Learning the friendly way

Dive into our resources, guides, and articles for all things money-related. Grow your financial confidence with our experts curated tips and articles for both experienced and new investors.

LATEST ARTICLEs

Bitcoin and Ethereum dominate headlines, but they represent just one approach to distributed ledger technology. While most projects iterate on blockchain's foundational concepts, Hedera Hashgraph (HBAR) takes a different approach, pursuing an entirely different architectural philosophy.

The result is a network engineered for enterprise-grade performance - processing thousands of transactions per second with deterministic fees and minimal energy consumption. Where many blockchain networks struggle with the scalability trilemma, Hedera's hashgraph consensus mechanism offers a compelling alternative that doesn't sacrifice security for speed.

What distinguishes Hedera in practice is its enterprise adoption trajectory. Major corporations across finance, healthcare, and supply chain management have moved beyond pilot programs to production deployments. This isn't theoretical adoption - it's measurable network activity from organizations with serious compliance and performance requirements.

Hedera has positioned itself as one of the most corporate-friendly distributed ledger technologies (DLTs) available today. But how exactly does it work, and why does it stand apart from the blockchain crowd?

The Basics: What Is Hedera Hashgraph?

Launched in 2018, Hedera Hashgraph is a distributed ledger technology that offers a genuine alternative to blockchain architecture. Instead of organizing transactions into sequential blocks like a digital filing cabinet, Hedera uses a directed acyclic graph (DAG) structure called the hashgraph. Think of it more like a web of interconnected transactions.

This design allows multiple transactions to be processed in parallel rather than waiting in a single-file line. The result? Hedera can handle over 10,000 transactions per second (TPS) with finality in just a few seconds, while Bitcoin manages about 6–8 TPS and Ethereum handles 12–15 TPS.

At its core, Hedera is engineered to tackle three persistent challenges that have plagued distributed ledger technology:

- Transactions settle in seconds, not the minutes or hours you might wait with other networks. This makes it possible to build applications where timing actually counts.

- Scalability without the usual trade-offs, The network can handle thousands of transactions simultaneously without slowing down or getting expensive when things get busy. Most blockchains struggle with this balancing act.

- Energy use that makes sense, unlike networks that consume as much electricity as small countries, Hedera runs efficiently enough that companies don't have to justify massive energy bills to their boards.

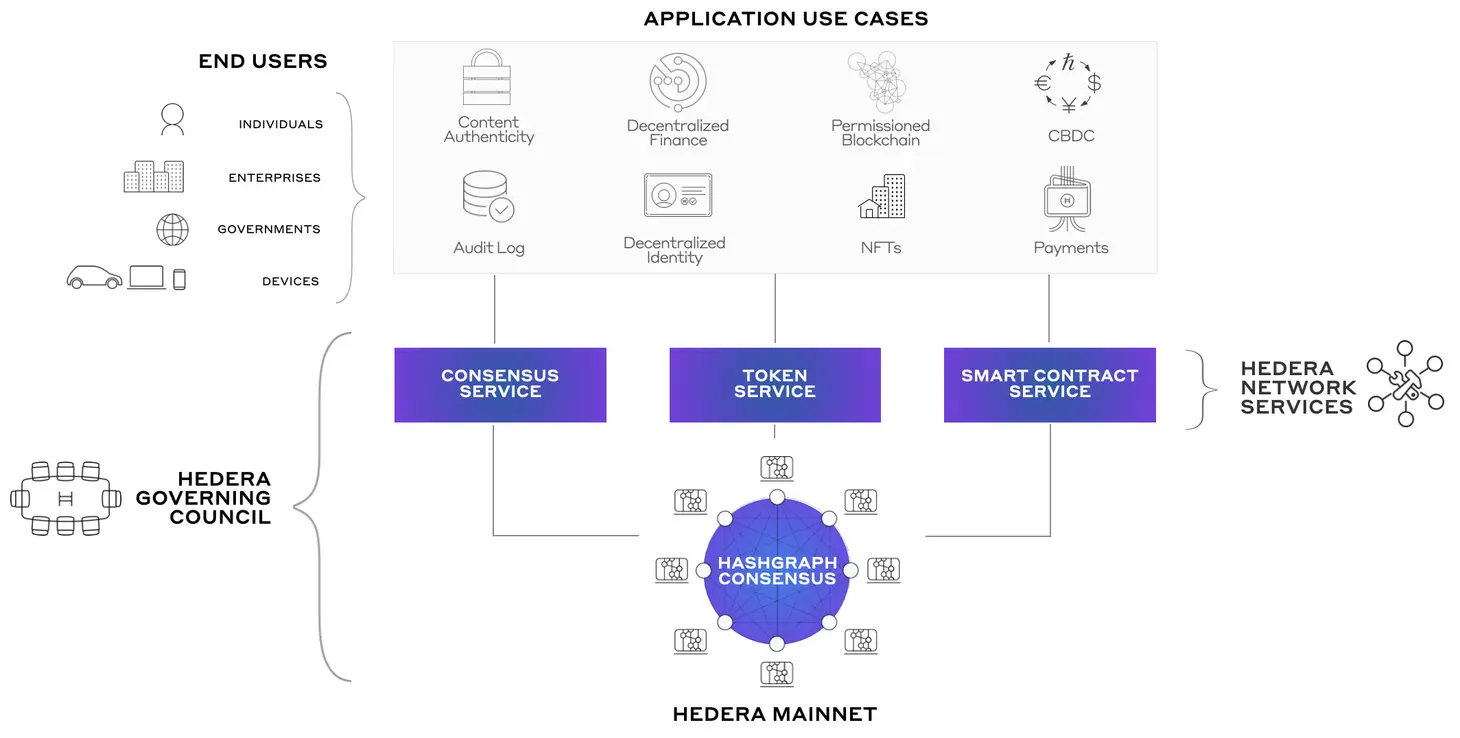

How Hedera Works: Gossip and Virtual Voting

Hedera's performance stems from its unique consensus mechanism, which combines two clever innovations that work together like a well-orchestrated dance.

Instead of broadcasting every transaction to the entire network simultaneously (imagine shouting news in a crowded room), nodes "gossip" by randomly sharing information with a few neighbors. Those nodes then pass it along to their neighbors, creating a ripple effect. Over time, the entire network organically learns about every transaction without the communication overhead. That is known as the “gossip-about-gossip protocol”.

Virtual voting is where things get interesting: once all nodes have the same historical record of gossip, they can independently calculate how the network would vote on each transaction. No actual vote messages need to be sent across the network. The outcome is mathematically deterministic based on the gossip history, saving significant time and bandwidth.

Together, these methods achieve asynchronous Byzantine fault tolerance (aBFT), which represents one of the highest levels of security available in distributed systems. This means the network can reach consensus and continue operating even if up to one-third of nodes act maliciously or fail completely.

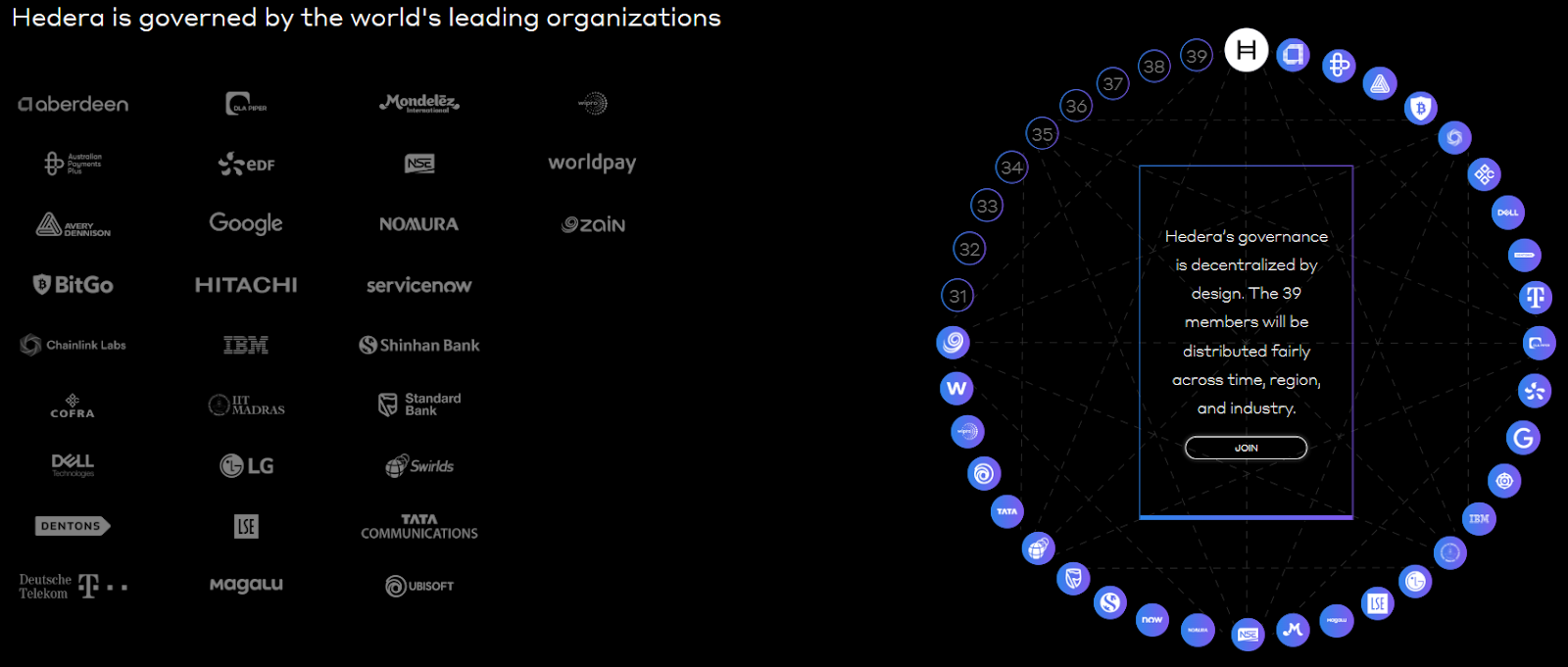

Governance: The Hedera Council

Perhaps the most controversial, and arguably the most distinctive, aspect of Hedera is its governance model. Instead of leaving critical network decisions to anonymous miners or distributed token holders, Hedera operates under a Governing Council of up to 39 well-known global organizations.

Current members include companies like Google, IBM, Dell, Boeing, Standard Bank, Ubisoft, and other established corporations. Each council member holds an equal vote on network decisions, including software upgrades, fee structures, and treasury management.

The rationale is straightforward: provide stability, accountability, and long-term strategic planning. However, this structure has sparked ongoing debate within the crypto community. Critics argue it reduces decentralization compared to blockchain networks where theoretically anyone can participate in governance, while supporters contend it offers the predictability that many enterprises require for serious adoption.

Key Services of Hedera

Hedera functions as more than just a payment network. The platform offers three core services that developers and enterprises can leverage to build decentralized applications:

Hedera Consensus Service (HCS): Provides secure, immutable logs of events and data. This proves particularly valuable for supply chain tracking, regulatory audits, and maintaining data integrity in heavily regulated industries like healthcare and finance.

Hedera Token Service (HTS): Enables the creation and management of various token types, including stablecoins, NFTs, and tokenized assets. Built-in features like account-level controls and compliance tools make it especially appealing for enterprises that need to meet regulatory requirements.

Hedera Smart Contract Service (HSCS): Supports Ethereum-compatible smart contracts, allowing developers to build DeFi applications, games, and automation tools while benefiting from Hedera's superior speed and substantially lower transaction fees.

Real-World Applications

Hedera's enterprise-focused approach has translated into practical implementations across multiple sectors:

- Finance: Standard Bank leverages Hedera's infrastructure for faster, more transparent cross-border payment processing.

- Supply chain: Companies like Suku and Avery Dennison use Hedera for product traceability and logistics management, providing end-to-end visibility.

- Healthcare: Safe Health Systems employs the network to securely log medical and clinical trial data while maintaining strict patient privacy standards.

- Gaming: Animoca Brands integrates Hedera's technology to create fair and tamper-proof in-game economies and digital asset management.

- Sustainability: Environmental organizations use Hedera's consensus service to track carbon credits and monitor environmental impact data with immutable records.

These implementations highlight Hedera's positioning as an enterprise-focused platform, creating a distinct contrast to networks that primarily serve DeFi protocols or retail trading activities.

Understanding HBAR: The Native Token

Like most distributed ledger technologies, Hedera operates with its own native cryptocurrency: HBAR. The token serves two fundamental purposes within the ecosystem:

- Network fuel: HBAR is required to pay transaction fees and access network services, including consensus operations, tokenization features, and smart contract execution.

- Network security: Node operators stake HBAR tokens to participate in consensus and help secure the network infrastructure.

One of Hedera's most practical advantages lies in its cost structure. A typical transaction costs approximately $0.0001, it’s economical enough to enable microtransactions and machine-to-machine payment scenarios that would be prohibitively expensive on other networks.

The total supply of HBAR is capped at 50 billion tokens. The distribution follows a controlled release schedule designed to avoid sudden market flooding while ensuring adequate liquidity for network operations.

How Hedera Compares to Other Networks

To understand Hedera's market position, it's helpful to consider how it stacks up against established blockchain models:

Proof-of-Work (PoW), exemplified by Bitcoin, is highly secure and battle-tested, but notoriously slow and energy-intensive.

Proof-of-Stake (PoS), used by Ethereum 2.0, is more energy-efficient than PoW, but can lead to wealth concentration among large token holders.

Lastly, Hedera Hashgraph uses gossip protocols and virtual voting to achieve speed, security, and efficiency simultaneously, while operating under corporate governance rather than anonymous network participants.

The trade-off is crystal-clear. Hedera prioritizes corporate trust, performance, and regulatory clarity, while accepting criticism that it may sacrifice some degree of decentralization compared to traditional blockchain networks.

The Challenges Ahead

Despite its technical strengths and enterprise adoption, Hedera faces some hurdles that could impact its long-term trajectory. The Governing Council model continues to raise questions about whether Hedera represents genuine decentralization or simply distributed corporate control, a debate that matters deeply to the broader crypto community's acceptance. Meanwhile, established networks like Solana, Avalanche, and Ethereum maintain their dominance over ecosystem development, making it challenging for Hedera to attract the vibrant developer communities that drive innovation.

The platform also faces an adoption challenge. While it excels in enterprise use cases, Hedera could broaden its appeal beyond corporate applications to achieve the kind of recognition that sustains long-term growth. Moreover, like all cryptocurrency projects, Hedera must navigate evolving regulatory frameworks across multiple jurisdictions, each with their own compliance requirements and restrictions.

Nevertheless, Hedera's focus on performance, enterprise-grade reliability, and regulatory compliance could provide resilience in certain market conditions where other projects would struggle to maintain institutional confidence.

HBAR ETF on the Horizon

Over the past several months, talk of a potential HBAR ETF has gained traction. An ETF would offer institutional and retail investors exposure to HBAR without needing to manage wallets, private keys, or direct custody. That kind of access lowers the entry-level barrier. Moreover, SEC approval of a Hedera ETF would imply a level of oversight, due diligence, and compliance that can help reduce perceived risks among cautious or regulated investors. It puts HBAR closer to the realm of mainstream finance instruments.

The U.S. Securities and Exchange Commission (SEC) recently pushed back the decision on the Canary HBAR ETF to November 8. The ETF was proposed by Nasdaq back in February; the SEC has delayed the decision twice already. Despite the most recent delay, however, market analysts remain optimistic. Bloomberg’s analysts, for instance, maintain a 90% likelihood of ETF approval in the near term.

The Future of Hedera

Hedera stands out in a crowded field by taking a completely different approach than most blockchain projects. Instead of following the usual playbook, they built something that actually works for businesses: fast transactions, costs you can predict, and energy usage that won't make your CFO cringe.

The real test isn't whether Hedera can keep doing what it's doing well. It's whether they can stay relevant as the whole distributed ledger world keeps evolving at breakneck speed. But here's the thing: while everyone else was busy trying to be the next Bitcoin, Hedera quietly built something that Fortune 500 companies actually want to use.

Whether that bet pays off long-term is anyone's guess. What's not up for debate is that they've proven there's more than one way to build a distributed ledger, and sometimes the road less traveled leads somewhere pretty interesting.

Let's Talk About Getting Your Crypto to Work While You Sleep

Remember when your grandparents bragged about their 2% savings account? Those days feel like ancient history now that crypto APY percentages are floating around that would make a traditional banker faint. But hold up, before you start dreaming about retiring next month on those sweet, sweet yields, let's dive into what APY actually means and why some of these numbers look like lottery tickets.

What the Is APY, Anyway?

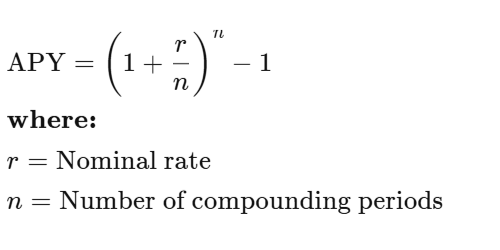

Think of APY as compound interest on steroids. While your bank's savings account sits there earning dust, APY measures how much your money can actually grow in a year when interest keeps building on top of interest. The faucet of passive income is now open.

Here's a reality check: Park $1,000 in your bank at 5% simple interest, and you'll have a whopping $1,050 after a year. Yawn, boring… But that same money with 5% APY compounded monthly? You're looking at $1,051.16.

"Big deal, that's only a dollar!" you might say. But here's where it gets interesting. Over time, that compounding effect turns into a money snowball rolling down a mountain. The difference between simple interest and compound interest isn't just pennies; it's the difference between walking and taking a rocket ship.

APY vs. APR: The Sibling Rivalry You Need to Understand

Okay, confession time…even seasoned crypto folks mix these up. Here's your cheat sheet:

APY (Annual Percentage Yield): What you earn when you lend out your crypto. The higher, the better for your wallet.

APR (Annual Percentage Rate): What you pay when you borrow crypto. Lower is your friend here.

Think of it this way: APY is the cool cousin who brings you money, while APR is the one who always asks to borrow twenty bucks.

For a more detailed comparison, click here.

Where Does APY Show Up in Crypto?

- Crypto "Savings Accounts"

Some platforms let you deposit your tokens and watch them multiply. It's like putting your crypto to work at a job that actually pays decent wages. Your coins get lent out to traders who need them, and you get a cut of the action.

- Staking: Become a Network Validator

With Proof-of-Stake blockchains like Ethereum or Cardano, you can "stake" your tokens to help secure the network. Think of it as being a digital security guard who gets paid in crypto. The network stays safe, and you earn rewards. Win-win.

- Yield Farming: The Wild West of DeFi

This is where things get interesting, and a bit crazy. You provide liquidity to decentralized exchanges, and in return, you earn trading fees plus shiny new governance tokens. Early yield farmers sometimes see APYs that look like phone numbers, but don't get too excited; those rates have a habit of crashing back to earth.

- Lending Protocols: Become the Bank

Platforms like Aave and Compound let you play banker. You lend your tokens, borrowers pay interest, and you collect the proceeds. APY goes up when everyone wants to borrow your particular flavor of crypto, and down when the demand cools off.

Why Are Crypto APYs So High?

While your bank offers you a measly 0.5%, crypto platforms are throwing around eye-watering numbers like 10%, 50%, or even 1,000%+. Here's why:

Crypto traders will pay premium rates to short a token or execute complex arbitrage strategies. Supply and demand at its finest.

Hype for new projects also plays a role. Fresh projects often throw ridiculous APYs at users to attract liquidity. It's like a grand opening sale, but with more zeros.

Risk gets factored in. Let's be real, crypto can get risky at times. Higher returns compensate for the white-knuckle ride.

Finally, token Incentives can play a role too. Many of those eye-popping APYs come partially from project tokens that could moon... or crater. It's the crypto Russian roulette.

The Math Behind the Magic

Don't worry, we're not about to turn this into a calculus nightmare. The APY formula is actually pretty straightforward:

Example: 10% interest compounded monthly gives you about 10.47% APY. Compound it daily? You're looking at 10.52%. In crypto, some protocols compound every block, which is like compounding every few seconds. Your calculator might start smoking.

The Fine Print

Before you quit your day job and become a full-time yield farmer, let's talk about the risks that nobody likes to mention at crypto parties. First up is volatility. Sure, your APY might be 20%, but if your token's price drops 50%, you're still in the red. Math is cruel like that. Then there's impermanent loss, which sounds harmless but can eat into your gains faster than you can say "automated market maker" when you're providing liquidity and token prices start dancing around.

Don't forget about smart contract risk, either. DeFi protocols are basically computer programs holding billions of dollars, and if they break, funds can disappear into the digital ether without so much as a goodbye note. Platform risk is equally sobering. Remember Celsius? FTX? Sometimes the platforms themselves go belly-up, taking user funds with them like the Titanic.

Last but not least, there’s APY whiplash. That jaw-dropping 100% APY you bookmarked yesterday? It might be 15% today because crypto moves fast. Rates fluctuate based on demand, new competition, token economics, and sometimes just because the crypto gods felt like shaking things up.

What's a "Good" APY?

- Conservative. Sticking to blue-chip assets and reputable platforms for 3-8% APY. For the faint of heart.

- Moderate. Staking some altcoins or providing liquidity for 10-20% APY. There’s some excitement, but not heart-attack levels.

- High (YOLO). Chasing new DeFi projects for 50-100%+ APY. It’s worth keeping in mind there’s a non-zero chance your tokens might become expensive digital art.

Remember, if an APY looks too good to be true, it's probably attached to risks that would make a hedge fund manager nervous.

Crystal Ball Time: The Future of APY in Crypto

Here's where things get interesting. As crypto grows up, APYs are starting to act less like lottery tickets and more like actual financial products. Big institutions are getting into staking, regulators are paying attention, and the wild west is slowly becoming a proper town with actual roads.

It’s likely crypto will keep offering better yields than traditional finance. It's just that the 10,000% APY days are likely becoming a fond memory.

The Bottom Line

APY in crypto is the same mathematical concept your finance professor taught you, just dressed up in digital clothing and offering significantly better rates. Whether you're staking, lending, or yield farming, understanding APY helps you separate the wheat from the chaff and the legitimate opportunities from dubious schemes.

APY isn't a cheat code to infinite money. It's a tool that, when used wisely, can help your crypto actually work for you instead of just sitting in your wallet looking pretty. But like everything in crypto, it comes with risks that deserve respect and careful consideration.

It’s worth remembering the best APY in the world is worthless if the underlying project disappears into the digital sunset. Choose wisely, diversify smartly, and may your compounds be ever in your favor.

Why can't a fully compliant, regulated crypto business secure a bank account in 2025?

If you're operating in this space, you already know the answer. You've lived through it. You've submitted the documentation, walked through your AML procedures, and demonstrated your regulatory compliance… only to be rejected. Or worse still, waking up to find your existing account frozen, with no real explanation and no path forward.

This isn't about isolated cases or bad actors being weeded out. It's a pattern of systematic risk aversion that's creating real barriers to growth across the entire sector, and it's throttling one of the most significant financial innovations of our generation.

We're Tap, and we're building the infrastructure that traditional banks refuse to provide.

The Economics Behind the Blockade

Let's examine what's actually driving this exclusion, because it's rarely about the reasons banks cite publicly.

The European Banking Authority has explicitly warned against unwarranted de-risking, noting it causes "severe consequences" and financial exclusion of legitimate customers. Yet the practice continues, driven by two fundamental economic pressures that have nothing to do with your business's actual risk profile.

The compliance cost calculation

Financial crime compliance across EMEA costs organizations approximately $85 billion annually. For traditional banks, the math is simple: serving crypto businesses requires specialized expertise, enhanced monitoring, and ongoing due diligence. As a result, it's cheaper to reject the entire sector than to build the infrastructure needed to serve it properly.

The regulatory capital burden

New EU regulations impose a 1,250% risk weight on unbacked crypto assets such as Bitcoin and Ethereum. This isn't a compliance requirement; it's a capital penalty that makes crypto exposure commercially unviable for traditional institutions, regardless of the actual risk individual clients present.

In the UK, approximately 90% of crypto firm registration applications have been rejected or withdrawn, often citing inadequate AML controls. Whether those assessments are accurate or not, they've created the perfect justification for blanket rejection policies.

The result? Compliant businesses are being treated the same as bad actors; not because of what they've done, but because of the sector they're in.

The Real Cost of Financial Exclusion

Financial exclusion isn’t just an hiccup; it creates tangible operational barriers that ripple through every part of running a crypto business.

Firms that have secured MiCA authorization, built robust compliance programs, and met regulatory requirements can find themselves locked out of basic banking services. Essential fiat on-ramps and off-ramps remain inaccessible, slowing payments, limiting growth, and complicating cash flow management.

Individual cases illustrate the problem vividly as well. Accounts are closed because a business receives a payment from a regulated exchange. Others are dropped with vague references to “commercial decisions,” offering no substantive justification. Founders frequently struggle to separate personal and business finances, as both are considered too risky to serve.

The irony is striking. By refusing service to compliant businesses, traditional banks aren’t mitigating risk; they’re amplifying it. Forced to operate through less regulated channels, these legitimate firms face higher operational and compliance risks, slower transactions, and reduced investor confidence. Over time, this slows innovation, and raises the cost of doing business for firms that are legally and technically sound.

Debanking Beyond Europe: U.S. Crypto Firms Face Their Own Challenges

Limited access to banking services isn’t exclusive to Europe. Leading firms in the U.S. crypto industry have faced numerous challenges regarding the banking blockade. Alex Konanykhin, CEO of Unicoin, described repeated account closures by major banks such as Citi, JPMorgan, and Wells Fargo, noting that access was cut off without explanation. Unicoin’s experience echoes a broader sentiment among crypto executives who argue that traditional financial institutions remain wary of digital asset businesses despite recent policy shifts toward a more pro-innovation stance.

Jesse Powell, co-founder of Kraken, has also spoken out about being dropped by long-time banking partners, calling the practice “financial censorship in disguise.” Caitlin Long, founder of Custodia Bank, recounted how her institution was repeatedly denied services. Gemini founders Tyler Winklevoss and Cameron Winklevoss shared similar frustrations.

These experiences reveal a pattern many in the industry interpret as systemic risk aversion. Even in a market as large and mature as the United States, crypto-focused businesses continue to encounter obstacles in maintaining basic financial infrastructure. The issue became especially acute after the collapse of crypto-friendly banks such as Silvergate, Signature, and Moonstone; institutions that once served as key bridges between fiat and digital assets. Their exit left a gap few traditional players have been willing to fill.

Why Tap Exists

The crypto industry has reached an inflection point. Regulatory frameworks like MiCA are providing clarity. Institutional adoption is accelerating. The technology is proven and tested. But the fundamental infrastructure gap remains: access to business banking that actually works for digital asset businesses.

This is precisely why we built Tap for Business.

We provide business accounts with dedicated EUR and GBP IBANs specifically designed for crypto companies and businesses that interact with digital assets. This isn't a side offering or an experiment, it's our core focus.

Our approach is straightforward

We built our infrastructure for this sector

Rather than retrofitting traditional banking systems to reluctantly accommodate crypto businesses, we designed our compliance, monitoring, and operational frameworks specifically for digital asset flows. This means we can properly assess and serve businesses that others automatically reject.

We price in the actual risk, not the sector

Blanket rejection policies exist because they're cheap and simple. We take a different approach: evaluating each business based on their actual controls, compliance posture, and operational reality. It costs more, but it's the only way to serve this market properly.

We're committed to sector normalization

Every time a legitimate crypto business is forced to operate without proper banking infrastructure, it reinforces outdated stigmas. By providing professional financial services to compliant businesses, we're helping demonstrate what should be obvious: crypto companies can and should be served by the financial system.

It isn't about taking on risks that others won't. It's about properly evaluating risks that others refuse to understand.

Moving Forward

The industry is maturing. Regulatory clarity is emerging. Institutional adoption is accelerating. But you can't put your business on hold while traditional banks slowly catch up to reality.

That's not sustainable in the long run.

As a firm, you shouldn't have to beg for a bank account. You shouldn't have to downplay your crypto operations just to access basic financial services. And you certainly shouldn't have to accept that systematic exclusion with little to no explanation other than “It’s just how things are."

The crypto sector is building the future of finance. Your banking partner should believe in that future too. If you're ready to work with financial infrastructure built for your business, not in spite of it, here we are.

Talk today with one of our experts to understand how we can help your business access the banking infrastructure you need.

As 2025 comes to a close, Bitcoin is still standing at a crossroads. From its recent drop to a low near $80,000 to a rebound above $94,000, price action has been volatile, and sentiment even more so. What follows is a deeper look at what could shape Bitcoin’s path through the year-end: who’s holding, what’s shifting under the surface, and which scenario is playing out now.

What’s Working Under the Hood

Whales Keep Hoarding

After a period of heavy distribution, large-holder wallets are showing renewed accumulation. According to recent on-chain data, whales resumed accumulation in early December, netting nearly 47,600 BTC after offloading over 113,000 BTC between October and November.

This shift stabilizes price around the $89,000 to $92,000 zone and signals renewed confidence from some of the biggest holders. Meanwhile exchange balances keep making lower lows in spite of recent volatility, which suggests selling pressure may be diminishing.

Liquidity, Rate Cuts & Risk Appetite Are Back in the Menu

Bitcoin’s prospects aren’t just about on-chain flows. Macro conditions seem to be aligning too. Growing odds of a rate cut by the Federal Reserve could fuel a late-year rebound for crypto more broadly. That said, macro risks remain real: global economic uncertainty, rate-sensitive flows, and volatility in the stock market mean BTC could remain tethered to broader risk sentiment. Still, if liquidity conditions improve and the environment remains risk-on, Bitcoin and crypto as a whole could benefit.

Key Technical Zones & What They Mean

Right now, Bitcoin trades around $92,000, having tested $94,500 in the past 24 hours. That places BTC squarely in a “decision zone.” On one side lies the psychological resistance zone near $100,000 to $105,000, with the 200-day moving average rubbing the $100,000 level. How price behaves inside these zones, will likely determine if we see a year-end push or a drawn-out consolidation.

Two Scenarios for the Closing Days of 2025

Scenario A: Stabilization

This is the base case. It assumes:

- Continued whale accumulation and reduced exchange supply

- Macro tailwinds from improved liquidity and calming rate expectations

- Spot demand (retail + institutional) remains stable or improves

BTC could nudge toward the $100,000 resistance level. A clean break above this level (particularly if on-chain flows remain constructive and spot demand returns) would be a technical development worth watching, as it could open the door to a retest of recent highs or further upward movement.

Scenario B: Quiet Consolidation

In this scenario, volatility remains high, but structural forces push for balance rather than breakout. That might occur if:

- Macro risks re-emerge (rate uncertainty, global liquidity tightening)

- Spot demand remains timid or institutional flows stall

- Whales stay cautious and accumulation slows

This is what could play out. BTC trades sideways through year-end. The $100,000 mark remains elusive, perhaps tested a few times, but never cleanly taken out. Consolidation would become the theme. On the flip side, this path would offer stability and may set up a more sustainable base.

Nothing is set in stone, especially in crypto. More extreme scenarios remain possible, from a retest of the $75,000 to $80,000 zone to a fresh push toward new all-time highs. But based on current market sentiment and derivatives positioning, the scenarios outlined above represent the most grounded paths forward.

A Quiet Setup with Potential

Bitcoin doesn’t seem to be roaring toward $150K or 200K by year-end like many expected a few months ago. What’s playing out instead is quieter and more foundational. If this foundation holds, Bitcoin could grind higher toward the $100,000 to $105,000 zone before 2026, in an optimistic but a realistic scenario. If macro turbulence or weak demand returns, however, consolidation around the low $90ks remains the most likely path.

Sure, 2025 hasn't delivered the explosive rally some had circled on their calendars. But beyond price action, the foundation is strengthening: institutional adoption is accelerating, regulatory clarity is emerging, and infrastructure is maturing faster than ever. And let's not forget, December has delivered surprises before. Bitcoin has a history of wrapping up the year with unexpected gifts. Whether that leads to a late-year breakout or simply a stable base heading into 2026, you can always follow along and watch a holiday rally if one decides to show up.

Από τη δημιουργία του Bitcoin το 2009, ο όρος fiat νόμισμα έχει γίνει όλο και πιο διαδεδομένος. Αλλά τι ακριβώς σημαίνει; Στο άρθρο αυτό, θα δούμε την προέλευση του όρου, πώς λειτουργεί, ποια παραδείγματα fiat υπάρχουν και πώς τα κρυπτονομίσματα έχουν αμφισβητήσει τον ρόλο του.

Ο όρος "fiat" προέρχεται από τα λατινικά και σημαίνει περίπου "κατ’ εντολή", δηλαδή μια επίσημη απόφαση με ισχύ νόμου. Έτσι, fiat χρήμα είναι εκείνο που αναγνωρίζεται ως νόμιμο μέσο πληρωμής από το κράτος.

Εκδίδεται και διαχειρίζεται από την κυβέρνηση ή την κεντρική τράπεζα και χρησιμοποιείται στις καθημερινές συναλλαγές για αγαθά και υπηρεσίες.

Από το 2020, όλα τα νομίσματα που διαπραγματεύονται διεθνώς θεωρούνται fiat. Η αξία τους δεν βασίζεται πλέον σε φυσικά αγαθά, όπως ο χρυσός ή το ασήμι, αλλά στην εμπιστοσύνη και την αξιοπιστία του κράτους που τα εκδίδει.

Fiat νόμισμα ή fiat χρήμα;

Οι όροι fiat currency και fiat money αναφέρονται ουσιαστικά στο ίδιο πράγμα: στα κρατικά εκδιδόμενα νομίσματα που χρησιμοποιούνται σε κάθε χώρα.

Υπάρχουν περίπου 180 διαφορετικά fiat νομίσματα σε κυκλοφορία παγκοσμίως, όπως:

- Δολάριο ΗΠΑ

- Ευρώ

- Στερλίνα

- Γιεν Ιαπωνίας

- Δολάριο Καναδά

Η ισοτιμία μεταξύ δύο fiat νομισμάτων ονομάζεται συναλλαγματική ισοτιμία.

Fiat χρήμα vs νομίσματα βασισμένα σε εμπορεύματα

Το fiat χρήμα είναι το ακριβώς αντίθετο από ένα νόμισμα που έχει εγγενή αξία, όπως ένα νόμισμα από χρυσό ή ασήμι.

Ενώ ένα commodity money (νόμισμα εμπορεύματος) έχει αξία λόγω του υλικού από το οποίο είναι φτιαγμένο, το fiat δεν έχει εγγενή αξία — αποκτά αξία μόνο γιατί η κυβέρνηση το ορίζει ως μέσο ανταλλαγής.

Πώς δημιουργήθηκαν τα fiat νομίσματα;

Όλα τα νομίσματα ξεκίνησαν ουσιαστικά ως υποσχέσεις πληρωμής (IOUs). Αρχικά υπήρχε το σύστημα ανταλλαγής (barter).

Παράδειγμα ανταλλαγής:

Αν ένας αγρότης αντάλλασσε 2 κιλά αλεύρι σήμερα για 10 κολοκύθες το φθινόπωρο, θα λάμβανε ένα "χαρτί" που επιβεβαίωνε αυτή τη συμφωνία. Το χαρτί αυτό αποκτούσε αξία και μπορούσε να ανταλλαχθεί και για άλλα αγαθά.

Για να γίνει πιο πρακτικό, οι άνθρωποι άρχισαν να χρησιμοποιούν φυσικά εμπορεύματα, όπως ο χρυσός, ως ενιαίο μέσο ανταλλαγής.

Από τον χρυσό στα νομίσματα

Η ζύγιση του χρυσού δεν ήταν πρακτική, οπότε τα κράτη άρχισαν να κόβουν χρυσά νομίσματα με σταθερό βάρος και εγγυημένη ποσότητα χρυσού. Έβαζαν χαρακώσεις γύρω από την άκρη του νομίσματος για να διασφαλίσουν ότι δεν έχει «ξυστεί» χρυσός από αυτό.

Η εμφάνιση των τραπεζών

Ο χρυσός ήταν δύσκολο να κουβαληθεί και επικίνδυνος να διατηρηθεί, έτσι εμφανίστηκαν οι τράπεζες. Εκεί, οι άνθρωποι αποθήκευαν τον χρυσό τους και έπαιρναν αποδείξεις ιδιοκτησίας — τα πρώτα "χαρτονομίσματα".

Από το χρυσό στο χαρτονόμισμα

Με τον καιρό, οι πολίτες έπαψαν να ανταλλάσσουν τα χαρτονομίσματα με χρυσό, και απλώς τα χρησιμοποιούσαν για συναλλαγές. Κάπως έτσι γεννήθηκε το σύστημα του fiat.

Η τιμή του νομίσματος δεν βασιζόταν πια στον χρυσό, αλλά στην απόφαση του κράτους για την αξία του — «κατ’ εντολή» δηλαδή.

Το τέλος του κανόνα του χρυσού

Μέχρι το 1971, το δολάριο ΗΠΑ ήταν συνδεδεμένο με συγκεκριμένη ποσότητα χρυσού. Τότε ο Πρόεδρος Ρίτσαρντ Νίξον κατάργησε οριστικά το σύστημα αυτό (γνωστό ως “Nixon shock”).

Από τότε, τα νομίσματα απέκτησαν ελεύθερη κυμαινόμενη αξία βασισμένη στην εμπιστοσύνη της αγοράς και την νομισματική πολιτική κάθε χώρας.

Είναι ακόμα χρήσιμο το fiat χρήμα;

Με την εμφάνιση των κρυπτονομισμάτων, ο τρόπος που αντιλαμβανόμαστε το χρήμα έχει αλλάξει σημαντικά.

Παρόλο που χώρες όπως το Ελ Σαλβαδόρ έχουν αναγνωρίσει το Bitcoin ως νόμιμο μέσο πληρωμής, τα fiat νομίσματα παραμένουν ο βασικός πυλώνας της παγκόσμιας οικονομίας και δύσκολα θα αντικατασταθούν στο άμεσο μέλλον.

CBDCs: Ψηφιακή εξέλιξη του fiat

Μια πρόσφατη καινοτομία είναι τα CBDCs (Central Bank Digital Currencies), τα οποία συνδυάζουν τον κόσμο των fiat με την τεχνολογία blockchain.

Πρόκειται για ψηφιακά νομίσματα που εκδίδονται από κεντρικές τράπεζες, λειτουργούν με τεχνολογία blockchain, είναι σταθερά σε αξία (όπως το ευρώ ή το δολάριο), και δεν παρουσιάζουν μεταβλητότητα όπως τα περισσότερα κρυπτονομίσματα.

Συμπέρασμα

Το fiat χρήμα παραμένει η ραχοκοκαλιά του παγκόσμιου χρηματοοικονομικού συστήματος. Παρά την άνοδο των ψηφιακών νομισμάτων, το fiat εξακολουθεί να παίζει καθοριστικό ρόλο στο παγκόσμιο εμπόριο, τη χρηματοδότηση και την καθημερινή οικονομική δραστηριότητα.

Η έννοια του χρήματος έχει αλλάξει ριζικά μέσα σε έναν αιώνα — και δεν αποκλείεται να δούμε ακόμα πιο δραστικές εξελίξεις στο μέλλον.

Ένα asset, ή αλλιώς περιουσιακό στοιχείο, μπορεί να οριστεί ως ένας πόρος ή αντικείμενο που προσφέρει μελλοντικά οικονομικά οφέλη στον ιδιώτη, την επιχείρηση ή το κράτος που το κατέχει.

Αν και τα περιουσιακά στοιχεία έχουν μακρά ιστορία στους ισολογισμούς των εταιρειών, σήμερα αποκτούν ευρύτερη έννοια, ειδικά στον σύγχρονο χρηματοοικονομικό κόσμο. Από χρηματοοικονομικά assets έως εκείνα που παρέχουν μακροπρόθεσμη οικονομική αξία, εδώ συγκεντρώσαμε όλα όσα χρειάζεται να γνωρίζετε για τα περιουσιακά στοιχεία.

Τι σημαίνει ο όρος "asset";

Το asset αναφέρεται σε έναν πόρο ή αντικείμενο που έχει οικονομική αξία, και από το οποίο ο κάτοχος — είτε πρόκειται για ιδιώτη, επιχείρηση ή κράτος — μπορεί να αναμένει μελλοντικά οικονομικά οφέλη.

Τα assets μπορούν να διατηρηθούν για να προσφέρουν ρευστότητα ή να πωληθούν με σκοπό το κέρδος. Συνήθως αποτιμώνται σε νομισματική αξία, ώστε να μπορεί να αξιολογηθεί η ρευστότητά τους ή το ενδεχόμενο κέρδος από τη μεταπώλησή τους.

Περιουσιακά στοιχεία που ανήκουν σε ιδιώτη αποκαλούνται προσωπικά assets, ενώ αυτά που ανήκουν σε επιχειρήσεις ονομάζονται επιχειρηματικά assets.

Τα assets χρησιμοποιούνται για την ενίσχυση της καθαρής θέσης, την αύξηση της αξίας μιας επιχείρησης και όχι μόνο. Μπορούν να είναι υλικά ή άυλα, όπως ο χρυσός ή τα κρυπτονομίσματα.

Ιδιώτες και εταιρείες χρησιμοποιούν assets για να αποδείξουν τη χρηματοοικονομική τους υγεία και σταθερότητα. Μπορούν να αξιοποιηθούν ως εγγύηση για δάνεια ή να πωληθούν για ρευστότητα.

Η επιτυχία μιας επιχείρησης συχνά υπολογίζεται αφαιρώντας τις υποχρεώσεις από τη συνολική αξία των assets της. Ένα asset θεωρείται πόρος που μπορεί στο μέλλον να αποφέρει έσοδα, είτε πρόκειται για εξοπλισμό παραγωγής είτε για μια πατέντα.

Τα assets κατηγοριοποιούνται σε: κυκλοφορούντα, πάγια, ενσώματα και άυλα, λειτουργικά και μη λειτουργικά.

Πώς λειτουργούν τα assets;

Ιδιώτες, επιχειρήσεις και κυβερνήσεις συγκεντρώνουν assets με την ελπίδα ότι θα τους αποφέρουν βραχυπρόθεσμα ή μακροπρόθεσμα οικονομικά οφέλη.

Βέβαια, αυτό δεν είναι εγγυημένο, αφού η αξία ενός asset μπορεί είτε να αυξηθεί είτε να μειωθεί, με το πραγματικό όφελος να πραγματοποιείται μόνο κατά την πώληση. Αυτή η μεταβλητότητα μπορεί να επηρεάσει την αξία του asset και, κατ’ επέκταση, τη συνολική οικονομική σταθερότητα του κατόχου.

Η φερεγγυότητα δείχνει κατά πόσο τα assets είναι επαρκή για την κάλυψη των υποχρεώσεων. Οι εταιρείες χρησιμοποιούν τον ισολογισμό τους για να αξιολογήσουν τη σχέση μεταξύ assets, υποχρεώσεων και καθαρής θέσης.

Πριν εξερευνήσουμε περισσότερο τον κόσμο των assets, ας δούμε τους βασικότερους τύπους.

Τύποι assets

Υπάρχουν 6 βασικές κατηγορίες περιουσιακών στοιχείων. Λόγω της ευρείας έννοιάς τους, ένα asset μπορεί να ανήκει σε περισσότερες από μία κατηγορίες. Ας τις δούμε αναλυτικά.

Κυκλοφορούντα assets (επιχειρηματικά assets)

Τα κυκλοφορούντα assets μπορούν εύκολα να μετατραπούν σε μετρητά, δηλαδή είναι άμεσα ρευστοποιήσιμα, και χρησιμοποιούνται για την κάλυψη υποχρεώσεων. Παραδείγματα περιλαμβάνουν: μετρητά και ισοδύναμα μετρητών, απαιτήσεις από πελάτες, αποθέματα και προπληρωμένες δαπάνες.

Πάγια assets

Γνωστά και ως μη κυκλοφορούντα assets, αποκτώνται για μακροπρόθεσμη χρήση, συνήθως άνω των 12 μηνών, και δεν είναι εύκολο να ρευστοποιηθούν άμεσα. Παραδείγματα είναι η γη, τα κτίρια και ο εξοπλισμός.

Ενσώματα assets

Πρόκειται για assets που μπορούμε να δούμε και να αγγίξουμε, δηλαδή φυσικά αγαθά. Παραδείγματα είναι τα μετρητά, το απόθεμα, τα κτίρια, οι μετοχές, τα μηχανήματα και τα έπιπλα.

Άυλα assets

Αντίθετα, τα άυλα assets δεν έχουν φυσική υπόσταση. Παραδείγματα είναι: η πνευματική ιδιοκτησία, οι πατέντες, τα κρυπτονομίσματα, οι άδειες, οι επιχορηγήσεις και οι μυστικές φόρμουλες.

Λειτουργικά assets

Τα λειτουργικά assets ανήκουν σε μια επιχείρηση και χρησιμοποιούνται στις καθημερινές της δραστηριότητες ή για την παραγωγή εσόδων. Παραδείγματα: αποθέματα, πατέντες, εξοπλισμός, άδειες και μυστικές φόρμουλες.

Μη λειτουργικά assets

Αυτά δεν χρησιμοποιούνται απαραίτητα για τις καθημερινές λειτουργίες της επιχείρησης, αλλά ενδέχεται να αποφέρουν κέρδη στο μέλλον. Παραδείγματα: αδόμητη γη, εμπορεύσιμα αξιόγραφα, βραχυπρόθεσμες και μακροπρόθεσμες επενδύσεις.

Ο ορισμός του asset

Όπως έχουμε ήδη δει, ο ορισμός του asset είναι ευρύς και, ακόμη και αν το κατατάξουμε σε κατηγορίες, δεν αποτυπώνει πάντα πλήρως τις δυνατότητές του.

Για παράδειγμα, μια πατέντα μπορεί να θεωρείται άυλο asset, αποθηκευμένη ψηφιακά, αλλά για κάποιες επιχειρήσεις αποτελεί βασικό λειτουργικό asset.

Ή το Bitcoin: αν και άυλο και ψηφιακά αποθηκευμένο, μπορεί επίσης να θεωρηθεί ως κυκλοφορούν asset ή ακόμη και ως ρευστό.

Το απόθεμα είναι ένα τυπικό παράδειγμα κυκλοφορούντος, ενσώματου και λειτουργικού asset ταυτόχρονα.

Αυτό αποδεικνύει ότι δεν υπάρχει αυστηρός ορισμός για το τι είναι asset, καθώς εξαρτάται σε μεγάλο βαθμό από τον τρόπο που θα επιλέξει να το αξιοποιήσει ο κάτοχος.

Ωστόσο, είναι καλό να θυμόμαστε:

- Τα ενσώματα assets δεν μπορούν να είναι άυλα.

- Τα κυκλοφορούντα assets δεν μπορούν να θεωρηθούν πάγια.

- Τα λειτουργικά assets δεν είναι μη λειτουργικά.

Υπάρχουν εξαιρέσεις, αλλά γενικά αυτές είναι οι βασικές αρχές.

Assets vs υποχρεώσεις

Είτε υπολογίζετε την καθαρή αξία ενός επιχειρηματία είτε την αξία μιας εταιρείας, οι υποχρεώσεις παίζουν καθοριστικό ρόλο στη φερεγγυότητα.

Αφαιρώντας τις υποχρεώσεις από τα assets, προκύπτει το Fund Balance, γνωστό και ως Καθαρή Θέση ή Ιδιοκτησία.

Για να το υπολογίσετε, χρειάζεται να αναλύσετε τον ισολογισμό της εταιρείας. Αν η εταιρεία είναι δημόσια, είναι υποχρεωμένη να δημοσιεύει τον ισολογισμό της στις ετήσιες εκθέσεις της.

Απλοποιημένα: Assets - Υποχρεώσεις = Καθαρή Θέση

Κατανόηση των assets και της οικονομικής τους αξίας

Η έννοια των assets είναι απεριόριστη — ακόμη και το κολιέ από ζαφείρι που κληρονομήσατε μπορεί να θεωρηθεί ως κυκλοφορούν και ενσώματο asset.

Η αξία του μπορεί να αξιοποιηθεί άμεσα ή να περιμένετε μια περίοδο έλλειψης ζαφειριών για ακόμα μεγαλύτερη αξία.

Η διαχείριση των assets διαφέρει μεταξύ προσωπικής και επαγγελματικής ζωής, αλλά ελπίζουμε ότι αυτό το άρθρο σάς βοήθησε να κατανοήσετε καλύτερα τις ομοιότητες και τις διαφορές.

Σε κάθε περίπτωση, το asset είναι ένας πόρος από τον οποίο άτομα, επιχειρήσεις ή κυβερνήσεις μπορούν να περιμένουν μελλοντική ροή εσόδων.

Είτε πρόκειται για πάγιο είτε για κυκλοφορούν asset, ο στόχος είναι πάντα η αξιοποίησή του για οικονομικό όφελος. Χρυσός, Bitcoin, ακίνητα, αυτοκίνητα, μυστικές φόρμουλες και πατέντες — όλα μπορούν να θεωρηθούν assets, καθώς έχουν την προοπτική να δημιουργήσουν αξία.

Τώρα που γνωρίζετε περισσότερα για τα assets και τη σημασία τους, κάντε τη δική σας έρευνα και ανακαλύψτε ποιο asset ταιριάζει στις ανάγκες και τις φιλοδοξίες σας.