be a scary place, with a few precautions in place you can bank on being able to avoid them.

What is a crypto scam?

A crypto scam is a type of investment fraud revolving around cryptocurrencies. According to a report by Chainalysis, a record-breaking $14 billion of crypto was stolen last year through crypto scams. While there are many different types of crypto scams, of which we'll explore 5 below, the common thread is that crypto is wrongfully taken from a user through fraudulent activities.

The biggest crypto scam of recent times was in late 2020 when people hacked into the Twitter accounts of high profile individuals and claimed that should someone send Bitcoin or Ethereum to an address they will receive twice the value back. These accounts included the likes of Barack Obama, Elon Musk and Joe Biden.

The top 5 most common crypto scams

While there are an infinite amount of crypto scams out there, below we are highlighting the 5 most common ones.

Fake crypto exchanges

These types of exchanges provide a buy/sell platform on which users can trade cryptocurrency, however, once they have deposited the funds they cannot withdraw any money. These funds might still appear on the platform although the money is long gone.

Always read the reviews of a platform, and do your own research before depositing money anywhere.

Ponzi schemes

Ponzi schemes might have started in the late 1800s but they're still here. The scheme works in such a way that each member earns rewards by recruiting new members, whose money is then used to pay off older members. This eventually reaches a saturation point after which it collapses.

Always do your due diligence and ensure that the scheme you're investing in is solid. If it sounds too good to be true, it probably is.

Fake investment schemes

Be wary of an investment opportunity promising to deliver unbelievable gains. This might be in the form of depositing funds on a platform only to lose the money or struggle to withdraw it at a later stage. These are often circulated through well-known publications or on social media with celebrities "endorsing" the products.

Pump and dumps also fall into this category. These schemes are created when a large group of people decide to invest in a coin, only to drive up the prices and cash out at the top. Many people are then left with a worthless coin at the end, having lost their investment.

Imitating a crypto exchange

Similar to the concept of phishing, someone might create a social media account of a big exchange and contact the user "on behalf of the company". This is intended to gain your trust and is either done in an attempt to gain your passwords, or with a message that you owe large amounts in tax which needs to be paid in Bitcoin immediately to avoid imprisonment.

Never follow links in an email, rather access the site from your own browser directly and be sure to check the URL. Successful scams of this nature often have a small typo in the URL which goes unnoticed.

Malware & ransomware

The malware allows scammers to gain access to your computer, either locking you out of files or stealing credit card or crypto address details. With this information, they can drain your accounts in minutes.

Ransomware works slightly differently in that the scammers lock the entire computer and demand a ransom to gain access again. This is often paired with blackmail where the victim, and in some cases organizations, are threatened that if they don't pay sensitive information will be released. A lot of victims in this situation manage to get out of it unharmed.

These might sound very scary, but should you maintain safe online protocols and check URLs before entering your details, they should be entirely avoided.

5 tips on how to avoid crypto scams

These might sound obvious but it never hurts to read them again. Below are 5 tips on how to stay vigilant and avoid crypto scams entirely.

- Be wary of phone calls and emails claiming to be from exchanges and never click the links from them.

- Never give your password, private key or security codes to anyone.

- Never give someone remote access to your device.

- Look out for social media accounts imitating legal firms or exchanges or a prominent person in the industry. Support will never contact you from a social media account.

- And lastly, if it sounds too good to be true - it probably is.

Easily avoided, comfortably secure

We hope this information assists you in keeping your data and money secure online, proper security is always imperative when using payment methods or services on the internet. As technology evolves, so too must our security systems and vigilance. With these tips above you should be well on your way to spotting something that doesn't quite look right, and avoiding crypto scam.

There's a time-old debate over whether hodling or trading leads to better profits when it comes to buying into the cryptocurrency market. While both are great options, in the article below we look at the pros and cons of each option and weigh them up.

What is trading?

Trading refers to the buying and selling of financial instruments, assets, or commodities in financial markets with the aim of making a profit. Trading requires continuous monitoring of the charts and frequent study, whether in the crypto or stock market. Crypto trading involves buying and selling crypto at various intervals, whether minutes, hours, days, weeks, months, and years. Despite the greater risks involved, the potential for big percentage returns attracts individuals to trading.

If you want to trade crypto assets, it's essential to have a basic knowledge of the industry and how events in the news may influence Bitcoin's price. Remember to set stop losses and take profits so that you can protect your trade.

The pros of trading

- Potentially sizable profits

Crypto is known to be a volatile market and it's not uncommon to see price movements of 30% or above when crypto trading. With some strong analytical skills, one can observe, analyze and trade these waves and yield sizable profits.

- You're in control

Some people make a living trading part-time or full-time, particularly day trading. Day trading is where you enter and exit positions typically within a 24-hour period. Either way, you are in control of your own hours and workload, allowing you to take a break after you've met or exceeded your daily or weekly earnings targets.

The cons of trading

- Need to know trading fundamentals and technical analysis

Before you begin trading, you need to learn how to do fundamental and technical analysis of charts. This process requires dedicated effort and time investment.

- Need to be able to manage emotions

The prices of cryptocurrencies can change rapidly, making this a more risky proposition than long-term holding. You must be prepared to sell a losing cryptocurrency when it's plunging or decide to hodl for it to recover. Anything might happen in this fast-paced market, so you must make wise decisions without getting emotional.

What is hodling?

The term first came about in 2013 from a misspelled work in a BitcoinTalk Forum. The inebriated trader made the now infamous typo, and the word stuck. Almost a decade later, the term "hodl" remains a permanent fixture in the crypto ecosystem. Some have since branded it as "Hold On for Dear Life".

The term refers to holding a particular cryptocurrency for long periods of time, ignoring market volatility and knuckling through a bear market. As a passive strategy designed for long-term time frames, hodling requires a trader to simply buy a cryptocurrency and hold it in a secure place for months or even years until it reaches your price target.

You can buy Bitcoin or your favorite cryptocurrency at regular intervals if you're planning to HODL. This term is associated with buying a small amount of Bitcoins weekly or monthly. For example, let's say you have $1,000 to buy over time.

In this case, you might purchase $30 in Bitcoin each week or $50 worth every month. By staggering your buys like this rather than putting it all at once, you minimize the likelihood of price fluctuations having as much impact on the price per coin. This strategy prefers to buy Bitcoin over trade Bitcoin.

The upside to hodling

- Minimal effort

Hodling requires initial research into the cryptocurrency you wish to buy in (very important ans crucial to do your own research). From there establish your budget and strategy.

- Minimal stress

The crypto market is known for its significant swings in value. Thankfully with hodling there is no need to time the market for entry and exit positions or watch the chart all of the time.

- Minimal trading fees

Save money on trading fees by conducting on a few transactions, versus the many you will need to do when day trading. Some countries won't even charge tax on your crypto gains after a certain period of time (but be sure to check this in your area).

The downside of hodling

- Need patience

As hodling is a long-term strategy approach it requires patience and mental endurance. If you decide to use the Hodling strategy you'll need to manage emotions during tough market fluctuations and might need to wait years before being able to cash in on any ROI (return on investment).

- Funds are locked in

Because this is a long-term strategy, your funds would be inaccessible for an extended period of time. This might result in foregone opportunities to invest elsewhere in the crypto space or any other market.

However, this can be avoided by leaving your funds in a crypto interest account. Tap provides users access to yield-generating wallets that allow you to enjoy both the long-term price gains as well as the returns.

In Conclusion: hodling vs trading

If you're a novice cryptocurrency investor, proceed with caution. There is no right or wrong answer to which of these strategies is "superior" and you could always combine both methods to match your portfolio depending of your risk appetite. Always keep in mind that before making any decisions, always do your homework, research about the asset you wish to purchase and about diversifying your portfolio to reduce risk regardless of the strategy you pick.