An in-depth look at XRP’s 2025 momentum, as legal clarity, technical strength, and growing institutional interest converge for the first time since 2017.

Keep reading

This week, XRP has been building pressure at $3.30, with three powerful catalysts aligning for the first time since 2017 - setting up what could be the token's most explosive run yet.

TLDR:

- XRP price surged 21% after the SEC Ripple Labs case was officially dismissed

- Technical indicators show buy-side momentum peaking, with Aroon Up hitting 100%

- Nine major asset managers now have pending XRP ETF applications, with 88% market odds for 2025 approval

- CME's XRP futures launched in May have already generated over $1.6 billion in trading volume

Three big forces are hitting XRP at once: legal clarity, strong technical momentum, and rising institutional demand. In the past, this mix has sent prices soaring.

The legal victory that changes everything

The SEC's formal dismissal of its case against Ripple Labs isn't just another regulatory win - it's the removal of XRP's biggest institutional adoption barrier. After nearly five years of uncertainty, corporate treasuries and institutional investors finally have the green light they've been waiting for.

And the timing couldn't be better. Just as regulatory clouds clear, analysts are agreeing that XRP's technical setup is screaming bullish signals that haven't been seen since the 2017 run-up.

Technical momentum reaches peak levels

XRP's chart tells a compelling story of institutional accumulation disguised as consolidation:

→ For starters, the token has climbed 21% over the past seven days, hitting a recent high of $3.36 (just 8% below its ATH). Momentum indicators suggest this is just the beginning.

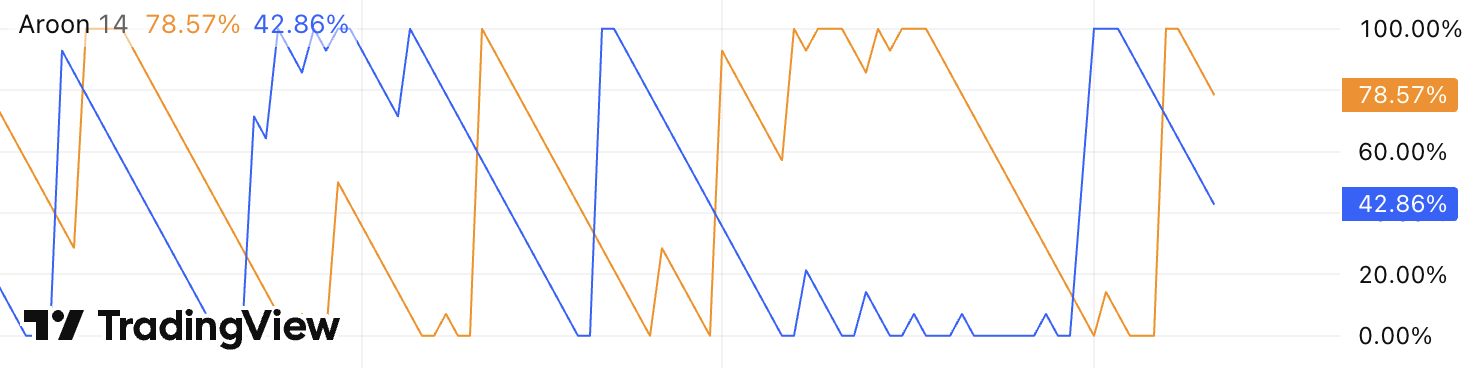

→ The Aroon Up line is holding at 100%, showing that buyers are consistently driving XRP to fresh highs. This sustained strength often comes before major moves - especially with the price holding above the key $3.15–$3.16 support area. *To view the current Aroon line, log into Trading View and add the indicator.

→ Market sentiment has shifted decisively bullish, with XRP's weighted sentiment score hitting a two-week high of 1.17. More telling is the token's social dominance, which has climbed to a recent high of 7.95%, meaning XRP is dominating an increasingly larger share of crypto conversations as retail interest reignites.

The institutional infrastructure is already built

While crypto X debates ETF timelines, institutional players have quietly constructed the infrastructure needed for serious XRP adoption. CME Group launched regulated XRP futures in May, providing the hedging tools institutions will need before taking major positions.

The results speak volumes: CME's XRP futures have already surpassed $1.6 billion in trading volume, signalling genuine institutional demand beyond retail speculation. These aren't just paper trades; they represent real institutional capital positioning for XRP's next move.

Nine major asset managers now have pending XRP ETF applications, including heavyweights like Grayscale, ProShares, and 21Shares. Polymarket traders are pricing in 88% odds for SEC approval by year-end, creating a feedback loop where institutional preparation drives retail anticipation.

Why this time is different

Previous XRP rallies were driven primarily by retail speculation and partnership announcements. But today's setup combines retail enthusiasm with genuine institutional infrastructure and regulatory clarity: a trifecta that hasn't existed since XRP's 2017-2018 surge.

The numbers back this up. Institutional trading volumes have spiked 208% to $12.40 billion following the SEC dismissal, while derivatives open interest climbed 15% to $5.90 billion.

Large-order flows are consistently defending the $3.15 support level, suggesting institutional accumulation even during short-term volatility.

What traders are watching

Analysts are saying that technical analysis points to immediate resistance at $3.39-$3.40, with sustained bullish momentum (bolstered by institutional flows and ETF positioning) raising the odds of a breakout, particularly if the Aroon Up indicator remains high.

According to market insiders, a successful move higher could fuel a run toward the $3.50-$3.75 range, with a longer-term target of $3.66+ for a cycle high retest.

Key levels to monitor:

- Support: $3.15-$3.16 (proven institutional buying zone)

- Resistance: $3.39-$3.40 (breakout confirmation level)

- Bull target: $3.66+ (cycle high retest)

Legal clarity, a technical breakout, and rising institutional demand are all hitting XRP at once - a rare mix of fundamentals and market momentum. For holders who’ve endured years of regulatory uncertainty, some are interpreting this as a potential breakout scenario.

NEWS AND UPDATES

LATEST ARTICLE

For millennia, humans have defined value through the tangible: gold you could hold, land you could stand on, and later, paper notes backed by government promises. But in just over a decade, cryptocurrency has fundamentally challenged these ancient conventions, introducing a radical new proposition: what if value could exist purely as information, secured not by central authorities but by mathematics and collective consensus?

Consider this: cryptocurrency isn't merely a financial innovation; it represents a philosophical, cultural, and psychological revolution in how we conceptualise value itself. While traditional economists and crypto bros might view crypto assets as speculative instruments, they miss the broader transformation occurring beneath the price charts - a complete reconstruction of our relationship with money, trust, and economic participation.

As we'll explore, this shift extends far beyond trading and investing. It's reshaping how entire generations think about wealth preservation, questioning long-held assumptions about institutional authority, and expanding financial access to previously excluded populations. From Bitcoin's deflationary model to the complex ecosystems of decentralised finance, crypto is rewriting the very language of value in the digital age. Let’s explore it.

From tangible to digital: the evolution of wealth perception

"Where exactly is your Bitcoin?" This seemingly simple question reveals the profound shift occurring in our collective understanding of wealth. For centuries, value storage meant physical possession (again, gold bars in vaults, cash in wallets, or property deeds in filing cabinets). The materiality of these assets provided psychological comfort; you could literally touch your wealth.

Cryptocurrency challenges this fundamental association between physicality and value. When someone owns Bitcoin, they don't possess a digital coin in the conventional sense. Instead, they control access to a position on an immutable ledger - a concept so abstract that it requires significant cognitive adjustment for many traditional investors.

From a behavioural aspect, the difficulty many people have with accepting cryptocurrency stems from our evolutionary programming: our brains developed to value tangible resources (food, shelter, tools). Abstract representations of value require more cognitive processing, which is why many people struggle with the concept of crypto despite understanding it intellectually.

This transition mirrors other historical shifts in value perception. When paper money first replaced gold coins, many resisted the change, insisting that value couldn't exist in mere paper promises. Today's movement from government-issued currency to algorithmic scarcity follows a similar pattern of initial resistance followed by gradual normalisation.

What makes the current transition unique is its complete divorce from the physical realm. Bitcoin, Ethereum, and thousands of other digital assets exist exclusively as information, secured through cryptography, distributed across thousands of computers worldwide, and accessible only through digital keys. This represents not an incremental change but a quantum leap in how we conceptualise ownership and store value.

Decentralisation: redefining trust and authority

Perhaps crypto's most revolutionary aspect isn't its digital nature but its decentralised structure. For centuries, we've outsourced trust to centralised institutions, for example, banks to protect our deposits, governments to manage currency supplies, and credit agencies to verify our financial identities.

Cryptocurrency proposes an alternative: what if trust could be encoded into protocol rules, distributed across networks, and verified by mathematics rather than human authorities?

When Satoshi Nakamoto created Bitcoin, it wasn't just a new asset class - it was a fundamental challenge to the monopoly on money creation. By solving the double-spend problem without requiring a central authority, blockchain technology essentially digitised trust itself.

This decentralisation has profound implications across the financial landscape:

- Banking without banks: Cryptocurrency enables people to become their own financial institutions: storing, transferring, and managing wealth without intermediaries who charge fees and impose conditions.

- Censorship resistance: When value exists on distributed networks, it becomes extraordinarily difficult for any single entity to freeze assets or block transactions, creating new forms of financial freedom.

- Global accessibility: Traditional financial systems reflect geographic and political boundaries. Decentralised networks operate independently of these constraints, allowing anyone with internet access to participate in the global economy.

In emerging markets particularly, this shift from institutional to algorithmic trust has accelerated rapidly. When Venezuela experienced hyperinflation exceeding 1,000,000% in 2018, many citizens turned to Bitcoin not as a speculative investment but as a practical necessity, literally a more stable store of value than their national currency. Similar adoption patterns have emerged across countries with unstable monetary policies or restrictive capital controls.

Some may view decentralisation as more than just a technological preference and more of a direct response to institutional failure. For example, when central banks and governments repeatedly mismanage monetary policy, people naturally tend to seek alternatives that can't be arbitrarily inflated or confiscated.

Scarcity, security & the psychology of hodling

Unlike fiat currencies that can be created indefinitely by central banks, Bitcoin introduced the concept of absolute digital scarcity: only 21 million will ever exist. Again, this fixed supply fundamentally changed how people think about money's relationship to inflation and time.

The term "HODL" (originally a typo for "hold") has evolved from crypto-community slang into a philosophy reflecting a significant psychological shift. Hodlers view cryptocurrency not as a short-term trading vehicle but as a long-term store of value, for some: digital assets worth preserving across generations.

Economist Saifedean Ammous, author of The Bitcoin Standard, argues that Bitcoin marks a return to "hard money" principles. He suggests that for most of human history, money was tied to inherently scarce resources like gold, which couldn't be artificially increased. In contrast, the widespread use of elastic fiat currencies in the 20th century is, in his view, a historical outlier. Bitcoin, with its fixed supply, reintroduces the idea of money that resists debasement.

This scarcity-based mindset has also impacted saving behaviours, particularly among younger generations. While traditional financial advisors typically recommend diversified portfolios with 3-6 months of emergency savings, many crypto adopters maintain much larger reserves, viewing fiat currency as an inherently depreciating asset and cryptocurrency as a hedge against monetary expansion.

The psychological security derived from mathematically guaranteed scarcity creates powerful emotional attachments. For many hodlers, their relationship with cryptocurrency transcends normal investment dynamics - it becomes a vote of confidence in a different economic model. This faith often persists through extreme market volatility, confounding traditional economic rationality models.

From a psychological perspective, consider this: the willingness to endure 70-80% drawdowns without selling suggests something deeper than profit motivation. For committed crypto holders, their assets represent not just potential financial gain but ideological alignment and identity. They're invested emotionally as well as financially.

Financial sovereignty and the global unbanked

For approximately 1.7 billion adults worldwide without access to banking services, cryptocurrency offers something revolutionary: financial inclusion without institutional permission. This aspect of the crypto revolution rarely makes headlines but represents one of its most profound impacts.

In regions where banking infrastructure is limited, cryptocurrency enables financial activities previously impossible:

- Cross-border remittances: Migrant workers can send money home without exorbitant fees or lengthy delays

- Savings protection: Citisens in economically unstable regions can store value beyond the reach of local currency depreciation

- Microfinance access: Blockchain-based lending platforms enable credit access without traditional banking relationships

The concept of "being your own bank" carries different significance for someone in rural Kenya than for someone in Manhattan. For the latter, it might represent philosophical alignment; for the former, it could mean the first real opportunity to participate in the global financial system.

Even in developed economies, cryptocurrency offers financial sovereignty to those facing exclusion. Sex workers, political dissidents, and others vulnerable to financial censorship have found in crypto a way to operate beyond institutional control, though, of course, this same quality raises legitimate concerns about illicit usage.

Risk, reward, and a new investment ethos

Cryptocurrency has also introduced an entirely different relationship with financial risk. Traditional investment wisdom emphasises diversification, steady appreciation, and risk mitigation. The crypto ecosystem, by contrast, has “normalised” extreme volatility, concentrated positions, and experimental financial protocols.

DeFi (decentralised finance) platforms exemplify this new investment psychology. These permissionless protocols enable users to lend, borrow, and trade directly through smart contracts, often offering yields far exceeding traditional finance but with correspondingly higher risks. The willingness to lock millions of dollars, or just hundreds, into experimental code represents a profound shift in risk tolerance.

What traditional investors might see as reckless, many crypto participants view as rational, given their time horizon and beliefs about technological adoption. If someone genuinely believes blockchain technology will transform finance, accepting short-term volatility for potential long-term exponential growth aligns with that conviction.

The future of value: identity, data, and the Metaverse

As crypto continues evolving, its impact on value perception extends into emerging domains like digital identity, data ownership, and virtual economies. Blockchain technology enables new forms of value representation far beyond simple currency.

The next frontier isn't just about money - it's about tokenising aspects of human activity that were previously outside economic systems. From attention to data to reputation, blockchain enables us to capture, measure, and exchange forms of value that were previously intangible. Enter Web3.

Several emerging trends suggest how our concept of value might further evolve:

- Digital identity as asset: Self-sovereign identity systems enable individuals to control and potentially monetise their verified credentials and reputation

- Data ownership: Blockchain-based systems allow users to control, track, and be compensated for their data rather than surrendering it to platforms

- Virtual property: As metaverse platforms develop, ownership of digital land, items, and experiences increasingly resembles traditional property rights

The integration of AI with blockchain technology particularly suggests radical possibilities. Autonomous economic agents (software that can hold assets, make transactions, and provide services) may create entirely new economic relationships not predicated on human participation at all.

Looking toward 2035-2045, we might see value systems where:

- Human attention becomes explicitly priced and compensated through micropayment systems

- Algorithmic reputation scores function as forms of capital across platforms

- Digital and physical assets become increasingly interchangeable through tokenisation

The distinction between 'real' and 'virtual' value is already dissolving. For digital natives, ownership of a rare game item or social token can feel as significant as physical possessions. As virtual experiences consume more of our time and attention, this trend will likely only accelerate.

Conclusion: the value revolution has already begun

Cryptocurrency's true revolution isn't financial - it's conceptual, transforming how we understand value itself. Beyond creating wealth or challenging institutions, crypto expands money's definition through mathematical scarcity, programmable assets, and community governance.

This philosophical shift fundamentally redefines our relationship with ownership, trust, and economic participation.

As digital and physical value boundaries blur, both opportunities and challenges emerge. Whether you participate or not, understanding these paradigm shifts will be crucial for navigating our economic future where value is increasingly defined by consensus rather than decree.

Du har hört historierna.

Någon köpte Bitcoin för några dollar och är nu ekonomiskt oberoende. Kanske var det en vän, ett nyhetsinslag eller den där personen som aldrig slutar prata om krypto. Och nu undrar du: Är det för sent att köpa Bitcoin?

Du är långt ifrån ensam. Folk har ställt exakt samma fråga vid varje ny prisnivå – när Bitcoin kostade 100 dollar, 1 000, 10 000 och till och med 100 000. Vissa hoppade på tåget, andra väntade och trodde att chansen redan hade gått dem förbi.

Men sanningen är: det är svårt att tajma marknaden. Det som känns "för sent" idag kan visa sig vara helt rätt om några år. Eller så är det verkligen för sent. Ingen vet säkert.

Den här guiden går igenom det du behöver känna till. Vi tittar på Bitcoins prisresa, nuläget och argumenten från båda sidor. Målet? Att ge dig en grund att fatta ett eget, informerat beslut.

En titt på Bitcoins prishistoria och marknadscykler

Att förstå var Bitcoin har varit hjälper till att sätta dagens pris i perspektiv. Så, häng med på en tillbakablick.

De tidiga åren (2009–2013)

Bitcoin började som ett experiment. År 2009 hade det inget egentligt pris – folk testade bara en ny digital valuta. Den första dokumenterade transaktionen? Någon köpte två pizzor för 10 000 BTC. Idag skulle de pizzorna vara värda hundratals miljoner kronor.

Vid 2013 hade priset nått omkring 100 dollar. De som köpte då kallades för galna. “Digitalt monopolpengar”, sa många. Men de "galna" såg sin investering öka hundrafalt.

Source: CoinGecko

Den första stora rusningen (2014–2017)

Nu började Bitcoin verkligen väcka uppmärksamhet. Priset fluktuerade vilt – ner till 200 dollar 2015, för att sedan skjuta i höjden. I slutet av 2017 nådde det nästan 20 000 dollar.

Plötsligt pratade alla om det. Din tandläkare gav kryptotips. Kassören på ICA kollade Bitcoin-priser på mobilen. Klassisk bubbelkänsla.

Kryptovintern (2018–2020)

Sen kom kraschen. Bitcoin föll tillbaka till cirka 3 200 dollar 2018. Många som köpt nära toppen låg rejält back. En del sålde med förlust och lämnade marknaden för gott.

Men perioden lärde många en viktig sak: Bitcoin rör sig i cykler. Stora uppgångar, rejäla nedgångar – och ibland långa perioder av stillhet.

Den institutionella eran (2021–idag)

Runt 2020 hände något. Stora företag började köpa Bitcoin. Tesla lade till det i sin balansräkning. PayPal öppnade för köp. Plötsligt var det inte bara teknikentusiaster som var intresserade.

Bitcoin nådde nya toppar, föll igen, återhämtade sig. Samma mönster – men med en viktig skillnad: stora institutioner var nu med i leken.

Vad händer med Bitcoin 2025?

Bitcoin har klarat flera marknadscykler, överlevt otaliga "dödsdomar" och fortsätter att studsa tillbaka. Men var står vi just nu?

Aktuella marknadskänslor

Marknaden känns annorlunda jämfört med tidigare. Mindre hype, mer eftertänksamhet. Det finns fortfarande de som tror att Bitcoin ska nå en miljon dollar – men också pensionsfonder som långsamt lägger till det i sina portföljer.

Institutionell närvaro

Stora finansaktörer erbjuder nu Bitcoin-tjänster. Det går att köpa Bitcoin-ETFer genom vanliga mäklare. Företag håller Bitcoin som reserv. Något som var otänkbart för bara några år sedan.

Regleringsläget

Myndigheter jobbar fortfarande på hur Bitcoin ska hanteras, men tonen har förändrats. Istället för förbud handlar det nu mer om tydligare regler. Det kan skapa osäkerhet på kort sikt, men ge stabilitet längre fram.

Varför många känner att de missat tåget

Vi måste också prata om psykologin. Det finns flera skäl till att Bitcoin känns skrämmande för nya intressenter.

- Miljonärsberättelserna. Alla artiklar nämner någon som blev rik snabbt. Det är sant – men ovanligt. Lite som att vinna på lotto.

- Rubrikerna. “Bitcoin rasar 50 %!” får fler klick än “Bitcoin svänger som vanligt”. Mediebilden blir snedvriden.

- Höga priser. När en Bitcoin kostar tiotusentals kronor känns det ouppnåeligt. Men många vet inte att man kan köpa delar av en Bitcoin.

Argumenten för att det INTE är för sent

Begränsat utbud, ökad efterfrågan

Det kommer aldrig finnas mer än 21 miljoner Bitcoin. Samtidigt växer intresset år för år. Enligt enkel ekonomi kan det pressa priset uppåt.

Digitalt guld på uppgång

Många ser Bitcoin som “digitalt guld” – en värdebevarare för den digitala tidsåldern. Om den rollen blir verklighet, finns det utrymme för tillväxt.

Global adoption är i sin linda

De flesta i världen äger fortfarande inte Bitcoin. Om spridningen fortsätter, särskilt i länder med instabila valutor, kan efterfrågan öka kraftigt.

Bättre infrastruktur

Det har blivit enklare att köpa, förvara och använda Bitcoin. Teknisk utveckling leder ofta till bredare användning.

Argumenten för att det KAN vara för sent

Volatiliteten är kvar

Priset svänger fortfarande kraftigt. En nedgång på 20 % på en dag är inte ovanlig, vilket kan vara svårt att hantera.

Osäker reglering

Även om ett totalförbud verkar osannolikt, kan hårda regler sätta käppar i hjulen för tillväxten.

Miljöfrågor

Bitcoin kräver mycket energi. Klimatdebatten kan påverka intresset, särskilt bland institutioner.

Konkurrens

Bitcoin var först – men långt ifrån ensam. Nyare tekniker kan ta över vissa användningsområden.

Vanliga strategier för att närma sig Bitcoin

Månadsvis köp

Vissa köper en liten summa regelbundet, t.ex. 500 kr i månaden. Det jämnar ut priset över tid.

“Kaffepengsstrategin”

Istället för att köpa en kaffe ute varje dag, lägg undan den summan i Bitcoin. Det är pengar du inte direkt saknar.

Tidsramar

De som ser Bitcoin som en långsiktig investering (5+ år) oroar sig ofta mindre för dagliga svängningar.

Rimlig exponering

En vanlig tumregel: investera aldrig mer än du har råd att förlora. För de flesta bör det vara en liten del av portföljen.

Vad säger experterna?

Traditionella rådgivare

Vissa föreslår en liten andel Bitcoin i portföljen, som skydd mot inflation. Andra är mer skeptiska på grund av prisvolatiliteten.

Kryptospecialister

Analytiker inom krypto spår ofta högre priser på lång sikt, baserat på utbud och efterfrågan – men är också tydliga med att det kommer svänga mycket på vägen dit.

Historiska mönster

Tekniker som förändrat världen – internet, smartphones – har ofta vuxit i vågor: först en boom, sen en dipp, sedan stabil tillväxt.

Alternativ till att köpa Bitcoin direkt

Om du är osäker, finns det andra sätt att få exponering.

- Bitcoin-ETF: Går att köpa genom din mäklare, utan att hålla krypto själv.

- Bitcoin-gruvbolag: Vissa företag är specialiserade på mining. Deras aktier påverkas ofta av Bitcoinpriset.

- Blockchain-investeringar: Fokusera på företag som bygger infrastrukturen bakom kryptovärlden.

Vanliga misstag att undvika

- Att investera pengar du inte har råd att förlora

- Att försöka pricka “perfekta” tillfället att köpa

- Att falla för löften om snabba pengar

- Att slarva med säkerheten vid direktköp

- Att låta känslorna styra besluten

Hur man köper Bitcoin säkert (om du bestämmer dig)

Om du bestämmer dig för att köpa Bitcoin via Tap, gör så här:

- Ladda ner appen

- Skapa ett konto och slutför verifieringen

- Öppna din personliga Bitcoin-plånbok i appen

- Ange hur mycket du vill köpa

- Bekräfta köpet – dina Bitcoin läggs till i din plånbok

(För en steg-för-steg-guide, se mer här.)

(Psst: här hittar du en mer detaljerad guide)

Slutsats: Vad är rätt beslut för dig?

Så, är det för sent att köpa Bitcoin?

Bitcoin har överlevt flera nedgångar och kommit tillbaka varje gång. Tekniken väcker fortfarande stort intresse, även bland etablerade aktörer.

Men det är också en mycket volatil tillgång, och ingen vet vad framtiden bär med sig. Ditt beslut bör baseras på din egen ekonomiska situation, din risktolerans och dina mål.

Du behöver inte bestämma dig idag. Läs på, följ marknaden och vänta tills du känner dig trygg. Det viktigaste är att beslutet känns rätt för dig – inte att du följer andras stress eller hype.

Vad är Badger DAO egentligen?

Badger DAO (BADGER) är en decentraliserad autonom organisation som fokuserar på att bygga produkter och infrastruktur för att föra in Bitcoin i decentraliserad finans (DeFi). I kryptovärlden där Bitcoin och DeFi ofta lever separata liv, skiljer sig Badger genom att bygga broar mellan dem. Plattformen gör det möjligt för Bitcoinägare att delta i Ethereums DeFi-ekosystem utan att behöva sälja eller flytta sina BTC.

Låt oss ta en närmare titt på hur Badger försöker lösa utmaningar kring Bitcoin i DeFi, såsom avkastning, interoperabilitet mellan kedjor och tekniska begränsningar.

TL;DR

Bitcoin i DeFi:

Badger skapar infrastruktur som gör det möjligt att använda Bitcoin i Ethereums DeFi via tokeniserade tillgångar som WBTC och renBTC.

Gemenskapsstyrning:

Som en DAO styrs Badger av BADGER-tokeninnehavare, som röstar om beslut kring utveckling, strategier och hur resurser ska användas.

Flerdelat ekosystem:

Består av BadgerDAO (styrning), Sett Vaults (avkastningsstrategier) och DIGG (en elastisk, BTC-kopplad token).

Bakgrunden till Badger DAO

Plattformen lanserades i december 2020 av Chris Spadafora och ett team av DeFi-entusiaster. Det var en rättvis lansering – ingen förförsäljning, inga riskkapitalbolag. Målet var tydligt: göra det möjligt att använda sin Bitcoin inom DeFi-appar utan att tappa exponeringen mot BTC:s prisrörelser.

Badger vill bryta ner de hinder som Bitcoin historiskt haft i DeFi-sammanhang – som begränsade avkastningsmöjligheter, isolerade ekosystem och tekniska svårigheter – genom att använda DAO-styrning och automatiserade strategier.

Sedan lanseringen har plattformen fortsatt utvecklas genom att skapa nya “vaults”, samarbeta med andra DeFi-protokoll och lansera DIGG – en token med elastisk tillgång som speglar Bitcoins pris.

Hur fungerar Badger-plattformen?

Badgers struktur bygger på tre huvudkomponenter:

- BadgerDAO – styrningslagret där innehavare av BADGER-token röstar om förändringar i protokollet och resursanvändning.

- Sett Vaults – “valv” som automatiskt distribuerar tokeniserad BTC i DeFi-protokoll för att generera avkastning.

- DIGG – en elastisk token som speglar BTC:s pris genom att justera sin tillgång utifrån marknadsvärdet.

Governance-funktionen körs på Ethereum, där användarna själva kan föreslå och rösta om förändringar. När någon sätter in sin tokeniserade Bitcoin i en Sett Vault, placeras den automatiskt i olika strategier som optimerats för att generera avkastning – utan att man behöver göra det manuellt.

Hur skyddar Badger användarnas tillgångar?

Badger har byggt en säkerhetsinfrastruktur som inkluderar granskningar från flera oberoende säkerhetsföretag. Protokollet använder även en “timelock” för governance-beslut, vilket innebär att användare hinner agera innan ändringar träder i kraft.

Viktigt att känna till är att Badger utsattes för en säkerhetsincident i december 2021, då cirka 120 miljoner dollar förlorades. Efter det har plattformen satsat på att återskapa förtroendet genom förbättrad säkerhet, fler granskningar och ett starkare community-styrt beslutsfattande.

Protokollets treasury innehåller även en försäkringsfond som kan användas vid oförutsedda händelser.

Fördelarna med Badger-plattformen

Badger gör det enklare för Bitcoinägare att delta i DeFi jämfört med traditionella metoder. Plattformen automatiserar strategier och optimerar avkastning, vilket minskar behovet av teknisk kunskap.

Samtidigt hanterar Badger två av de största utmaningarna för Bitcoin i DeFi:

- Fragmentering – Badger sammanför olika tokeniserade BTC-tillgångar och protokoll i ett enda gränssnitt.

- Tekniska hinder – Gränssnittet är utformat för att vara tillgängligt även för de som inte är tekniskt insatta.

Efter säkerhetsincidenten 2021 har Badger utökat sitt fokus med bättre skydd, planer för multi-chain-support och fler samarbetsprojekt – särskilt inom Layer 2-lösningar och DeFi-protokoll med behov av Bitcoin-likviditet.

Användningsområden för BADGER

Badger gör det möjligt för både privatpersoner och företag att använda sina Bitcoininnehav i DeFi – oavsett om det gäller yield farming, likviditetsutbud eller att låna med BTC som säkerhet utan att sälja den.

Plattformen kombinerar Bitcoins styrka som värdebevarare med DeFi:s avkastningsmöjligheter, vilket ger användarna större kontroll och flexibilitet över sina tillgångar.

Företag kan dessutom använda Badger för att skapa Bitcoinstrategier som ger avkastning utan att ta onödiga risker, tack vare plattformens säkerhetsfokus och interoperabilitet mellan olika blockkedjor.

Så köper du BADGER

Vill du lägga till BADGER i din kryptoplånbok? Då kan du enkelt köpa och sälja tokenen direkt i Tap-appen (efter att du slutfört registrering och verifiering).

Ladda ner appen för att komma igång.

Harvest Finance is a decentralised yield farming protocol that automates the process of earning maximum returns on crypto investments. Launched in 2020 on the Ethereum blockchain, it functions as a yield aggregator that automatically moves users' funds between different DeFi protocols to capture the highest available yields. It now operates on additional blockchains such as Binance Smart Chain and Polygon.

The platform was designed to solve one of the biggest challenges in DeFi yield farming: the time and expertise needed to constantly monitor and switch between different protocols to maximise returns. Instead of users having to do this manually, Harvest Finance does it automatically, making yield farming accessible to everyone.

TLDR

Automated yield farming: Harvest Finance is a DeFi protocol that automatically farms the highest yields available from various DeFi protocols and pools, optimising returns using advanced farming techniques.

Yield aggregator: Harvest Finance serves as a yield aggregator where assets are deposited into strategic vaults to maximise their yield.

Vault system: Users deposit their crypto assets into specialised vaults, receiving fTokens in return that represent their share of the vault and accumulated rewards.

Native token (FARM): FARM is the governance token that allows holders to vote on protocol parameters and share in farming revenue. FARM token holders can vote on proposals for the operational treasury and may receive a fee from Harvest operations

What is Harvest Finance (FARM)?

Harvest Finance simplifies the complex world of yield farming by creating an automated system that does the hard work for users. When you deposit your crypto into a Harvest vault, the protocol automatically deploys your funds to various DeFi platforms that offer the best returns at any given time.

Think of it like having a professional fund manager for your crypto, but instead of a human making decisions, smart contracts automatically move your money to wherever it can earn the most. The protocol automatically farms the highest yield by moving funds between farming pools on your behalf, eliminating the need for users to constantly research and switch between different platforms.

The platform supports various types of assets including stablecoins, popular cryptocurrencies, and liquidity pool tokens. When you deposit assets, you receive fTokens (like fUSDC for USDC deposits) that represent your share of the vault and track your earnings over time.

Harvest Finance's goal is to make yield farming more accessible by automating the process and optimising the potential returns using the latest farming techniques, bringing sophisticated DeFi strategies to everyday users.

Who created Harvest Finance?

The founders of Harvest Finance remain anonymous, which was common for many DeFi projects launched in 2020. The team is completely anonymous, though the project succeeded in attracting a relatively sizable community and has been involved in the community by doling out grants.

Despite the anonymous nature of the founding team, Harvest Finance has built a strong reputation in the DeFi community through its transparent operations and community involvement. The token was distributed via fair launch with no token sales to investors, demonstrating the team's commitment to decentralised principles.

The project launched during the height of the 2020 DeFi summer when yield farming became extremely popular, and the anonymous team capitalised on the growing demand for automated yield optimisation tools.

How does Harvest Finance work?

Vault Strategy System

The platform operates through a system of specialised vaults, each designed for different types of assets and risk profiles. When you deposit crypto into a vault, you receive fTokens that represent your share of that vault's total holdings.

The magic happens behind the scenes, where the protocol's strategies automatically deploy your funds to various DeFi protocols like Compound, Curve, Uniswap, and others based on where they can earn the highest yields. The system constantly monitors yield opportunities and automatically rebalances to maximise returns.

Automated Yield Optimisation

Harvest Finance's protocol design automatically farms the highest available yields and distributes the profits to users in the pool. This means users don't need to understand the complexities of different DeFi protocols or spend time managing their positions.

The protocol uses sophisticated algorithms to determine the best allocation of funds across different yield farming opportunities, taking into account factors like APY rates, smart contract risks, and gas costs for rebalancing.

Profit Sharing Model

When the automated strategies generate profits, these are shared among all users in the vault proportional to their deposits. A portion of the profits is also distributed to FARM token holders who stake their tokens in profit-sharing pools, creating an additional incentive layer for the community.

What is FARM?

FARM serves as the governance and profit-sharing token of the Harvest Finance ecosystem:

- Governance Rights: Holders can vote on protocol parameters and propose or veto the introduction of new Vaults, giving the community control over the platform's direction.

- Profit Sharing: FARM, when deposited in Profit Sharing pools, becomes a means of participating in farming revenue, allowing token holders to earn a share of the protocol's success.

- Protocol Incentives: Harvest at launch required a native crypto so as to be able to incentivise yield farmers, and allow Harvest to stake other platforms and collect rewards in return.

- Community Participation: The token creates alignment between users and the protocol's long-term success, as both benefit from higher yields and more efficient farming strategies.

FARM operates as an ERC-20 token on Ethereum, making it compatible with the broader DeFi ecosystem and easily tradeable on decentralised exchanges. While FARM is originally an ERC-20 token, it also exists on other blockchain platforms such as Polygon and Binance Smart Chain, expanding to multiple blockchains to offer yield farming opportunities across different ecosystems

How can I buy and sell FARM?

For those looking to participate in automated yield farming, FARM tokens are readily available through the Tap app. You can purchase, sell, and store FARM tokens securely while managing them alongside your broader crypto portfolio.

Numeraire är ett banbrytande projekt som kombinerar dataanalys, AI och blockchain för att skapa vad som beskrivs som världens första AI-drivna och crowdsourcade hedgefond. Det grundades i oktober 2015 av Richard Craib, en sydafrikansk teknolog, och representerar ett helt nytt sätt att närma sig finansmarknaderna.

I stället för att förlita sig på traditionella analytiker, låter Numerai tusentals data scientists världen över tävla om att bygga de mest träffsäkra maskininlärningsmodellerna för börsprognoser – modeller som sedan styr hedgefondens faktiska investeringsbeslut.

TL;DR

AI-styrd hedgefond:

Numeraire (NMR) är en Ethereum-baserad token som används i Numerai – en hedgefond baserad i San Francisco som fattar beslut med hjälp av AI, utan mänskliga känslor.

Data science-tävling:

Numerai anordnar världens tuffaste datatävling, där deltagare belönas med NMR-tokens för modeller som förbättrar fondens resultat. Mer än 200 000 USD delas ut varje månad.

Crowdsourcade prognoser:

Deltagare använder Numerais krypterade data för att skapa maskininlärningsmodeller och skicka in sina prognoser, som sedan utvärderas och belönas.

Staking-mekanism:

För att delta måste användare hålla och satsa NMR-tokens – både för att visa förtroende för sina modeller och för att få tillgång till olika funktioner i ekosystemet.

Hur fungerar Numeraire?

Numerai använder ett unikt system där hedgefondens strategi formas av en global datatävling. Så här går det till:

- Numerai släpper anonymiserad, krypterad finansiell data varje vecka.

- Data scientists laddar ner datan och bygger modeller som förutspår hur aktier kommer prestera.

- Prognoserna skickas in och utvärderas utifrån hur väl de stämmer med marknadsutfallet.

För att delta på riktigt måste deltagare satsa (stakea) NMR-tokens på sina inskickade modeller. Går det bra? Då får de mer NMR. Går det dåligt? Då förloras en del av insatsen. Den här mekanismen uppmuntrar till kvalitet framför kvantitet – du måste tro på dina egna modeller.

Till skillnad från många andra projekt använder Numerai inte en enskild vinnande modell. Istället kombineras de mest framgångsrika bidragen till en större “meta-modell” som fonden baserar sina investeringar på. Det gör systemet mer motståndskraftigt än om man bara litade på en enda förutsägelse.

Vem skapade Numeraire?

Richard Craib grundade Numerai 2015. Han studerade matematik och ekonomi vid University of Cape Town och senare på University of California, Berkeley. Innan Numerai arbetade han inom globala aktiemarknader, bland annat på Prudential (M&G).

Craib ville bygga en ny typ av hedgefond – en som drivs av kollektiv intelligens, transparenta incitament och teknik, snarare än traditionella analytiker. Numerai har sedan dess vuxit till att attrahera några av världens skarpaste data scientists.

Vad är NMR?

NMR är den inbyggda tokenen i Numerai-ekosystemet och används för flera viktiga funktioner:

- Tävlingar: Deltagare måste satsa NMR för att delta i tävlingarna och tjäna belöningar.

- Styrning: Tokeninnehavare kan delta i beslut kring plattformens framtid och förändringar.

- Incitament: Den staking-baserade modellen säkerställer att deltagarna bidrar med seriösa modeller.

- Belöningar: Numerai delar ut över 200 000 USD i NMR varje månad till framgångsrika modeller.

Tokenen är en ERC-20-token och fungerar smidigt inom hela Ethereum- och DeFi-ekosystemet.

Hur kan jag köpa och sälja NMR?

Du kan enkelt köpa, sälja och hantera NMR direkt i Tap-appen, tillsammans med dina övriga kryptotillgångar. Appen erbjuder ett enkelt gränssnitt och säker förvaring, vilket gör det lätt att komma igång.

Värt att nämna är att NMR:s utveckling är nära kopplad till Numerais hedgefonds framgång och tillväxten av dess globala nätverk av data scientists.

Livepeer är ett decentraliserat nätverk för videostreaming, med målet att göra videoinnehåll mer tillgängligt och prisvärt för alla. Projektet lanserades 2017 och var det första fullt decentraliserade live-videoprotokollet – ett alternativ till traditionella, centraliserade streamingtjänster som YouTube och Twitch.

Plattformen fungerar genom att koppla samman innehållsskapare med datoroperatörer som tillhandahåller datorkraft. Denna peer-to-peer-modell kan minska kostnaderna för videobehandling med upp till 50–90 % jämfört med molnbaserade lösningar, samtidigt som kvaliteten bibehålls.

TL;DR

Decentraliserad videoinfrastruktur:

Livepeer bygger ett nätverk där AI-bearbetning och videotranskodning kan utföras av oberoende noder i stället för dyra serverhallar.

Kostnadseffektiv streaming:

Tack vare sin decentraliserade marknadsplats kan Livepeer erbjuda konkurrenskraftiga priser och tillförlitliga tjänster till utvecklare och plattformar.

Ethereum-baserat protokoll:

Byggt på Ethereum ger det utvecklare frihet att skapa videolösningar utanför storföretagens kontroll.

LPT-tokenen:

Livepeers inbyggda token används för staking och styrning av nätverket, inte som direkt betalningsmedel.

Hur fungerar Livepeer?

När någon vill streama video använder de normalt stora serverhallar för att bearbeta innehållet. Livepeer gör det istället möjligt att distribuera jobbet över ett globalt nätverk av datorer – så kallade orchestrators – som hjälper till att transkoda video till olika kvaliteter (t.ex. 1080p, 720p, 480p). Det gör att videor fungerar oavsett enhet eller internetuppkoppling.

Det här gynnar både innehållsskapare, tittare och datoroperatörer:

- Skapare betalar mindre för högkvalitativ streaming

- Operatörer tjänar pengar genom att bidra med datorkraft

- Tittare får samma upplevelse som på traditionella plattformar

För utvecklare innebär det ett billigt, flexibelt och decentraliserat alternativ till att själva bygga upp videoinfrastruktur.

Vem ligger bakom Livepeer?

Livepeer grundades 2017 av Doug Petkanics (CEO) och Eric Tang (CTO) – två mjukvaruutvecklare med lång erfarenhet av startupvärlden. Doug har tidigare varit med och grundat Wildcard och studerat vid University of Pennsylvania, medan Eric är teknisk visionär med fokus på hur blockchain kan effektivisera streaming.

De såg hur videoinnehåll blev allt dyrare att distribuera, samtidigt som några få stora aktörer kontrollerade större delen av infrastrukturen. Livepeer föddes ur idén att göra streaming mer öppet och decentraliserat – utan att tumma på kvalitet eller prestanda.

Transkodningsnätverket

Grunden i Livepeer är dess videotranskodningsnätverk. Varje gång en video ska streamas behöver den konverteras till flera olika format för att fungera på olika enheter och nätverk. Det är det här jobbet som Livepeer distribuerar över tusentals datorer världen över.

Operatörerna tävlar om att erbjuda bästa möjliga tjänst till lägsta pris, vilket skapar ett naturligt effektivt system där kvalitet och kostnad balanseras.

Säkerhet och staking

För att få utföra arbete i nätverket måste operatörerna stakea LPT-tokens. Det fungerar som en säkerhetsinsats – om de fuskar eller levererar dålig service riskerar de att förlora sina tokens. Det här håller kvaliteten hög.

Andra användare kan också välja att delegera sina LPT till operatörer de litar på, och i gengäld få en andel av belöningarna, utan att själva behöva köra någon hårdvara.

Ekonomiska incitament

Livepeer fungerar som en öppen marknadsplats för videobearbetning. De operatörer som erbjuder bäst kombination av pris, tillförlitlighet och kvalitet får jobben. Själva betalningarna sker i ETH eller andra kryptovalutor, medan LPT används för staking, governance och belöningar.

Vad är LPT?

LPT är Livepeers native token och används inte främst som betalmedel utan för att:

- Säkra nätverket: Operatörer måste stakea LPT för att få jobba i nätverket

- Styra protokollet: Tokeninnehavare kan rösta om viktiga beslut och uppgraderingar

- Få belöningar: Genom delegation kan du få en del av intäkterna från operatörer

- Utföra arbete: LPT representerar rätten att bidra till nätverket och tjäna på videobearbetning

Tokenen följer en inflationsmodell där nya LPT skapas som belöning – men värdet balanseras av användning och nätverkets tillväxt.

Hur köper och säljer man LPT?

Nyfiken på att utforska LPT? Du kan enkelt köpa, sälja, handla och lagra Livepeer-tokenen direkt i Tap-appen – tillsammans med dina andra digitala tillgångar.

Eftersom LPT:s värde är kopplat till hur mycket Livepeers infrastruktur används, påverkas efterfrågan av hur många utvecklare och innehållsskapare som väljer att bygga på plattformen.