Learning the friendly way

Dive into our resources, guides, and articles for all things money-related. Grow your financial confidence with our experts curated tips and articles for both experienced and new investors.

LATEST ARTICLEs

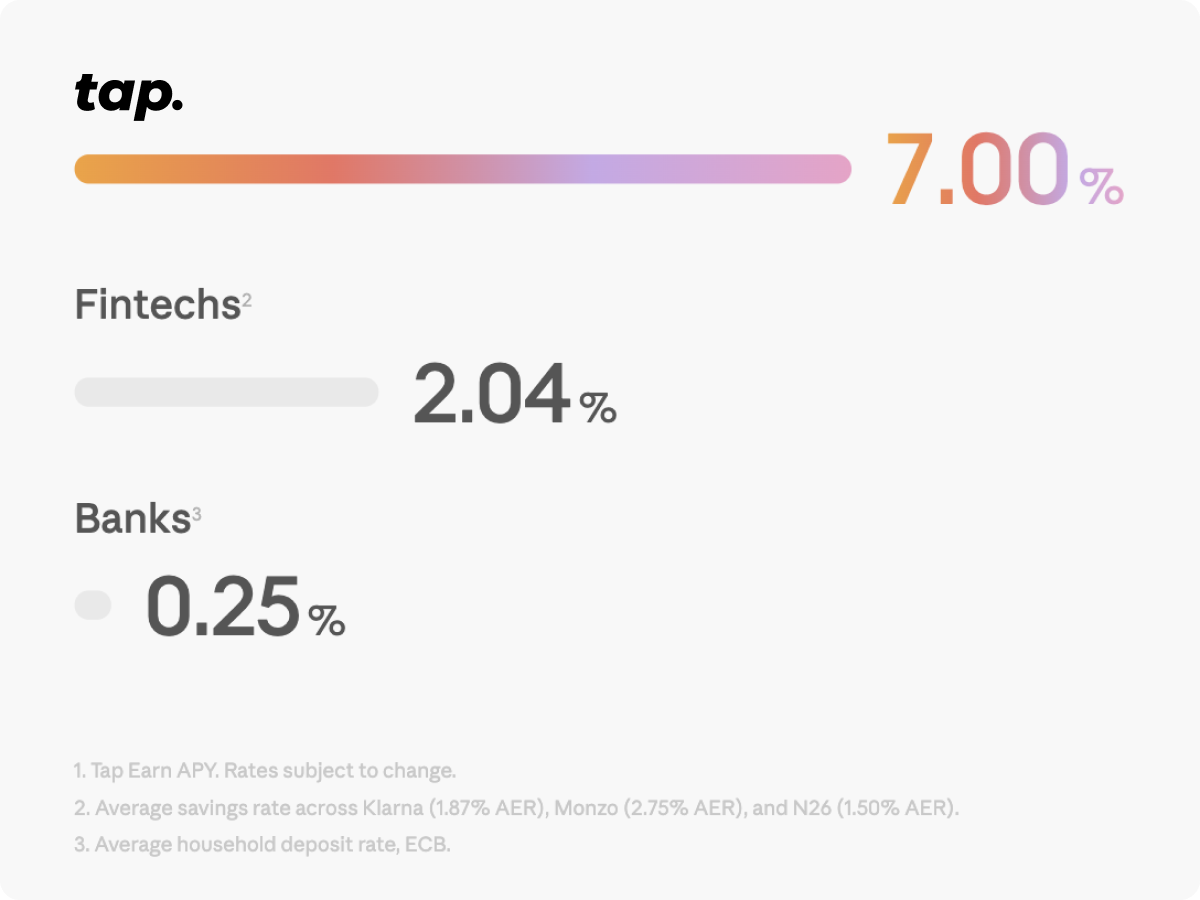

Savings accounts haven't changed in decades, but the cost of everything else has. Rent's up. Groceries cost more. A coffee costs what lunch used to. And your savings account? Still paying you next to nothing while the bank lends your money out and keeps the difference.

Most savings accounts pay around 0.4% APY. That's $4 a year on $1,000.Even the fintech "high-yield" ones barely push past 3%, and they still come with the usual catches, fine prints, and withdrawal limits.

Meanwhile, the official inflation rate keeps running higher. When inflation runs higher than your interest rate, you're losing purchasing power every year. Your savings shrink, even if the number in your account slowly ticks up.

It should be easier to save for your holidays, that nicer car, or your dream house down payment. That's why we built Tap Earn.

A Better Way to Earn

Tap Earn offers up to 7% APY, that's nearly 18x what most banks pay and double what fintechs offer out there.

Your interest compounds daily and pays out every week, straight into your balance. No waiting for end-of-month statements, no quarterly or year cycles, no lockup. Every Monday, your balance is higher than it was on Friday. Not a bad way to start the week.

And unlike your bank, you don't have to guess what you've earned. Open the app anytime and see exactly how much interest you've made, down to the cent.

What Can You Earn On?

Tap Earn launches with USDT, USDC, BTC, ETH, XRP, and SOL. More of your favorite assets are on the way.

We're not trying to list everything under the sun. Every asset we add has to meet one standard: can we offer a rate worth your time? If we can't give you a good rate on it, we won't add it just to pad a menu. Quality over quantity. Your earnings come first.

Deposit From Anywhere

Accessibility matters most to us, earning should be easy no matter how you deposit. With Tap, you can deposit money anytime, anywhere, using whatever method you like best. Tap supports bank transfers and debit cards, from majors to stablecoins to the long tail most platforms don't bother supporting. You don't need to move your life around to start earning. Link your existing bank account in minutes and start earning higher rates on your savings without switching banks or opening new accounts here and there.

Your money is yours, and you should be able to access it when you need it. You can withdraw with no penalties, take out what you want, when you want.

Time to Start Earning

Tap is trusted by 400,000+ users across 40+ countries and is publicly listed on the London Stock Exchange. This isn't a startup in someone's garage.

Ready to get started? Download the app, or head to the app and simply find the "Earn" tab from the hub.

It's time to earn what you deserve.

See you inside.

Tap Earn services are provided by Tap Earn Inc and are not regulated by the Gibraltar Financial Services Commission or by the UK Financial Conduct Authority, or covered by the Gibraltar Investor Compensation Scheme or the UK Financial Services Compensation Scheme.

Τι είναι το Chainlink;

Το Chainlink είναι ένα αποκεντρωμένο δίκτυο oracle που επιτρέπει στα smart contracts να συνδεθούν με δεδομένα του πραγματικού κόσμου. Από τιμές fiat νομισμάτων και καιρικές προβλέψεις, μέχρι APIs και τραπεζικές πληρωμές, το Chainlink προσφέρει έναν ασφαλή τρόπο για να «μιλάνε» τα blockchain με τον έξω κόσμο.

Αυτό λύνει ένα βασικό πρόβλημα των smart contracts: χωρίς πρόσβαση σε εξωτερικά δεδομένα, πολλά από αυτά δεν μπορούν να λειτουργήσουν όπως πρέπει.

Πώς λειτουργεί το Chainlink;

Το Chainlink συνδέει smart contracts με εξωτερικά δεδομένα μέσω ενός αποκεντρωμένου δικτύου από oracles.

Αναλυτικά η διαδικασία περιλαμβάνει 3 βασικά στάδια:

1. Επιλογή Oracle

Ο χρήστης δημιουργεί μια συμφωνία παροχής υπηρεσιών (SLA) όπου ορίζει τα δεδομένα που χρειάζεται. Το δίκτυο στη συνέχεια επιλέγει τους κατάλληλους oracles και ο χρήστης καταθέτει το απαιτούμενο ποσό σε LINK tokens.

2. Αναφορά Δεδομένων

Οι oracles συλλέγουν τα δεδομένα από τις εξωτερικές πηγές και τα στέλνουν πίσω στο smart contract μέσω του Chainlink.

3. Συγκέντρωση Αποτελεσμάτων

Τα αποτελέσματα συγκρίνονται σε ένα aggregation contract για να ελεγχθεί η αξιοπιστία και η ακρίβεια. Όσο πιο ακριβής και συνεπής είναι ένας oracle, τόσο υψηλότερο reputation score αποκτά.

Ποιος δημιούργησε το Chainlink;

Το Chainlink ιδρύθηκε το 2017 από τους Sergey Nazarov και Steve Ellis, οι οποίοι είχαν προηγουμένως αναπτύξει το SmartContract.com.

Η ιδέα ξεκίνησε ως ένας τρόπος να «ζωντανέψουν» τα smart contracts δίνοντάς τους πρόσβαση σε τραπεζικά συστήματα και εξωτερικά δεδομένα. Το whitepaper δημοσιεύτηκε το 2017 και η πρώτη πώληση LINK tokens μέσω ICO συγκέντρωσε $32 εκατομμύρια.

Γιατί Chainlink και όχι κάποιο άλλο oracle;

Το Chainlink είναι αποκεντρωμένο, πράγμα που σημαίνει ότι δεν εξαρτάται από έναν μόνο πάροχο δεδομένων. Αντίθετα, τα δεδομένα προέρχονται από πολλαπλούς oracles, διασταυρώνονται και επαληθεύονται πριν χρησιμοποιηθούν από το smart contract.

Επιπλέον, το Chainlink:

- Λειτουργεί σε Proof-of-Stake σύστημα.

- Προσφέρει διαφάνεια και επαλήθευση μέσω reputation scoring.

- Μπορεί να συνδεθεί με οποιαδήποτε blockchain και οποιοδήποτε API.

Τι είναι το LINK;

Το LINK είναι το native token του Chainlink και έχει τρεις κύριες χρήσεις:

- Πληρωμή των oracles για την παροχή δεδομένων

- Κίνητρο για συνεπή και αξιόπιστη λειτουργία των node operators

- Staking για συμμετοχή στο δίκτυο και διασφάλιση της αξιοπιστίας

Οι node operators ποντάρουν LINK tokens ως εγγύηση για τις υπηρεσίες τους, ενώ οι χρήστες πληρώνουν σε LINK για να αποκτήσουν τα δεδομένα που χρειάζονται.

Πώς με ωφελεί το Chainlink;

Το Chainlink είναι ιδανικό για όποιον θέλει να φέρει τα έξυπνα συμβόλαια πιο κοντά στην πραγματικότητα.

Αν είσαι developer, μπορείς να χρησιμοποιήσεις το Chainlink για:

- Τιμές συναλλάγματος

- Καιρικές συνθήκες

- Αποτελέσματα αγώνων

- Σύνδεση με τραπεζικά APIs και πολλά άλλα

Επιτρέπει στις εφαρμογές σου να λειτουργούν με αληθινά δεδομένα με ασφαλή και αποκεντρωμένο τρόπο.

Πώς μπορώ να αγοράσω LINK;

Μπορείς να αγοράσεις LINK απευθείας μέσα από την εφαρμογή Tap.

- Κάνε σύνδεση ή δημιουργία λογαριασμού

- Επίλεξε LINK στο ανταλλακτήριο

- Αγόρασέ το με κάρτα Visa / Mastercard ή μέσω άλλου crypto

Το LINK θα αποθηκευτεί αυτόματα στο ασφαλές crypto πορτοφόλι σου μέσα στην εφαρμογή.

Συμπερασματικά

Το Chainlink γεφυρώνει το χάσμα μεταξύ blockchain και του πραγματικού κόσμου. Με ένα ισχυρό αποκεντρωμένο σύστημα oracles και το utility token LINK, προσφέρει ασφαλή, διαφανή και αξιόπιστη πρόσβαση σε εξωτερικά δεδομένα για κάθε είδους smart contracts.

Είτε χτίζεις εφαρμογές, είτε επενδύεις σε κρυπτονομίσματα, το Chainlink είναι σίγουρα ένα project που αξίζει την προσοχή σου.

Το Livepeer είναι ένα αποκεντρωμένο δίκτυο για μετάδοση βίντεο, σχεδιασμένο για να κάνει το video streaming πιο προσιτό και οικονομικό για όλους. Ξεκίνησε το 2017 και αποτελεί το πρώτο πλήρως αποκεντρωμένο πρωτόκολλο ζωντανής μετάδοσης, προσφέροντας μια εναλλακτική στις παραδοσιακές υπηρεσίες όπως το YouTube ή το Twitch.

Η πλατφόρμα συνδέει δημιουργούς περιεχομένου που χρειάζονται επεξεργασία των βίντεό τους με υπολογιστές που προσφέρουν την απαραίτητη υπολογιστική ισχύ. Αυτή η peer-to-peer προσέγγιση μπορεί να μειώσει το κόστος μετάδοσης έως και 50–90% σε σύγκριση με τους κλασικούς παρόχους cloud, χωρίς συμβιβασμούς στην ποιότητα ή την αξιοπιστία.

TLDR

Αποκεντρωμένη υποδομή για βίντεο: Το Livepeer προσφέρει απεριόριστη υπολογιστική ισχύ για βίντεο, ιδανική για AI εφαρμογές και επεξεργασία βίντεο.

Χαμηλότερο κόστος μετάδοσης: Δημιουργεί μια αγορά όπου προγραμματιστές μπορούν να ενσωματώσουν υπηρεσίες βίντεο και transcoding με χαμηλότερο κόστος.

Χτισμένο στο Ethereum: Προσφέρει μια λύση πάνω στο blockchain που δίνει περισσότερη ελευθερία σε προγραμματιστές και ανεξαρτησία στους δημιουργούς περιεχομένου.

Token δικτύου (LPT): Το Livepeer Token χρησιμοποιείται για staking και διακυβέρνηση του δικτύου, όχι για άμεσες πληρωμές.

Τι κάνει το Livepeer;

Το Livepeer δημιουργεί ένα παγκόσμιο δίκτυο όπου οποιοσδήποτε μπορεί να προσφέρει υπολογιστική ισχύ για την επεξεργασία βίντεο. Αντί για ακριβούς κεντρικούς servers, τα βίντεο μετατρέπονται και διανέμονται μέσω ενός αποκεντρωμένου δικτύου υπολογιστών.

Η επεξεργασία γίνεται μέσω του transcoding, δηλαδή της μετατροπής των βίντεο σε διαφορετικά format και ποιότητες για να προβάλλονται άνετα σε διάφορες συσκευές και συνδέσεις. Παραδοσιακά, αυτή η διαδικασία απαιτεί τεράστιες υποδομές. Το Livepeer, όμως, το πετυχαίνει με ένα αποκεντρωμένο δίκτυο.

Οι δημιουργοί εξοικονομούν κόστος, οι "orchestrators" κερδίζουν ανταμοιβές για τη συμμετοχή τους, και οι χρήστες απολαμβάνουν ποιοτική προβολή. Το δίκτυο είναι ιδιαίτερα χρήσιμο για developers που φτιάχνουν video εφαρμογές και θέλουν έτοιμη υποδομή χωρίς τεράστια κόστη.

Ποιοι ίδρυσαν το Livepeer;

Το Livepeer ιδρύθηκε το 2017 από τους Doug Petkanics και Eric Tang, έμπειρους προγραμματιστές με κοινή πορεία στον χώρο της τεχνολογίας. Ο Petkanics είναι CEO με φόντο στο software development και ο Tang είναι CTO με στόχο τη χρήση του blockchain για αποδοτικότερο streaming.

Από την ίδρυσή του, το δίκτυο έχει εξελιχθεί εντυπωσιακά και πλέον χρησιμοποιεί περισσότερες από 70.000 μονάδες GPU για επεξεργασία βίντεο.

Πώς λειτουργεί το Livepeer;

Δίκτυο επεξεργασίας βίντεο (transcoding)

Ο πυρήνας του Livepeer είναι η μετατροπή των βίντεο σε πολλά formats (1080p, 720p, 480p). Η εργασία αυτή δεν γίνεται σε κέντρα δεδομένων αλλά διανέμεται σε χιλιάδες υπολογιστές ανά τον κόσμο που ανταγωνίζονται στην ποιότητα και το κόστος.

Ασφάλεια και staking

Όσοι θέλουν να συμμετέχουν ως "orchestrators" πρέπει να κάνουν stake tokens LPT ως εγγύηση καλής λειτουργίας. Οι χρήστες μπορούν επίσης να αναθέσουν τα LPT τους σε αξιόπιστους orchestrators και να κερδίζουν μέρος των ανταμοιβών.

Οικονομικά κίνητρα

Η αγορά του Livepeer λειτουργεί με βάση τον ανταγωνισμό. Οι δουλειές δίνονται στους orchestrators που προσφέρουν το καλύτερο αποτέλεσμα στην καλύτερη τιμή. Οι πληρωμές γίνονται κυρίως σε ETH, ενώ το LPT χρησιμοποιείται για staking και διακυβέρνηση.

Τι είναι το LPT;

Το LPT είναι το native token του Livepeer και έχει ρόλο εργασίας και ασφάλειας στο δίκτυο. Συγκεκριμένα προσφέρει:

- Ασφάλεια δικτύου: Απαιτείται staking για συμμετοχή ως orchestrator.

- Διακυβέρνηση: Οι κάτοχοι LPT μπορούν να ψηφίζουν σε προτάσεις του δικτύου.

- Ανταμοιβές με ανάθεση: Οι χρήστες μπορούν να αναθέσουν τα tokens τους και να λαμβάνουν ποσοστά από τις αμοιβές.

- Δικαίωμα συμμετοχής: Το LPT συμβολίζει το δικαίωμα παροχής υπηρεσιών επεξεργασίας στο δίκτυο.

Το token ακολουθεί μοντέλο πληθωρισμού, με νέα LPT να εκδίδονται για να επιβραβεύουν τους συμμετέχοντες.

Πώς μπορώ να αγοράσω ή να πουλήσω LPT;

Μπορείτε να αγοράσετε, να πουλήσετε και να αποθηκεύσετε LPT tokens απευθείας από την εφαρμογή Tap. Αφού ολοκληρώσετε την επαλήθευση λογαριασμού, μπορείτε εύκολα να διαχειριστείτε τα LPT σας μαζί με άλλα κρυπτονομίσματα.

Πριν εξερευνήσετε περαιτέρω το LPT, καλό είναι να γνωρίζετε ότι η αξία του token σχετίζεται άμεσα με τη χρήση του δικτύου. Όσο περισσότεροι developers και δημιουργοί περιεχομένου χρησιμοποιούν την υποδομή του Livepeer, τόσο αυξάνεται και η ζήτηση για staking και το οικοσύστημα συνολικά.

Το Ripple είναι μια από τις πιο συζητημένες και αναγνωρίσιμες επιλογές για όσους θέλουν να διαφοροποιήσουν το χαρτοφυλάκιό τους σε crypto. Ανάμεσα σε επαίνους αλλά και αντιπαραθέσεις, το Ripple χαράζει τον δικό του δρόμο στον κόσμο των κρυπτονομισμάτων.

Ας δούμε τι είναι το Ripple (XRP) και γιατί τραβά τόσο συχνά τα φώτα της δημοσιότητας.

Τι είναι το Ripple (XRP);

Για να κατανοήσουμε τι είναι το Ripple, πρέπει πρώτα να γνωρίσουμε τα τρία βασικά του στοιχεία:

- Ripple Labs είναι η εταιρεία που διαχειρίζεται τα διάφορα προϊόντα της πλατφόρμας.

- RippleNet είναι το δίκτυο που διευκολύνει τις παγκόσμιες πληρωμές μεταξύ χρηματοπιστωτικών ιδρυμάτων, βασισμένο στο XRP Ledger.

- XRP είναι το κρυπτονόμισμα που υποστηρίζει το δίκτυο, προσφέροντας ταχύτερες και οικονομικότερες συναλλαγές.

Με απλά λόγια, το Ripple είναι μια ψηφιακή πλατφόρμα πληρωμών που έχει σχεδιαστεί για την ταχύτερη και φθηνότερη διεκπεραίωση διεθνών συναλλαγών, συστημάτων μεταφοράς χρημάτων και ανταλλαγής περιουσιακών στοιχείων. Η εταιρεία έχει αναπτύξει διάφορα προϊόντα για χρηματοπιστωτικά ιδρύματα, χτίζοντας έτσι μια γέφυρα μεταξύ της παραδοσιακής χρηματοοικονομικής αγοράς και της τεχνολογίας blockchain.

Αντί για κλασική blockchain τεχνολογία, το Ripple χρησιμοποιεί τη δική του, ιδιόκτητη κατανεμημένη τεχνολογία λογιστικής. Έχει σχεδιαστεί για να προσφέρει μια εναλλακτική λύση στο παραδοσιακό σύστημα πληρωμών, όπως το SWIFT, απευθυνόμενο σε διεθνείς και διασυνοριακές συναλλαγές.

Τι είναι το XRP;

Το XRP κυκλοφόρησε το 2013 με συνολική ποσότητα 100 δισεκατομμυρίων token, από τα οποία περίπου 52 δισεκατομμύρια βρίσκονται αυτή τη στιγμή σε κυκλοφορία. Τα coins παραμένουν υπό τη διαχείριση της εταιρείας και απελευθερώνονται σταδιακά στην αγορά μέσω διαφορετικών μηχανισμών από το mining.

Αν και το XRP είναι το εγγενές νόμισμα του XRP Ledger, η τεχνολογία του ledger μπορεί να διαχειρίζεται συναλλαγές σε πολλά νομίσματα. Το XRP χρησιμοποιείται κυρίως για γρήγορη μετατροπή μεταξύ διαφορετικών νομισμάτων.

Η ιστορία του XRP

Το Ripple ξεκίνησε ως ιδέα το 2004 από τον Ryan Fugger στο Βανκούβερ, ως μια διαδικτυακή πλατφόρμα πληρωμών. Με την εμφάνιση των κρυπτονομισμάτων, δύο προγραμματιστές πρότειναν στον Fugger να συνδυάσουν τις ιδέες τους και να δημιουργήσουν το δικό τους ψηφιακό νόμισμα.

Έτσι, το 2012 ιδρύθηκε η OpenCoin από τους Chris Larsen και Jed McCaleb, με τον Fugger να συμμετέχει στην ομάδα. Τον Σεπτέμβριο του 2013, η OpenCoin μετονομάστηκε σε Ripple Labs και αργότερα, το 2015, απλά σε Ripple.

Το 2016, η εταιρεία έλαβε μία από τις τέσσερις άδειες BitLicense που απαιτούνται από την Πολιτεία της Νέας Υόρκης για την παροχή υπηρεσιών με ψηφιακά νομίσματα.

Πώς λειτουργεί το Ripple;

Το Ripple χρησιμοποιεί έναν διαφορετικό και πιο σύνθετο μηχανισμό για τη διατήρηση του δικτύου του, σε σύγκριση με άλλα crypto όπως το Bitcoin ή το Ethereum. Το ledger του RippleNet διατηρείται από την κοινότητα του XRP και μπορεί να διεκπεραιώνει συναλλαγές κάθε 3-5 δευτερόλεπτα.

Το δίκτυο αποτελείται από ανεξάρτητα validator nodes, που επικυρώνουν τις συναλλαγές μέσω ενός μηχανισμού συναίνεσης. Αυτά τα nodes περιλαμβάνουν χρηματοπιστωτικά ιδρύματα, πανεπιστήμια και εταιρείες εκτός του blockchain χώρου.

Το σύστημα πληρωμών του Ripple έχει ήδη ενσωματωθεί σε τραπεζικά συστήματα για τον εκσυγχρονισμό των παραδοσιακών διαδικασιών. Για παράδειγμα, η τεχνολογία xCurrent του Ripple χρησιμοποιήθηκε στην εφαρμογή One Pay FX της ισπανικής τράπεζας Santander, διευκολύνοντας διεθνείς πληρωμές. Αντίστοιχα, η εφαρμογή MoneyTap στην Ιαπωνία συνδέει 61 τράπεζες για εγχώριες πληρωμές μέσω κινητού τηλεφώνου.

Τα προϊόντα του Ripple συνεχίζουν να υιοθετούνται παγκοσμίως.

Ripple και SEC

Το 2020 ξέσπασε μία από τις μεγαλύτερες νομικές μάχες στον χώρο των crypto, όταν η Επιτροπή Κεφαλαιαγοράς των ΗΠΑ (SEC) μήνυσε το Ripple και δύο στελέχη του, υποστηρίζοντας ότι παραβίασαν τους νόμους περί προστασίας των επενδυτών.

Η SEC απαγόρευσε άμεσα τη διαπραγμάτευση του XRP σε όλες τις αμερικανικές πλατφόρμες, δίνοντας το έναυσμα για μια πολύκροτη δικαστική υπόθεση.

Το βασικό ερώτημα της υπόθεσης ήταν αν το XRP πρέπει να θεωρείται αξιόγραφο, με την SEC να ισχυρίζεται ότι η εταιρεία συγκέντρωσε παράνομα 1,3 δισεκατομμύρια δολάρια μέσω μη εγγεγραμμένης προσφοράς αξιόγραφων.

Η υπόθεση είναι ιδιαίτερα σημαντική, καθώς το αποτέλεσμά της θα μπορούσε να επηρεάσει τη ρύθμιση και άλλων κρυπτονομισμάτων. Αν το XRP κριθεί αξιόγραφο, θα μπορούσαν να ακολουθήσουν νέοι κανονισμοί και για άλλα ψηφιακά περιουσιακά στοιχεία.

Σε πρόσφατη απόφαση, η δικαστής Analisa Torres δήλωσε ότι το XRP "δεν αποτελεί απαραίτητα αξιόγραφο εκ φύσεως", διαψεύδοντας εν μέρει τους ισχυρισμούς της SEC, και έκρινε ότι η εταιρεία δεν παραβίασε τους ομοσπονδιακούς νόμους περί αξιόγραφων όταν διέθετε το XRP σε δημόσιες πλατφόρμες.

Ωστόσο, η SEC σημείωσε μια μερική επιτυχία, αφού η δικαστής αποφάνθηκε ότι ορισμένες πωλήσεις token σε θεσμικούς επενδυτές πληρούν τα κριτήρια για συναλλαγές αξιόγραφων.

Ο CEO της Ripple, Brad Garlinghouse, χαρακτήρισε την απόφαση "τεράστια νίκη όχι μόνο για τη Ripple, αλλά και για ολόκληρη τη βιομηχανία στις ΗΠΑ."

Ripple vs Bitcoin

Όταν συγκρίνουμε το XRP με το Bitcoin, είναι σημαντικό να κατανοήσουμε τις διαφορετικές τους χρήσεις.

Το Bitcoin σχεδιάστηκε για να παρέχει ένα ψηφιακό σύστημα peer-to-peer πληρωμών και αποθήκευσης αξίας, ενώ το XRP δημιουργήθηκε για τη διευκόλυνση των διεθνών συναλλαγών, προσφέροντας μια ταχύτερη και οικονομικότερη εναλλακτική στις παραδοσιακές συναλλαγές fiat.

Επιπλέον, το Bitcoin βασίζεται στο mining μέσω του μηχανισμού Proof-of-Work, ενώ το Ripple χρησιμοποιεί ένα δίκτυο validators εκτός του crypto οικοσυστήματος. Το σύστημα συναίνεσής του επιτρέπει ταχύτερη επιβεβαίωση συναλλαγών και είναι ενεργειακά αποδοτικότερο.

Πώς να αγοράσετε XRP

Αν σας ενδιαφέρει να προσθέσετε το XRP στο crypto χαρτοφυλάκιό σας, μπορείτε εύκολα και με ασφάλεια μέσω της εφαρμογής Tap. Μέσα από την εφαρμογή, το XRP είναι διαθέσιμο για αγορά, πώληση, ανταλλαγή και αποθήκευση, όλα σε ένα ασφαλές και εύχρηστο περιβάλλον.

Το IBAN (International Bank Account Number) δημιουργήθηκε αρχικά από την Ευρωπαϊκή Κεντρική Τράπεζα για να διευκολύνει τις διεθνείς μεταφορές χρημάτων. Σήμερα, το IBAN χρησιμοποιείται ευρέως σε πολλές χώρες και αποτελεί βασικό κομμάτι του σύγχρονου τραπεζικού συστήματος.

Σε αυτό το άρθρο θα δούμε τι είναι το IBAN, πώς μοιάζει, πώς διαφέρει από τον κωδικό SWIFT, και πώς μπορείτε να βρείτε τον δικό σας αριθμό.

Τι είναι το IBAN;

Το IBAN είναι ένας διεθνής αριθμός τραπεζικού λογαριασμού, μοναδικός για κάθε λογαριασμό, που έχει σχεδιαστεί για να διευκολύνει και να βελτιστοποιεί τις διεθνείς μεταφορές χρημάτων.

Ουσιαστικά λειτουργεί σαν ένα σύστημα επαλήθευσης, διασφαλίζοντας ότι τα στοιχεία του λογαριασμού είναι σωστά πριν ολοκληρωθεί μια διασυνοριακή συναλλαγή.

Αρχικά χρησιμοποιήθηκε εντός της Ευρωπαϊκής Ένωσης για τη μείωση λαθών στις συναλλαγές, αλλά πλέον έχει υιοθετηθεί και από χώρες εκτός ΕΕ. Από τότε που εφαρμόστηκε, τα λάθη στις διεθνείς μεταφορές χρημάτων έχουν μειωθεί δραστικά, σε λιγότερο από 0,1%.

Πώς μοιάζει ένας αριθμός IBAN;

Ο αριθμός IBAN αποτελείται από έναν συνδυασμό γραμμάτων και αριθμών (έως 34 χαρακτήρες). Δεν πρέπει να συγχέεται με τον αριθμό τραπεζικού λογαριασμού, καθώς το IBAN τον περιλαμβάνει μαζί με άλλα σημαντικά στοιχεία.

Ένας τυπικός αριθμός IBAN περιλαμβάνει:

- Δίγραμμο κωδικό χώρας (π.χ. GR για Ελλάδα)

- Δύο ψηφία ελέγχου

- Κωδικό τράπεζας

- Τον BBAN (Basic Bank Account Number), δηλαδή τον βασικό αριθμό λογαριασμού, ο οποίος διαφέρει ανά χώρα και λειτουργεί ως πρότυπο για εγχώριες πληρωμές

Παράδειγμα IBAN Ηνωμένου Βασιλείου:

GB28VBCD12345612345678

- GB = Κωδικός χώρας

- 28 = Ψηφία ελέγχου

- VBCD = Κωδικός τράπεζας

- 123456 = Sort code

- 12345678 = Αριθμός λογαριασμού

IBAN vs SWIFT – Ποια η διαφορά;

Πολλοί μπερδεύονται ανάμεσα στο IBAN και τον κωδικό SWIFT. Ας ξεκαθαρίσουμε τι κάνει το καθένα.

SWIFT (ή BIC)

Ο κωδικός SWIFT χρησιμοποιείται για την ταυτοποίηση του ιδρύματος (τράπεζας) κατά τη διάρκεια μιας διεθνούς μεταφοράς χρημάτων. Αποτελείται από 8 ή 11 χαρακτήρες και περιλαμβάνει πληροφορίες για την τοποθεσία και το όνομα της τράπεζας.

IBAN

Ο αριθμός IBAN, αντίθετα, χρησιμοποιείται για να ταυτοποιήσει τον τραπεζικό λογαριασμό του παραλήπτη της συναλλαγής. Είναι ένα πρότυπο αναγνώρισης λογαριασμών, εξασφαλίζοντας ότι τα χρήματα μεταφέρονται σωστά και γρήγορα.

Συμπερασματικά:

- Ο SWIFT δείχνει ΠΟΙΑ τράπεζα συμμετέχει.

- Το IBAN δείχνει ΠΟΙΟΣ λογαριασμός εντός αυτής της τράπεζας.

Και οι δύο είναι σημαντικοί για μια σωστή και ασφαλή διεθνή συναλλαγή.

Πού θα βρείτε το IBAN σας;

Αν αναρωτιέστε πού μπορείτε να βρείτε τον αριθμό IBAN σας, υπάρχουν διάφοροι τρόποι:

- Από το λογαριασμό σας ή το εκκαθαριστικό: Τα περισσότερα τραπεζικά statements αναγράφουν το IBAN σας ξεκάθαρα.

- Από το e-banking σας: Συνδεθείτε στην πλατφόρμα online banking και ελέγξτε τα στοιχεία του λογαριασμού σας. Συνήθως υπάρχει εμφανές πεδίο με το IBAN.

- Καλέστε την τράπεζά σας: Αν δεν μπορείτε να το βρείτε, απλώς επικοινωνήστε με την εξυπηρέτηση πελατών της τράπεζας. Θα χρειαστεί να δώσετε τον αριθμό λογαριασμού και άλλα στοιχεία ταυτοποίησης.

🔍 Προσοχή: Δεν χρησιμοποιούν όλες οι χώρες το IBAN. Αν στέλνετε χρήματα διεθνώς, βεβαιωθείτε ποια μορφή απαιτείται για τον παραλήπτη.

Επιπλέον, το μήκος και η δομή ενός IBAN διαφέρουν από χώρα σε χώρα — οπότε πάντα επιβεβαιώστε ότι τα στοιχεία έχουν καταχωρηθεί σωστά πριν από οποιαδήποτε μεταφορά.

IBAN και επαγγελματικοί λογαριασμοί στην Tap

Ανοίγοντας έναν επαγγελματικό λογαριασμό μέσω της πλατφόρμας Tap, κάθε χρήστης αποκτά αυτόματα έναν μοναδικό αριθμό IBAN.

Αυτός μπορεί να χρησιμοποιηθεί για την παραλαβή διεθνών πληρωμών, με υποστήριξη για πολλαπλά νομίσματα, καλύπτοντας τις ανάγκες διαφόρων κλάδων και επιχειρήσεων.

Το Etherscan είναι ένα δωρεάν εργαλείο εξερεύνησης blockchain που επιτρέπει σε οποιονδήποτε να βλέπει τις συναλλαγές που πραγματοποιούνται στο δίκτυο του Ethereum. Και όχι μόνο! Μέσα από την πλατφόρμα μπορείτε να εντοπίσετε blocks, χρεώσεις gas, διευθύνσεις πορτοφολιών, έξυπνα συμβόλαια και κάθε είδους on-chain δεδομένα.

Τι είναι το Etherscan;

Το Etherscan είναι ένας εξερευνητής blockchain ειδικά για το δίκτυο του Ethereum. Μέσα από αυτό το εργαλείο, μπορείτε να αποκτήσετε μια εικόνα για την κατάσταση των συναλλαγών, των χρεώσεων gas, των έξυπνων συμβολαίων (smart contracts) και του περιεχομένου αποκεντρωμένων εφαρμογών (dApps). Πρόκειται για ένα παράθυρο στη διαφάνεια του blockchain.

Δεν χρειάζεται να δημιουργήσετε λογαριασμό για να δείτε δεδομένα. Ωστόσο, αν το επιθυμείτε, μπορείτε να ανοίξετε λογαριασμό και να έχετε πρόσβαση σε επιπλέον λειτουργίες όπως ειδοποιήσεις για εισερχόμενες συναλλαγές ή εργαλεία για developers. Αν χρησιμοποιείτε dApps, παρακολουθείτε πορτοφόλια ή συμμετέχετε σε blockchain παιχνίδια, το Etherscan είναι ένα πολύτιμο εργαλείο.

Γιατί το Etherscan είναι τόσο δημοφιλές;

Το Etherscan είναι ο πιο δημοφιλής εξερευνητής για το δίκτυο του Ethereum — και όχι άδικα. Παρόλο που δεν είναι πορτοφόλι και δεν επιτρέπει την αγορά ή πώληση κρυπτονομισμάτων, προσφέρει πλήρη εικόνα του δικτύου, με στατιστικά, αναλύσεις και ιστορικά στοιχεία για το ETH και τα tokens που βασίζονται σε αυτό.

Είναι επίσης χρήσιμο για να κατανοήσετε πώς λειτουργεί το blockchain στην πράξη και μπορεί να σας βοηθήσει να εντοπίσετε ύποπτες κινήσεις, όπως μεγάλες πωλήσεις από "φάλαινες" ή μετακινήσεις tokens από ομάδες έργων.

Πώς χρησιμοποιείται το Etherscan;

Αν θέλετε να επιβεβαιώσετε μια συναλλαγή ή να ελέγξετε ένα έξυπνο συμβόλαιο, το Etherscan σας καλύπτει. Παρακάτω εξηγούμε πώς μπορείτε να εντοπίσετε μια συναλλαγή.

Πώς να εντοπίσετε μια συναλλαγή στο Etherscan

Κάθε συναλλαγή στο blockchain συνοδεύεται από ένα μοναδικό αναγνωριστικό (TXID), γνωστό και ως "transaction hash". Μοιάζει κάπως έτσι:

CopyEdit

0x3349ea4144aed83291f87b3904b02f8f1e76c3b5bfed0d95a000fafddaed01bc

Για να παρακολουθήσετε την πρόοδο ή να δείτε λεπτομέρειες για μια συναλλαγή, απλώς αντιγράψτε αυτό το TXID στο πεδίο αναζήτησης στην αρχική σελίδα του Etherscan. Εκεί θα δείτε πληροφορίες όπως:

- Transaction Hash: Το μοναδικό ID της συναλλαγής

- Κατάσταση: Αν η συναλλαγή έχει ολοκληρωθεί, αποτύχει ή είναι σε εξέλιξη

- Block: Ο αριθμός του block στο οποίο καταχωρήθηκε

- Ώρα/Ημερομηνία: Πότε πραγματοποιήθηκε η συναλλαγή

- Αποστολέας: Η διεύθυνση πορτοφολιού που έστειλε τα κεφάλαια

- Παραλήπτης: Η διεύθυνση πορτοφολιού ή έξυπνο συμβόλαιο που τα έλαβε

- Ποσό: Το ποσό που μεταφέρθηκε

- Χρέωση συναλλαγής: Ποσό σε gas fees

- Τιμή Gas: Η τιμή ανά μονάδα gas κατά την εκτέλεση (σε ETH ή Gwei)

Πώς να δείτε τις τιμές gas στο Etherscan

Όλες οι συναλλαγές στο Ethereum απαιτούν πληρωμή gas. Αυτές οι χρεώσεις εξαρτώνται από το πόσο "φορτωμένο" είναι το δίκτυο. Μέσα από το εργαλείο Gas Tracker του Etherscan μπορείτε να δείτε σε πραγματικό χρόνο τις τιμές gas και τη συνολική δραστηριότητα στο δίκτυο.

Συμπέρασμα

Το Etherscan είναι ένα από τα πιο χρήσιμα εργαλεία για όσους χρησιμοποιούν το Ethereum. Σας επιτρέπει να επιβεβαιώνετε συναλλαγές, να παρακολουθείτε έξυπνα συμβόλαια και να έχετε καλύτερη εικόνα του τρόπου λειτουργίας του blockchain. Η διαφάνεια είναι στο επίκεντρο των κρυπτονομισμάτων και το Etherscan είναι ο καθρέφτης αυτής της αρχής.